What Determines the Rate on a 30-Year Mortgage?

This has caused potential homebuyers, mortgage lenders, and other market observers to ask us — why have mortgage rates risen despite the Fed cutting rates?

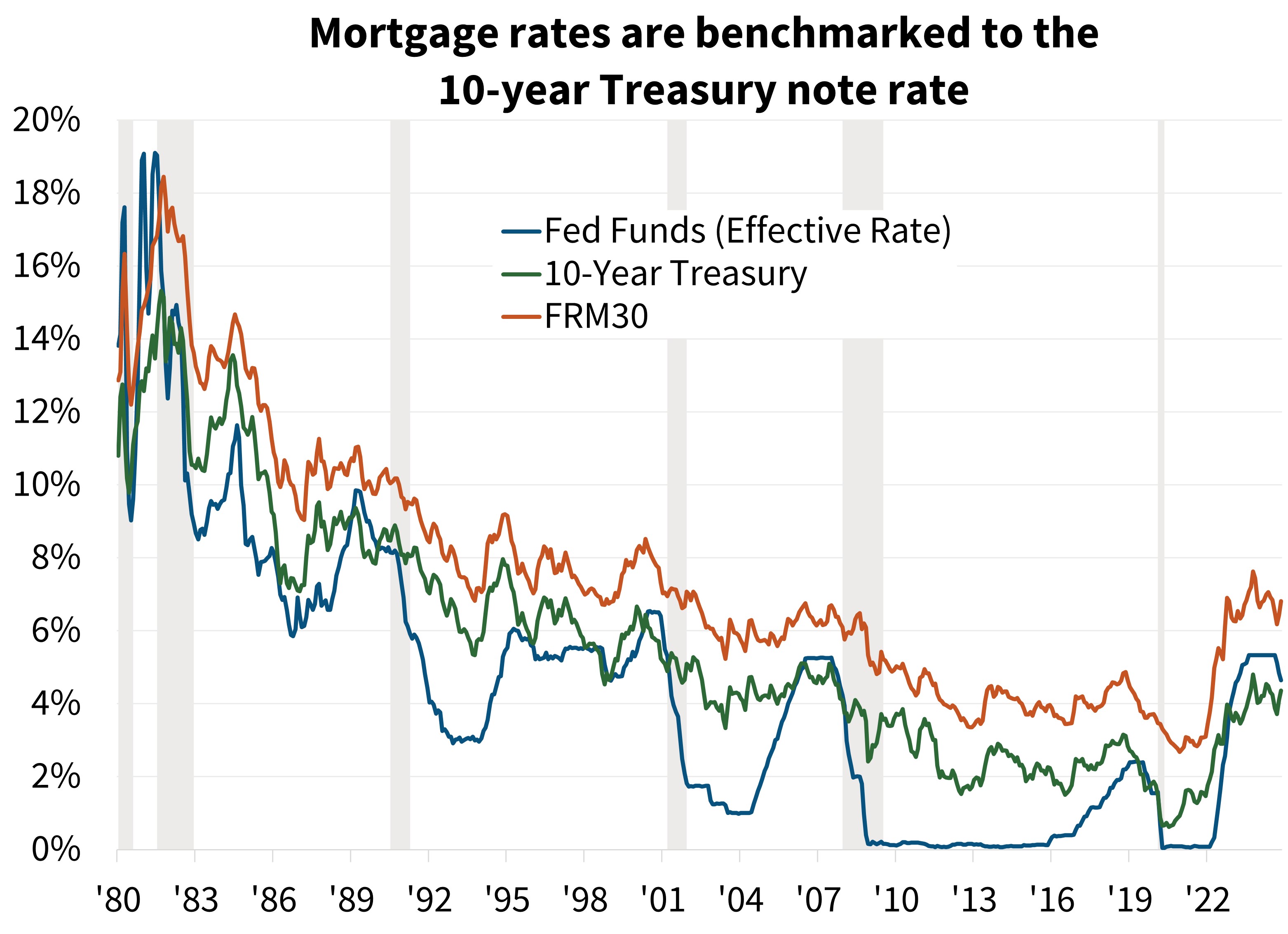

The short answer is this: The federal funds rate is the interest rate at which banks lend money to one another overnight, meaning it's an interest rate on very short-term lending. Interest rates on other short-term bonds and loans move very closely with changes in the federal funds rate. The 30-year mortgage, on the other hand, is a long-duration loan and thus has a different rate at which market participants are willing to lend. This rate is determined in the bond market.

Below, we explain how the rate on a 30-year mortgage is determined and how these factors explain the movements in mortgage rates following the COVID-19 pandemic.

Key takeaways

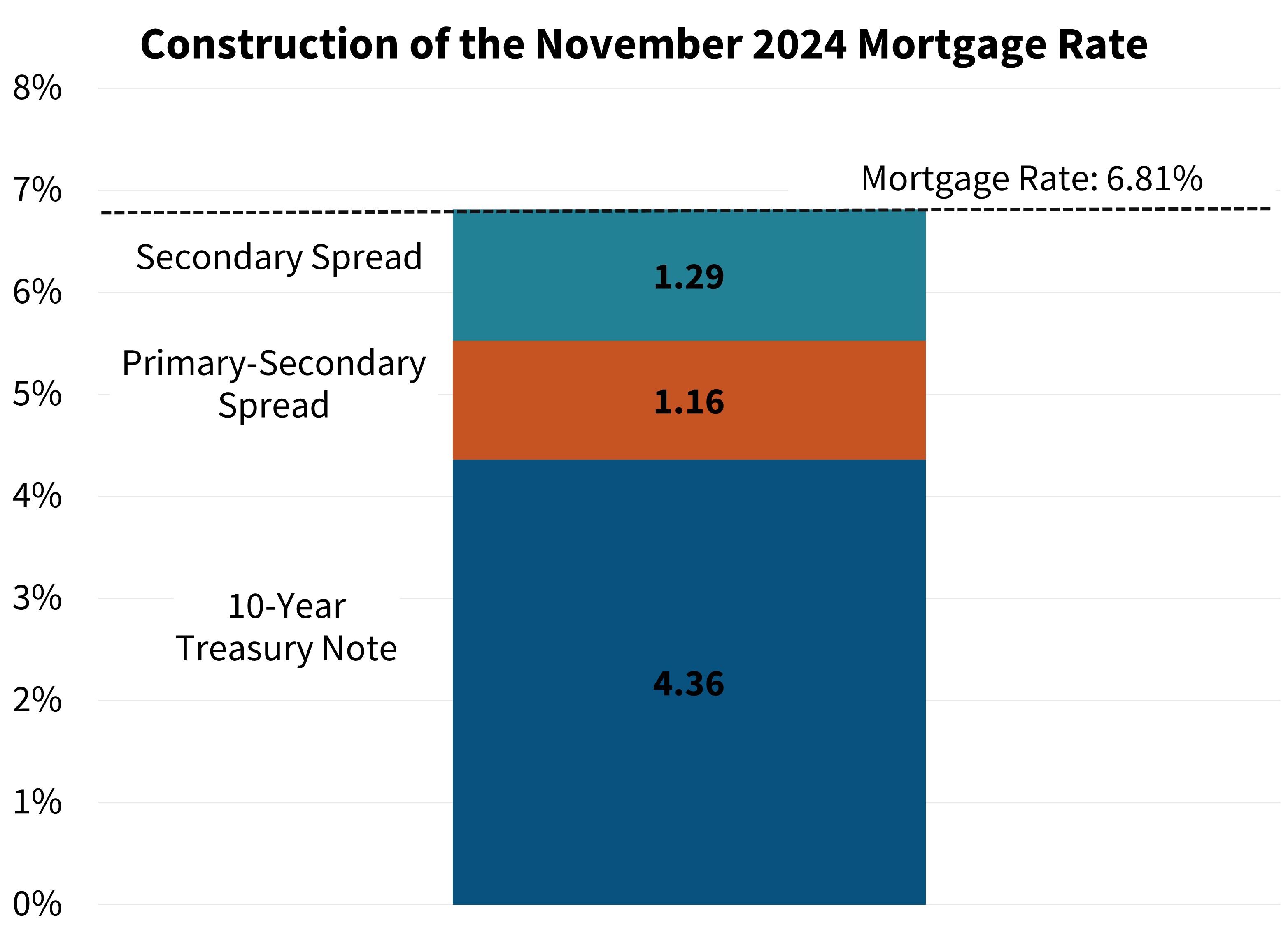

- The 30-year mortgage rate is benchmarked to the rate of the 10-year Treasury note. As the rate on the 10-year Treasury note moves, mortgage rates follow suit.

- The rate on the 10-year Treasury note is determined by investors' expectations for shorter-term interest rates in the economy over the duration of the bond plus a term premium, which compensates investors for the risks associated with holding a longer-duration bond. Expectations of short-term rates are influenced by investors' expectations for monetary and fiscal policy, economic growth, and inflation.

- Mortgage rates are determined by adding a spread to the benchmark 10-year Treasury note. The spread, or difference, between the rate offered on a 30-year mortgage and the 10-year Treasury note is constructed of two primary components:

- The primary-secondary mortgage spread is the difference between the mortgage rate that is offered to borrowers and the rate on a mortgage-backed security (MBS). This spread reflects industry costs of originating a mortgage and lender margins.

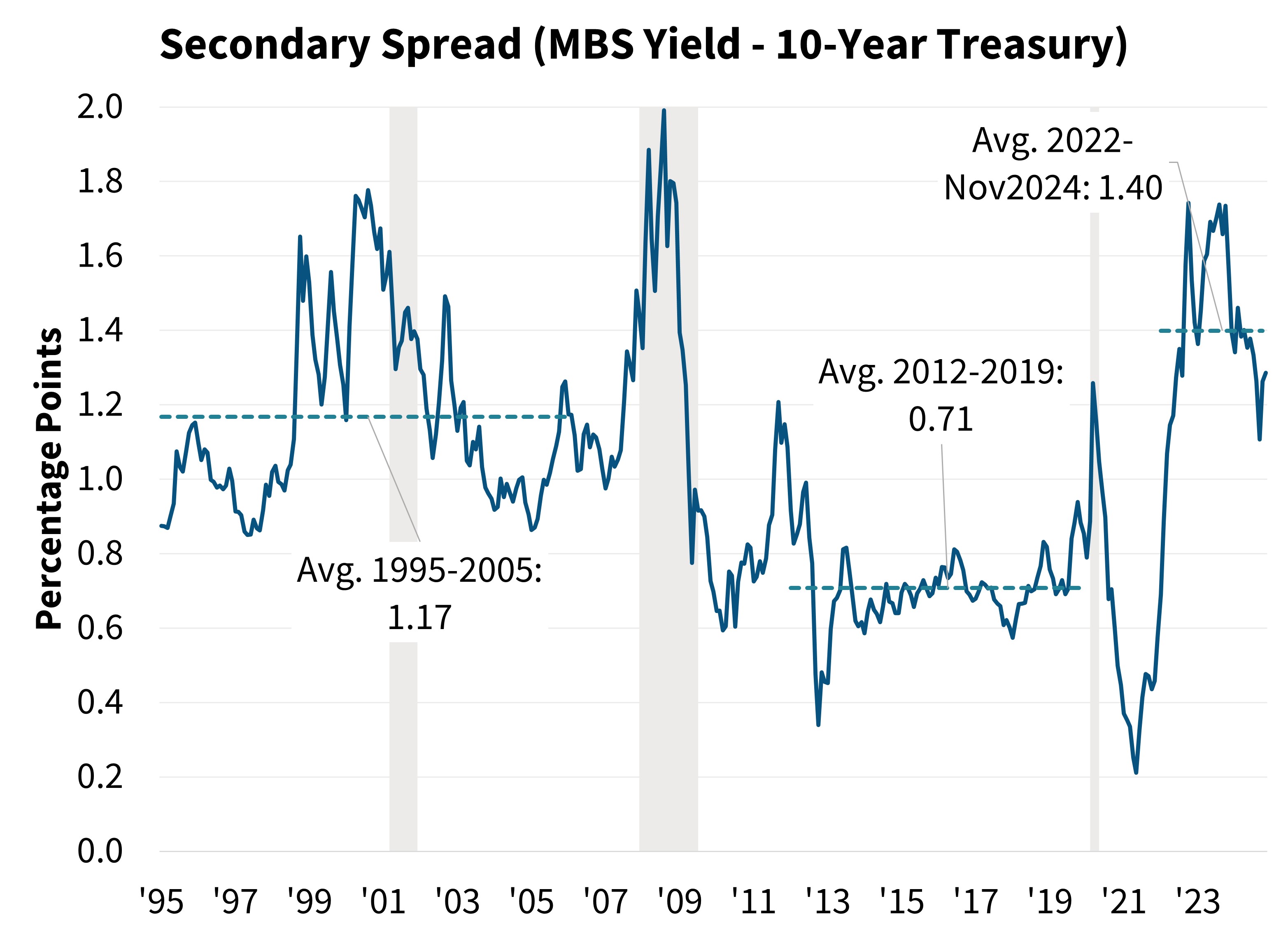

- The secondary mortgage spread is the difference between the rate on an MBS and the rate on the 10-year Treasury note. This spread reflects the additional risk present in an MBS relative to the 10-year Treasury note.

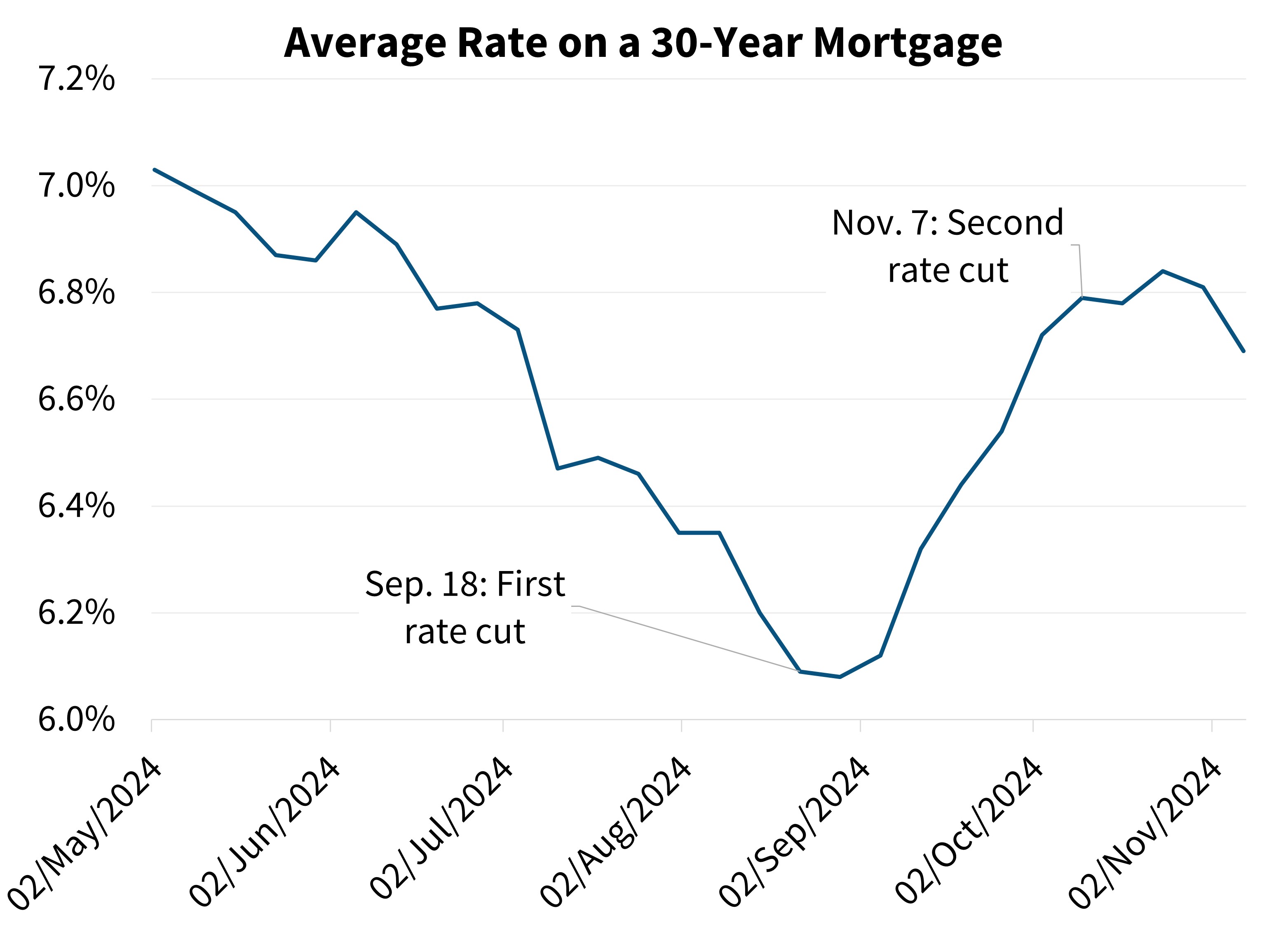

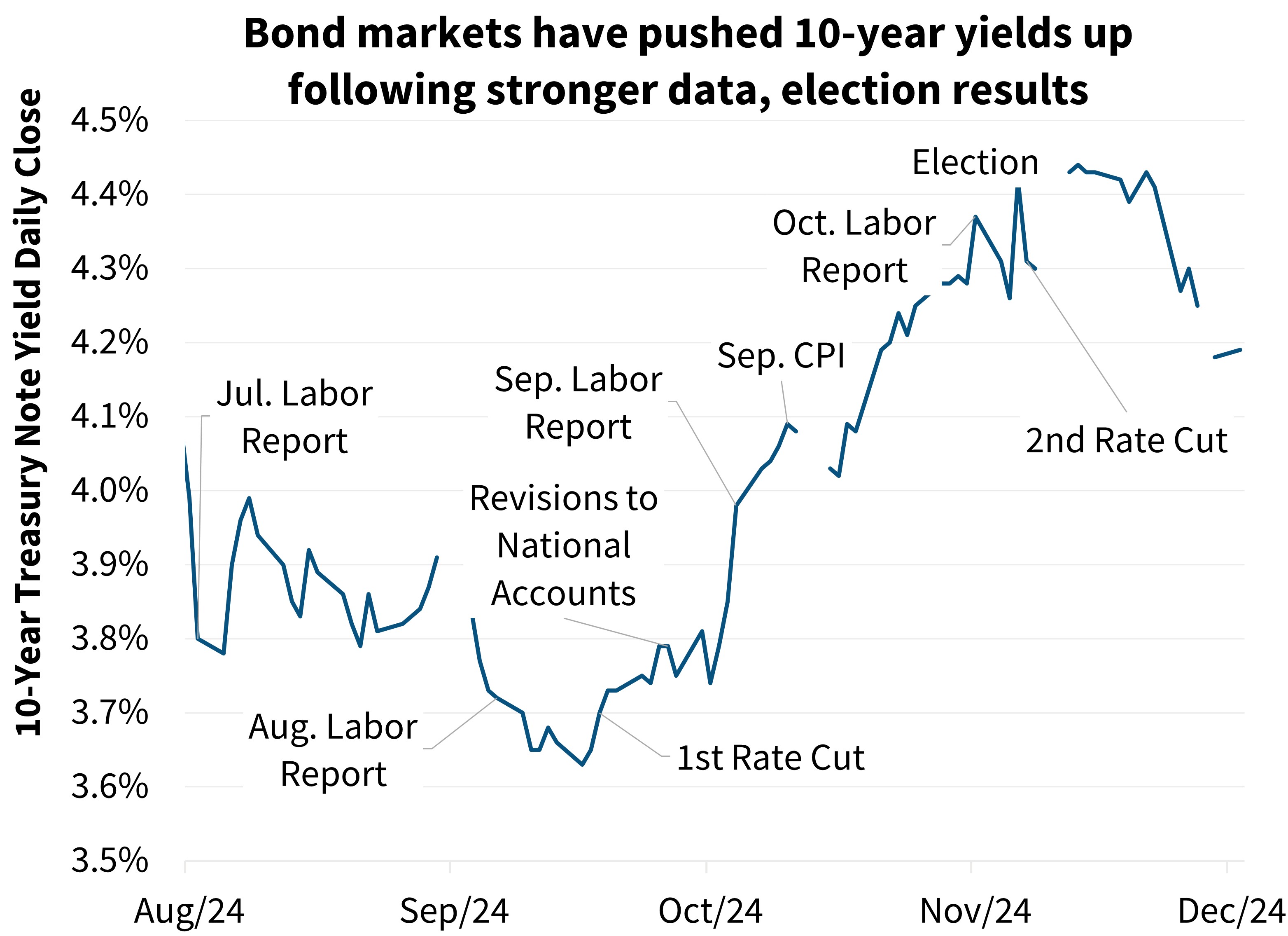

- Since the Federal Reserve cut interest rates in September, the market has digested positive economic data releases, stickier-than-expected inflation data, and the outcome of the 2024 election. These have ultimately pushed the rate on the 10-year Treasury note upward, and thus mortgage rates have risen.

The 10-Year Treasury Note and the 30-Year Mortgage

What Determines the Rate on the 10-Year Treasury Note?

The rate on the 10-year Treasury note is determined by investors' expectations for short-term interest rates over the duration of the bond.

Consider, as an example, an investor who is choosing between the 10-year Treasury note and a much shorter-duration 1-year Treasury bill. Instead of purchasing the 10-year Treasury note, the investor could purchase a 1-year Treasury bill and roll over their investment each year into a new 1-year Treasury bill for 10 years. The investor then would consider what they expect the rate on a 1-year Treasury bill (and other short-term rates) to be over the next 10 years when determining the rate they will require to purchase a 10-year Treasury note. Because interest rates over a 10-year period are highly uncertain, investors take on additional risk when investing in a long-duration bond. Investors typically demand additional yield (i.e., a higher rate), known as the term premium, on a longer-duration bond compared to a short-duration bond to compensate them for this additional risk.

Investors' expectations for shorter-term interest rates, and thus the rate they are willing to accept on the 10-year Treasury note, are informed by their views on future monetary and fiscal policy, economic growth, and inflation.

- Monetary policy: The Federal Reserve sets the target federal funds rate to achieve its dual mandate of maximum employment and stable prices. The federal funds rate provides a benchmark for other interest rates in the economy, particularly short-term rates. While current monetary policy has some impact on the 10-year Treasury note rate, investors' expectations of future monetary policy are more important. Bond market investors set the rate they are willing to accept on the 10-year Treasury note based on their expectations of short-term interest rates over the duration of the bond, which is in part a function of their expectations for monetary policy over the next 10 years.

- Fiscal policy: Fiscal policy can affect economic growth and inflation. It can also affect the supply of government debt, depending on its impact on the federal budget deficit. When government debt issuance is high (or expectations are that it will be high), there is upward pressure on interest rates to attract sufficient demand to purchase government debt. Expectations for debt issuance may also affect the term premium.

- Economic growth: Economic growth informs monetary policy given the Fed's dual mandate for price stability and maximum employment, as maximum employment generally relies on a strong economy. Additionally, economic growth affects the demand for bonds like the 10-year Treasury note. Investors who expect a stronger economy may seek other investment opportunities, such as equities. This causes demand for Treasury bonds to decline, pushing rates upward to attract investment. Conversely, if investors expect poor economic growth, they may seek a "safe haven" in Treasury bonds, causing rates to decline as demand rises.

- Inflation: Inflation informs the stable prices side of the Fed's mandate. Additionally, inflation causes a loss of purchasing power. If investors expect higher inflation, they will demand higher interest rates as compensation, while expectations for lower inflation cause investors to demand a lower interest rate.

The Mortgage Spread

The Primary-Secondary Mortgage Spread

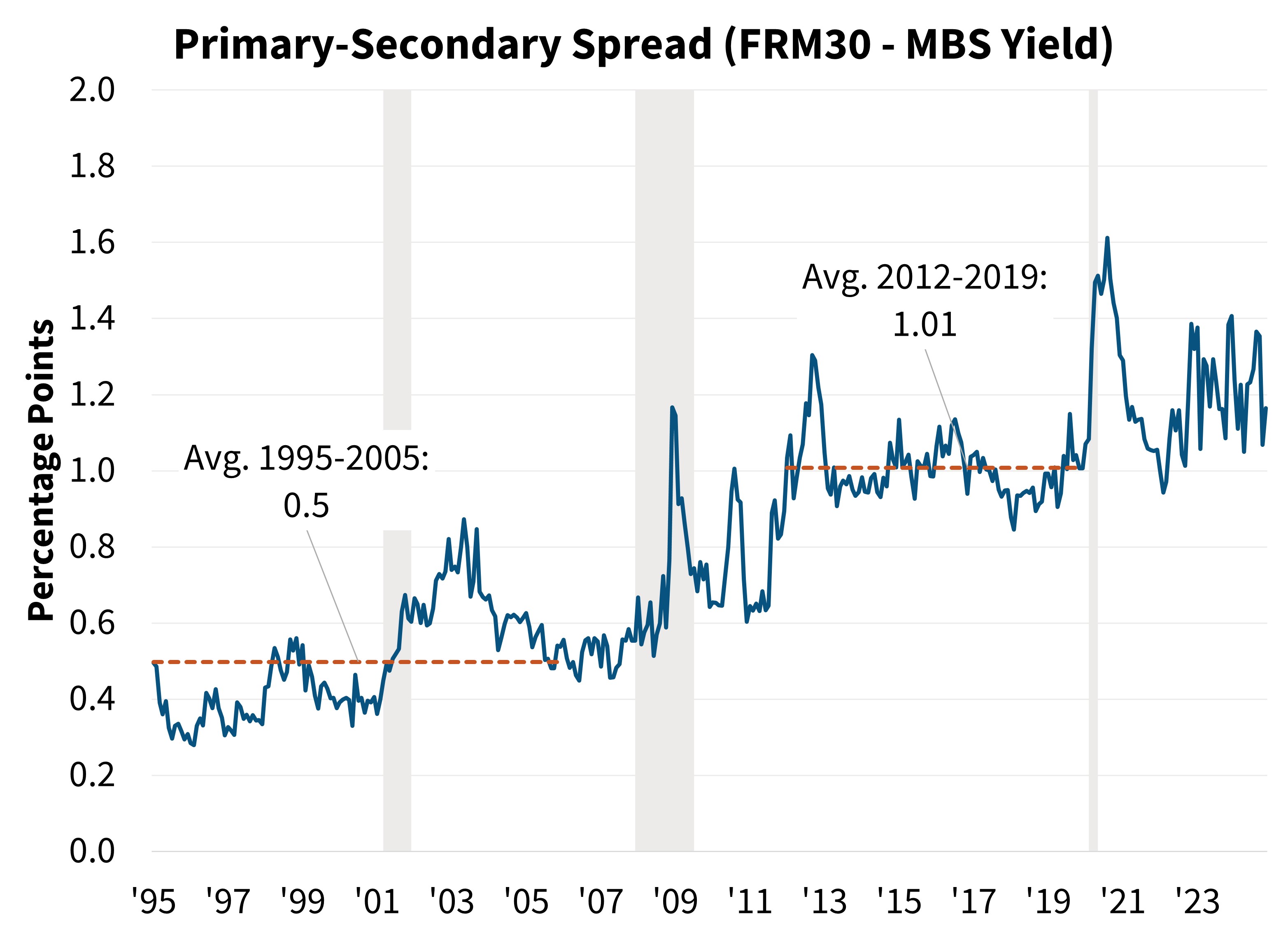

The Secondary Mortgage Spread

The other component of the mortgage spread is the secondary spread, which is the difference between the rate on an MBS yield and the rate on a 10-year Treasury note. Relative to the 10-year Treasury note, MBS carry two additional risks:

- Prepayment risk: Unlike the 10-year Treasury, which has a guaranteed rate for the duration of the bond, mortgage borrowers may prepay before the end of their mortgage term to refinance, move, or pay off their mortgage early.

- Credit risk: Whereas the 10-year Treasury is considered a virtually risk-free investment, a mortgage borrower or the entity providing a guarantee to the MBS investor may defaultii.

While changes in credit or prepayment risk may explain some of the volatility in the secondary spread during specific periods, the Federal Reserve’s balance sheet actions are the main factor driving the difference in the secondary spread.

Following the Great Financial Crisis, the Federal Reserve began purchasing MBS and Treasury securities, a policy known as quantitative easing, to stabilize the financial system and drive interest rates, particularly mortgage rates, lower. The Fed is a non-economic buyer, which means it is not sensitive to the rate an MBS is paying. Therefore, when the Fed purchases MBS, it replaces private investors who are sensitive to the rate on MBS, which drives the secondary spread lower.

When the Fed does not purchase MBS to offset the ongoing runoff of MBS in its portfolio, a policy known as quantitative tightening, it gradually owns a smaller share of total MBS outstanding. As a result, private investors need to purchase that additional share, and as rate-sensitive buyers, they require a higher interest rate to do so. That’s why the secondary spread is driven upward when private investors replace the Fed in the MBS market.

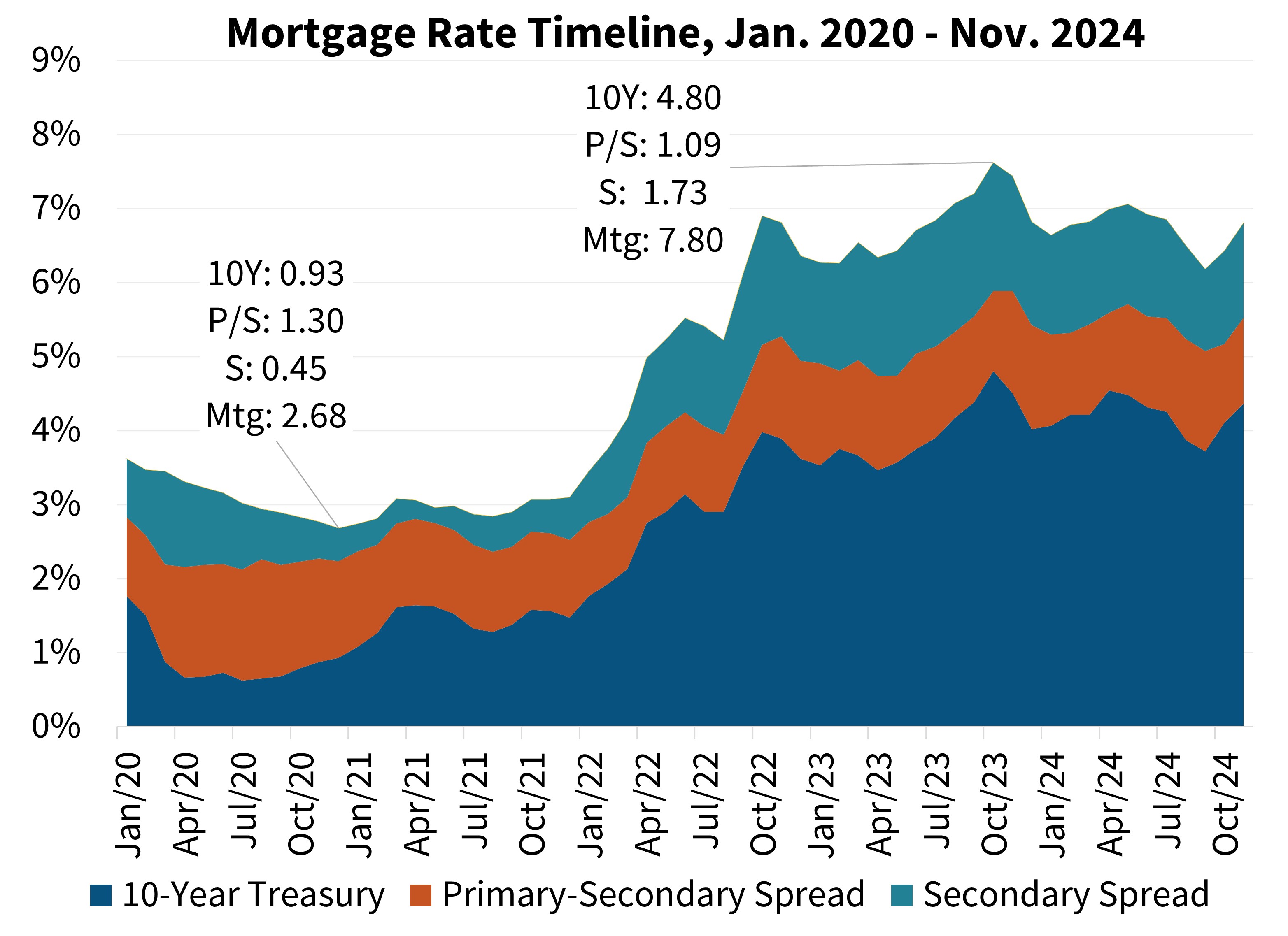

A Look at Mortgage Rates Since 2020

When mortgage rates hit their cycle-high of 7.8 percent in October 2023, the rate on the 10-year Treasury note had risen to a monthly average of 4.8 percent. Economic growth was strong, and inflation remained elevated well above the Fed’s 2-percent target. The federal funds rate was at 5.33 percent and the market expected a “higher for longer” policy stance from the Fed, meaning short-term rates were likely to stay high.

Additionally, the Fed’s balance sheet run-off put upward pressure on the secondary spread, which was elevated at 1.73 percentage points, as private investors sought higher rates on MBS to absorb the additional share. From this, we can see the rise in mortgage rates since the end of 2020 has been due primarily to an increase in the 10-year Treasury note rate and a widening in the secondary spread.

Following the September 2024 reduction in the federal funds rate, bond market investors have digested a number of data releases that point to a stronger economy than many had expected and somewhat-stickier inflation than previously thought. Given these developments, along with the results of the 2024 election

We highlighted this interest rate dynamic in our November Economic Commentary, where we shared our expectation that existing home sales will remain subdued through the next year due to the significant increase in mortgage rates and other long-duration bond rates since September.

Data sources for charts: Freddie Mac, Federal Reserve Board, Fannie Mae

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR Group bases its opinions, analyses, estimates, forecasts, beliefs, and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current, or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR Group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

i The average mortgage duration is generally considered to be 7-10 years. When lenders and investors benchmark the rate on a 30-year mortgage to other Treasury notes, they use a blend of 5, 7, and 10-year Treasury notes. For simplicity, this Housing Insights piece will focus on just the 10-year Treasury note.

ii Agency MBS do not have borrower credit risk because they carry a guaranty of timely payment of both principal and interest. Fannie Mae’s obligations under this guaranty are based on the financial health of the corporation and are not backed by the full faith and credit of the U.S. government.

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count