Economic Developments - February 2025

For a PDF version of this report, click here.

- Incoming economic data since our last forecast, including the fourth quarter gross domestic product (GDP) report, labor market data, and inflation readings, point to an economy that entered 2025 with strong momentum. Our GDP outlook (2.2 percent Q4/Q4 in 2025) is only modestly revised this month, with stronger growth in Q1 offset by a slower pace of expansion later in the year.

- We have upwardly revised our inflation forecast primarily due to higher-than-expected recent data releases. We now expect the Consumer Price Index (CPI) to be 2.8 percent on a Q4/Q4 basis in 2025 and core CPI to be 2.9 percent (previously 2.5 percent for both). In line with financial markets, we now expect just one cut to the federal funds rate this year as the Fed responds to inflation data that is more "sticky" than previously anticipated.

- This forecast incorporates the currently implemented additional 10 percent tariff on imports from China, which has reduced our GDP forecast by one-tenth on a Q4/Q4 basis and increased our CPI forecast for 2025 by roughly the same magnitude (all else equal). Other tariff proposals that are not currently implemented are not included in our base forecast, though they present higher-than-usual risks to our current outlook.

- We have modestly upgraded our mortgage rate outlook this month and expect rates will end 2025 and 2026 at 6.6 and 6.5 percent, respectively. The net effect of tariffs on mortgage rates is unclear, and there are plausible scenarios for both upward and downward movement in rates. As such, we continue to expect mortgage rate volatility as markets react to tariff implementation, incoming economic data, and other fiscal policy changes.

- Our housing forecast is little changed this month, with a slight upgrade to existing home sales due to stronger-than-expected sales data in December. While we continue to forecast new home sales to outperform relative to existing sales, we have revised downward our new sales forecast modestly to reflect a weaker-than-expected Q4 2024.

- In turn, our outlook for single-family mortgage originations has been only slightly modified to $1.89 trillion in 2025 (previously $1.92 trillion) and $2.22 trillion in 2026 (previously $2.27 trillion).

Economy, Labor Market, and Inflation Start 2025 on Firm Footing

Incoming economic data since our last forecast continue to show that the economy entered 2025 on firm footing. GDP rose at a 2.3 percent annualized rate in the fourth quarter, close to our forecast of 2.4 percent. While we had predicted consumption would continue to grow at a robust annualized pace of 3.3 percent, the actual 4.2 percent growth rate surprised to the upside and implies a stronger-than-expected handoff to the first quarter, causing an upward revision to our near-term consumption forecast, though we do continue to expect deceleration moving forward. Due to inventory investment being a large drag on Q4 GDP growth, final sales to private domestic purchasers, which is sometimes considered “core GDP” and more indicative of underlying trends, posted an even stronger 3.2 percent annualized growth rate compared to topline GDP growth of 2.3 percent.

A continuation of strong economic growth and a firming in the labor market is consistent with increased inflation pressures relative to earlier in 2024. In January, the core CPI rose 0.4 percent over the month and ticked up one-tenth to 3.3 percent compared to a year ago. While some of the hotter-than-expected CPI may be due to ongoing seasonal adjustment issues that have pushed inflation readings upward in the first quarter of recent years, year-over-year core CPI readings have not decelerated meaningfully in eight months. Further, core CPI has risen at a 3.8 percent annualized rate over the past three months and 3.7 percent over the past six months. As a result of incoming data, we now expect headline and core CPI to grow at 2.8 and 2.9 percent on a Q4/Q4 basis in 2025, upward revisions of three-tenths and four-tenths, respectively.

Financial markets are now pricing in just one 25-basis-point rate cut this year, in line with our updated view of only one fed funds rate cut occurring in 2025, which we now expect will occur in September (we previously anticipated two cuts).

Tariffs and Trade Policy Uncertainty Adds to Risk Around the Forecast

While all economic forecasts are subject to risks, current trade policy uncertainty presents higher-than-usual risks to our forecast this month. For this forecast, we have incorporated the additional 10 percent tariff on imports from China, but we have not included any of the other tariffs measures currently being discussed. Implementing the increase in the tariff rate on imports from China leads to a slight downward revision to our growth forecast for 2025 of about one-tenth and an upward revision to our core inflation forecast for the next year of roughly the same magnitude.

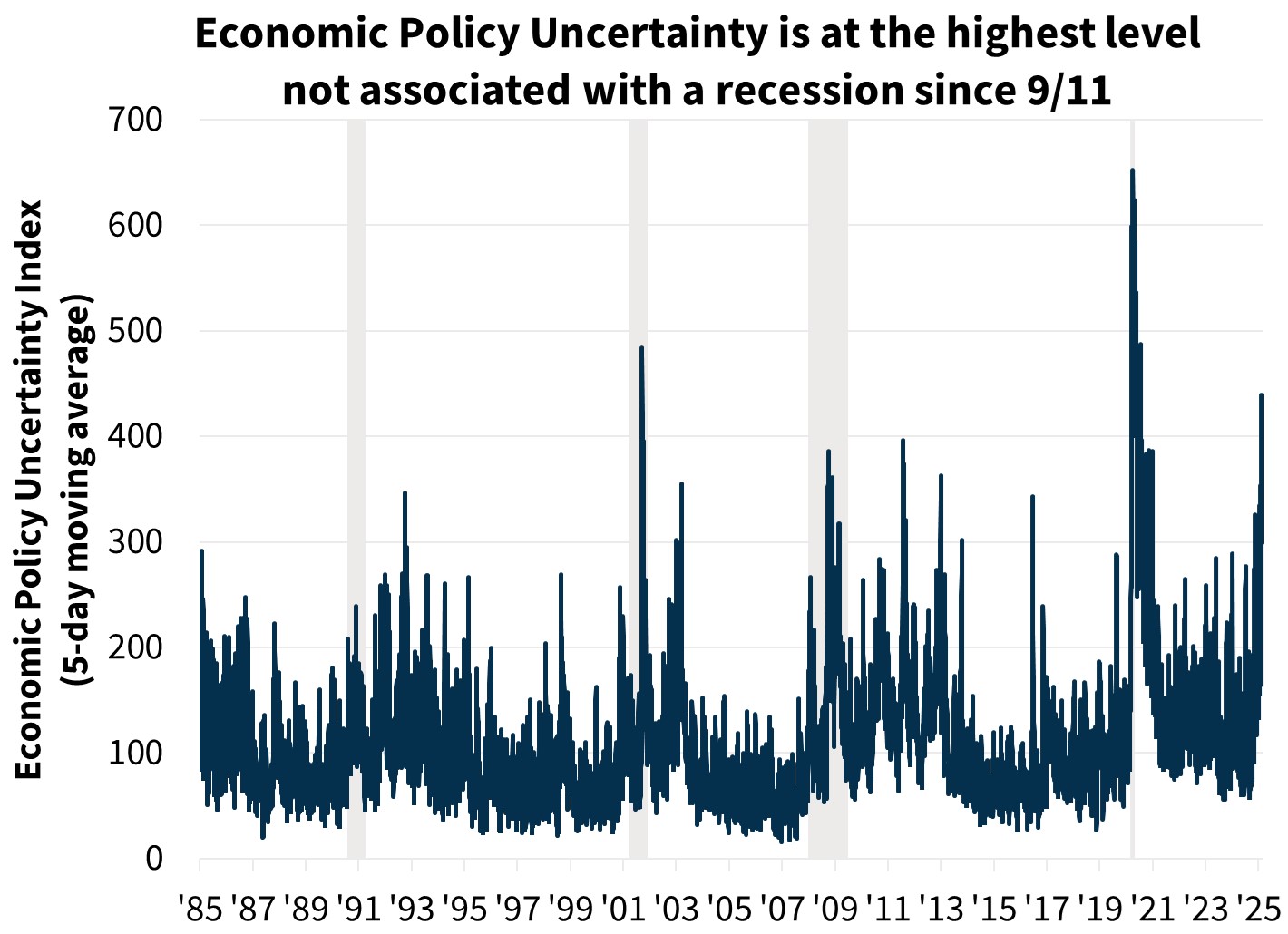

Sustained uncertainty may weigh on business investment and consumer spending as firms and households delay activities. For instance, the Economic Policy Uncertainty Index recently spiked to the highest levels on record outside of recessionary periods.

Trade Policy and Effects on Mortgage Rates Unclear

It’s not clear how all of this will affect mortgage rates. If additional tariffs are implemented, there are plausible scenarios where it could lead to either higher or lower mortgage rates, depending on the details, timing, and the reaction of foreign nations and central banks.

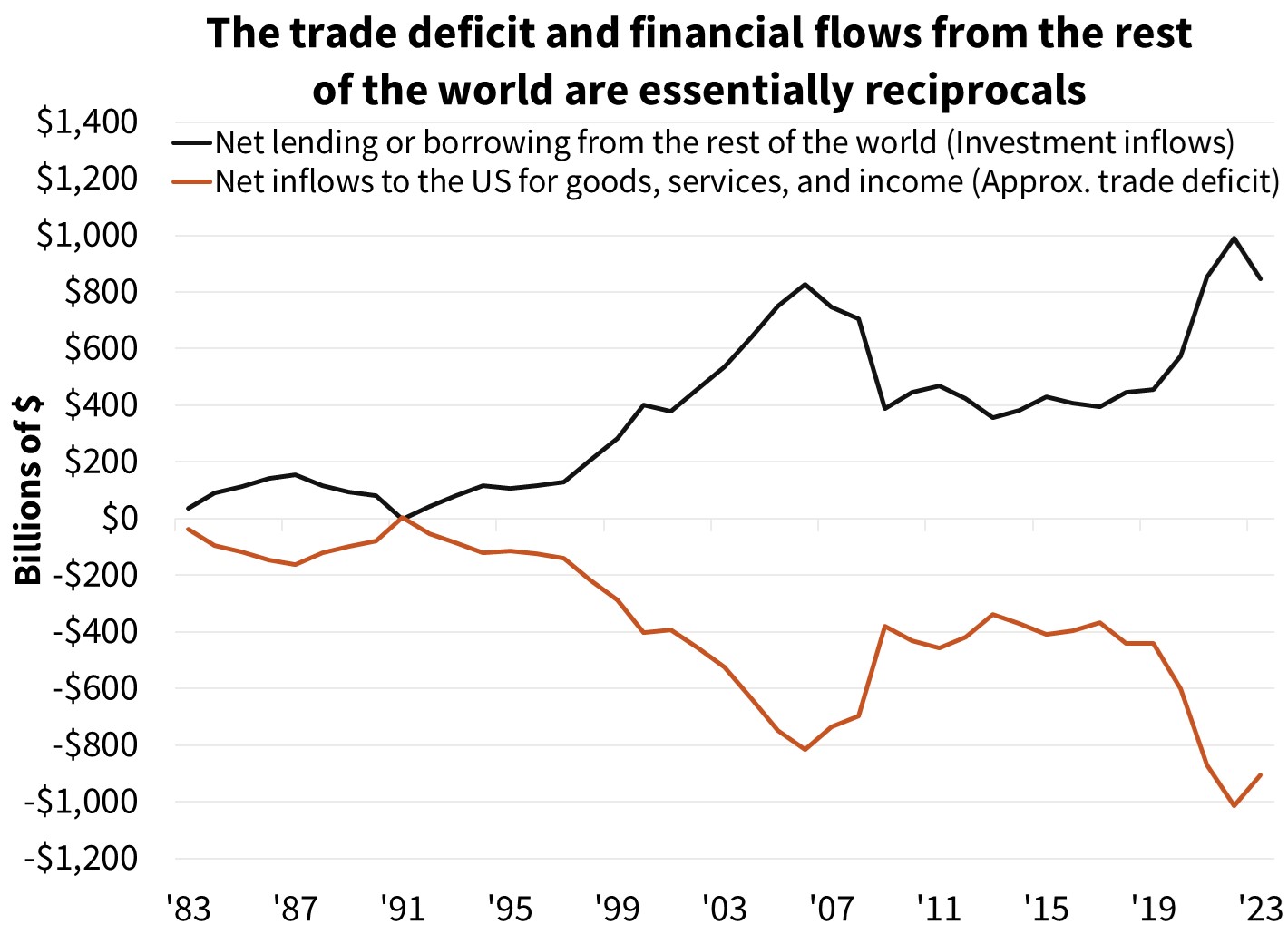

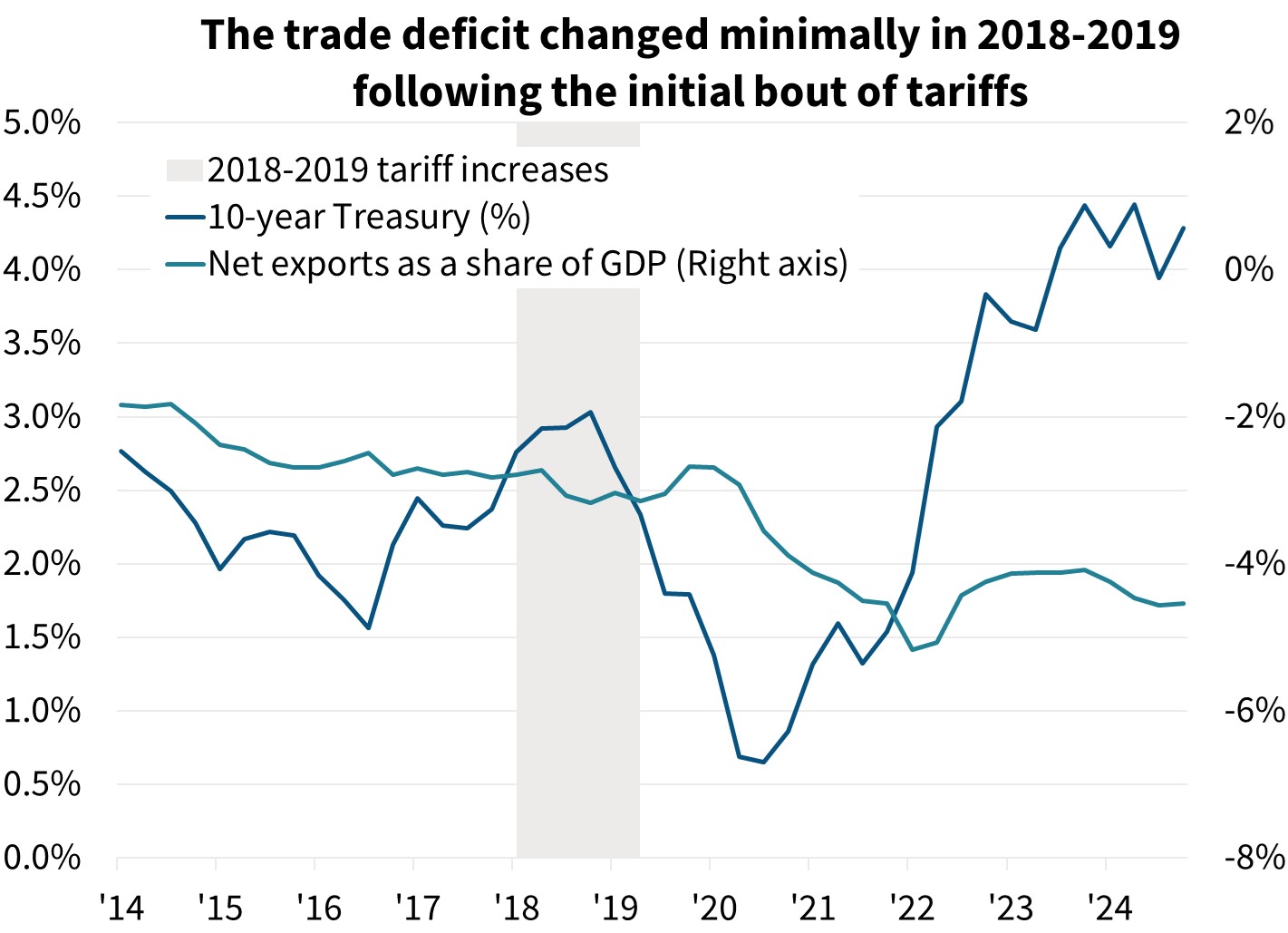

However, other nations would likely implement retaliatory tariffs, and currency exchange rates would adjust. On net, we expect increasing tariffs is more likely to reduce overall trade volumes (imports and exports) than to reduce the trade deficit. Looking back at the 2018-2019 period when tariffs were previously increased, the trade deficit as a share of GDP was not meaningfully changed. Interest rates may still move upward if the near-term increase in price levels leads to a rise in inflationary expectations, and the Fed responds by holding rates higher for longer.

Further complicating this analysis is how tariffs fit into broader fiscal policy. If tariff revenues are used to reduce fiscal deficits, then they would translate into a contractionary fiscal policy, suggesting a lower fed funds rate will be needed going forward to maintain the dual employment and 2-percent inflation target. However, if proceeds are used to finance additional spending or offset other tax cuts, then the effects on aggregate demand in the economy and monetary policy response would differ.

In summary, we are holding to one of our major themes for the year. While we expect mortgage rates to remain comparatively elevated as a baseline, periods of heightened volatility should be expected. Rates are likely to move, perhaps sharply, as trade, fiscal, and monetary policy developments unfold and associated economic data is released.

Home Sales Expected to Remain Sluggish – Only Modest Revisions to the Outlook

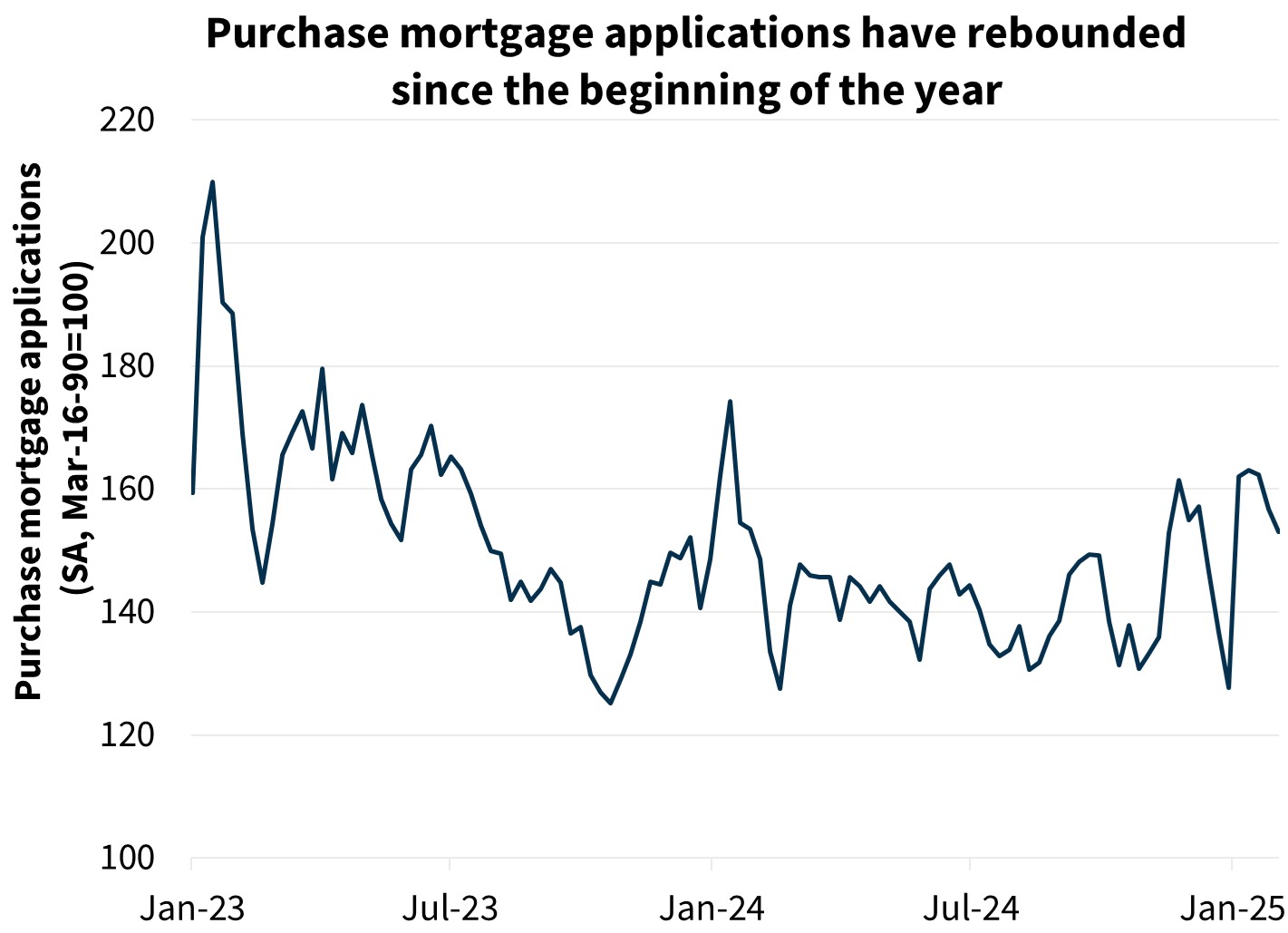

Pending home sales, which, on average, lead closings by 30-45 days, fell 5.5 percent in December, pointing to some pull-back in sales in Q1 from the December pace. We project 2025 existing home sales to rise slightly from 2024 by 2.9 percent, but this would reflect a pace still down 22 percent from 2019.

We have made only modest revisions to our new home sales and single-family housing starts outlooks, primarily driven by recent incoming data. Housing starts rose somewhat more than we had anticipated in December, while new home sales, following disruptions from hurricanes in October, rebounded by somewhat less than anticipated.

Fundamentally, our view remains intact that new home sales and construction will remain comparatively strong this year, as homebuilders have shown a willingness to continue to use concessions to drive sales, though a build-up of inventories in some key metros presents some downside risk to this forecast. We expect the pace of single-family starts to fall slightly by 1.4 percent in 2025 after rising 6.5 percent in 2024, as builders work off some of their existing inventory of completed homes for sale. It should be noted, however, that beyond previously mentioned mortgage rate risk, the future development of tariff policies also presents risk to the pace of new home construction due to effects on the prices of lumber and other building materials.

Economic Forecast Changes

Economic Growth

Following the strong Q4 2024 gross domestic product (GDP) report, we’ve upgraded our Q1 2025 GDP growth expectation to a seasonally adjusted annualized rate (SAAR) of 2.5 percent, up three-tenths from the prior forecast, as we expect consumption to remain strong in the first quarter, though not as strong as the prior two quarters. Our Q4/Q4 growth expectation for 2025 was unchanged at 2.2 percent, while our 2026 forecast was revised up to 2.2 percent Q4/Q4 growth, up two-tenths from our last forecast. Our February forecast has been changed to reflect the 10 percent tariff on goods from China, though this has a minor impact on our growth outlook, only shaving about a tenth off of 2025 GDP growth.

Labor Market

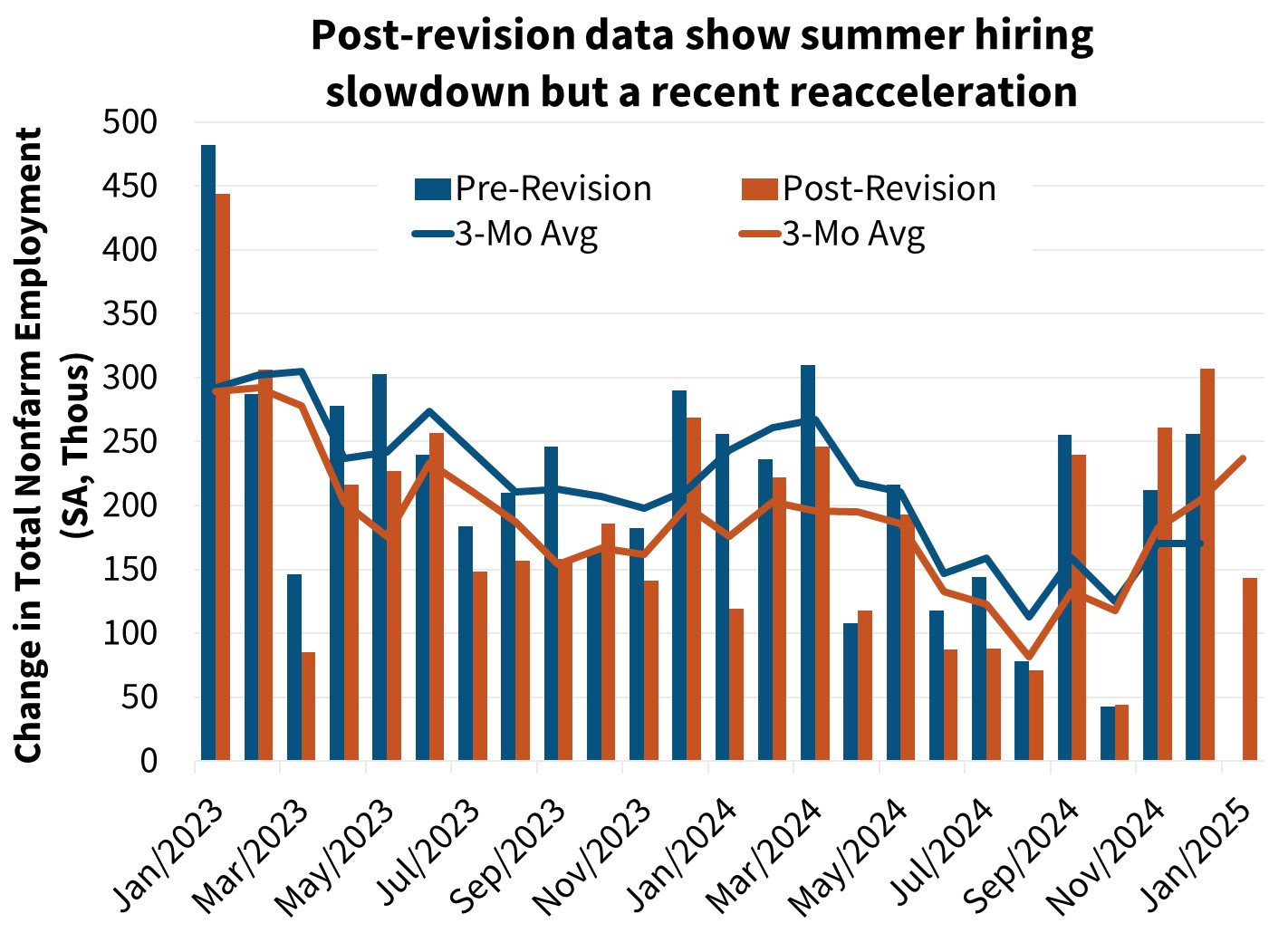

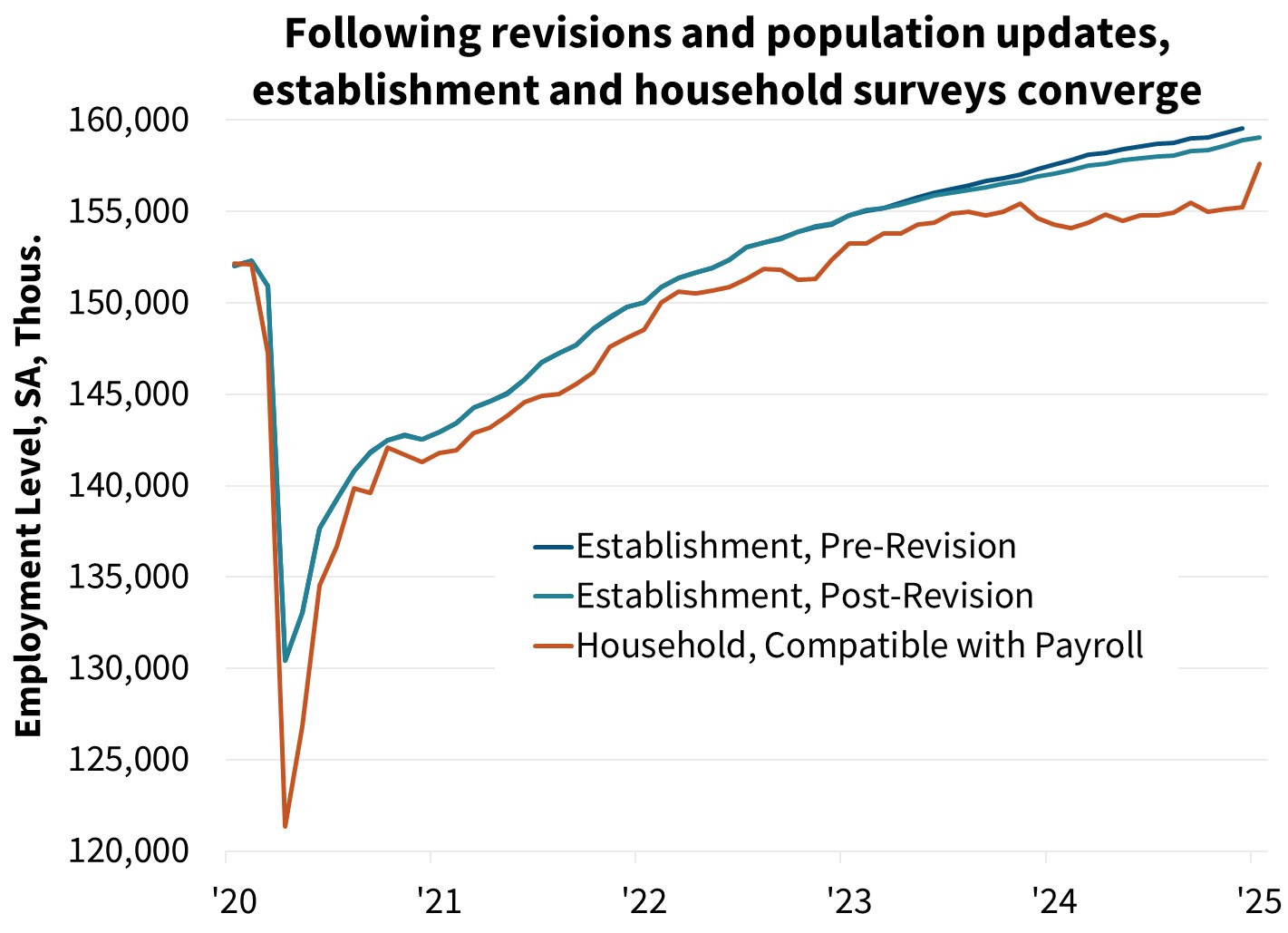

Nonfarm payroll employment growth surprised to the upside in January, rising by 143,000. The unemployment rate fell one-tenth to 4.0 percent. The prior two months had a combined upward revision of 100,000 jobs. The annual benchmarking process from the Bureau of Labor Statistics resulted in a downward revision, though it was not as large as expected and the pace of employment is now reported to have accelerated more quickly at the end of 2024.

Inflation & Monetary Policy

Inflation remains sticky, with the January CPI report showing an acceleration in both headline and core inflation. Our inflation outlook is now higher than last month; we now expect core inflation to end 2025 and 2026 at 2.9 percent YoY and 2.3 percent YoY, respectively. The impact of the tariffs on China was also minimal on our inflation outlook, only adding about a tenth to the CPI outlook in 2025.

In terms of monetary policy, we have lowered our fed funds rate expectation following the strong CPI and labor reports. We now expect that the Fed will cut the federal funds rate by 25 basis points just once in 2025, and we expect that to occur in September. The potential impacts of further tariffs, as well as a resilient economy, also leave open the potential for zero rate cuts in 2025, though a resumption of interest rate hikes also appears unlikely at this time.

Housing & Mortgage Forecast Changes

Mortgage Rates

Our mortgage rate forecast has been revised upward compared to last month given the rise in interest rates since our last forecast. We expect the 30-year fixed-rate mortgage to average 6.8 percent in 2025 and 6.5 percent in 2026 (up two-tenths and one-tenth, respectively, from our last forecast). However, interest rates remain volatile, particularly as the market attempts to adjust to changing expectations around Fed policy and other factors (see details above), which adds risk to our outlook.

Existing Home Sales

Existing home sales rose 2.4 percent to a SAAR of 4.245 million in December. Given the recent increase in purchase applications, our outlook for existing home sales was revised slightly upward through most of 2025, though it was revised down slightly in 2026 due to the increase in our mortgage rate forecast. We expect a lack of affordability and the lock-in effect to further limit the pace of sales for the foreseeable future.

New Home Sales

New single-family home sales rose in December, rising by 3.6 percent to a SAAR of 698,000. We have downwardly revised our new home sales outlook due to our higher mortgage rate outlook, but we continue to believe that the new home sales market will be a comparative bright spot in the housing market in 2025.

Single-Family Housing Starts

Our forecast for single-family housing starts was revised upward slightly in the near term following the increase in December, though our outlook was revised downward in 2026 due to our higher interest rate outlook.

Multifamily Housing Starts

Our multifamily housing starts forecast was revised upward following the strong December reading. While the multifamily starts series is notoriously volatile, we continue to believe demographic trends will be supportive of multifamily construction in the longer term once the current high levels of units in the construction pipeline are completed.

Single-Family Home Prices

Our quarterly single-family home price forecast, last updated in January, remains, by design, unchanged this month. Home prices grew 5.8 percent on a national basis in 2024. We project home prices will grow 3.5 percent in 2025 on a Q4/Q4 basis and 1.7 percent Q4/Q4 in 2026. Our next home price update will be in April.

")

Single-Family Mortgage Originations

This month, we have revised upward our expectations for 2025 single-family purchase origination volumes slightly to $1.4 trillion. As mentioned above, recent data on existing home sales has come in stronger than expected, pushing up our expectation for sales in 2025, leading to an upward revision to purchase originations. For 2026, we have revised volumes downward by 1 percent to $1.6 trillion, as a higher mortgage rate forecast is expected to increase the lock-in effect, dampening sales.

Meanwhile, we have downgraded the single-family refinance originations forecast again in February, as a result of higher actual mortgage rates in January and a higher expected path for the mortgage rate in this month’s forecast. In 2025, single-family refinance volumes are expected to be $464 billion, representing a downgrade of $32 billion from the January forecast. In 2026, we expect single-family refinances to be $650 billion, a downgrade of $43 billion from January's forecast. As seen in the Refinance Application-Level Index (RALI), while refinance applications have trended somewhat upward in recent weeks, they are still well below the recent uptick seen last September.

Economic & Strategic Research (ESR) Group

February 18, 2025

Data sources for charts: Federal Reserve Board, Bureau of Labor Statistics, Bureau of Economic Analysis, Policyuncertainty.com, Mortgage Bankers Association

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Mark Palim, SVP and Chief Economist

- Patty Koscinski, Economics Senior Director

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Eric Hardy, Economist

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst