Economic Developments - December 2024

For a PDF version of this report, click here.

As we approach the new year, we expect many trends from 2024 to continue in 2025, with housing affordability and the mortgage rate “lock-in effect” continuing to remain key challenges. Below, in addition to our economic and housing outlook, we also share five predictions for the housing market in 2025.

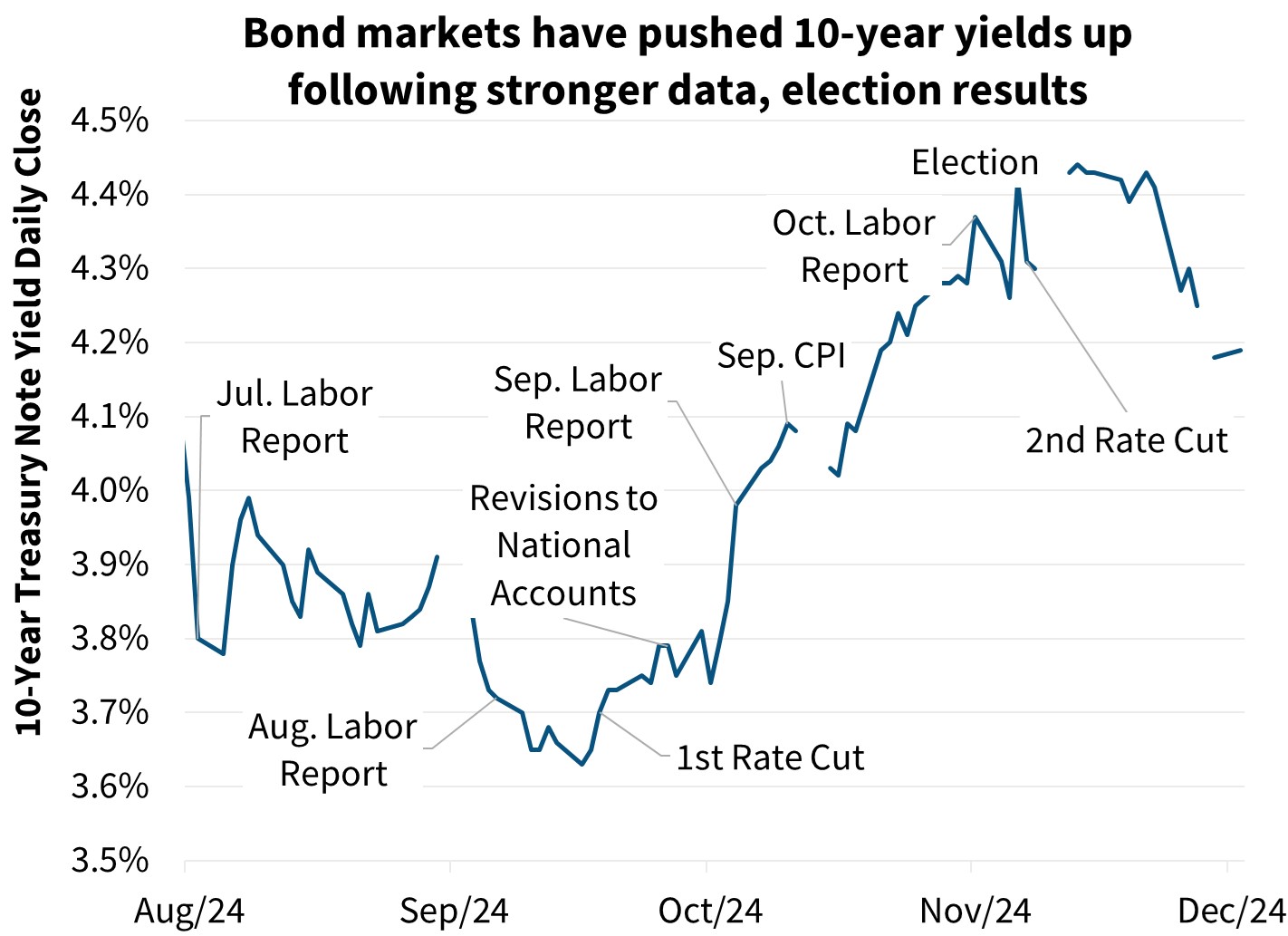

The economy appears poised to end 2024 on solid footing: Consumer spending has been resilient and, while the labor market is slowly cooling, unemployment remains low, and job growth is currently at a healthy pace based on demographic trends. Combined with inflation measures remaining stickier than markets expected earlier in 2024, we forecast no meaningful decline in the 10-year Treasury rate in 2025, which will keep mortgage rates elevated and home sales suppressed. This dynamic is occurring with a backdrop of uncertainty over whether solid labor productivity can continue to fuel growth next year, whether inflation will come in for a soft landing, or, if not, whether interest rates will remain structurally higher for longer.

Changes to immigration, trade, fiscal, and regulatory policies could all materially impact our outlook for economic growth, inflation, interest rates, and housing, though we have not incorporated any explicit policy changes in our forecast at this point as we await further details.

1. Average mortgage rates will decline modestly but remain above 6 percent, with likely bouts of volatility

We forecast the average mortgage rate to remain above 6 percent in 2025. Sticky inflation and an apparent stabilization in job market gains have lowered market expectations for future interest rate cuts. Unless economic growth starts to slow significantly, we expect mortgage rates to remain elevated relative to pre-pandemic levels, moving only slightly downward to around 6 percent by the end of 2025.

Our baseline expectation is for economic growth and employment gains to slow modestly next year and for core inflation to continue to ease — but not to reach the Fed’s target until 2026. Still, there is considerable upside risk to our economic forecast stemming from the potential for continued resilience in consumer spending and stronger-than-anticipated productivity growth. However, a meaningful slowdown in immigration flows or significant tariffs point to downside risk to economic growth and upside risk to inflation measures. Potential tax and regulatory policy changes present both upside and downside risks that may also impact interest rates.

2. Existing home sales will remain near 30-year lows, but location matters

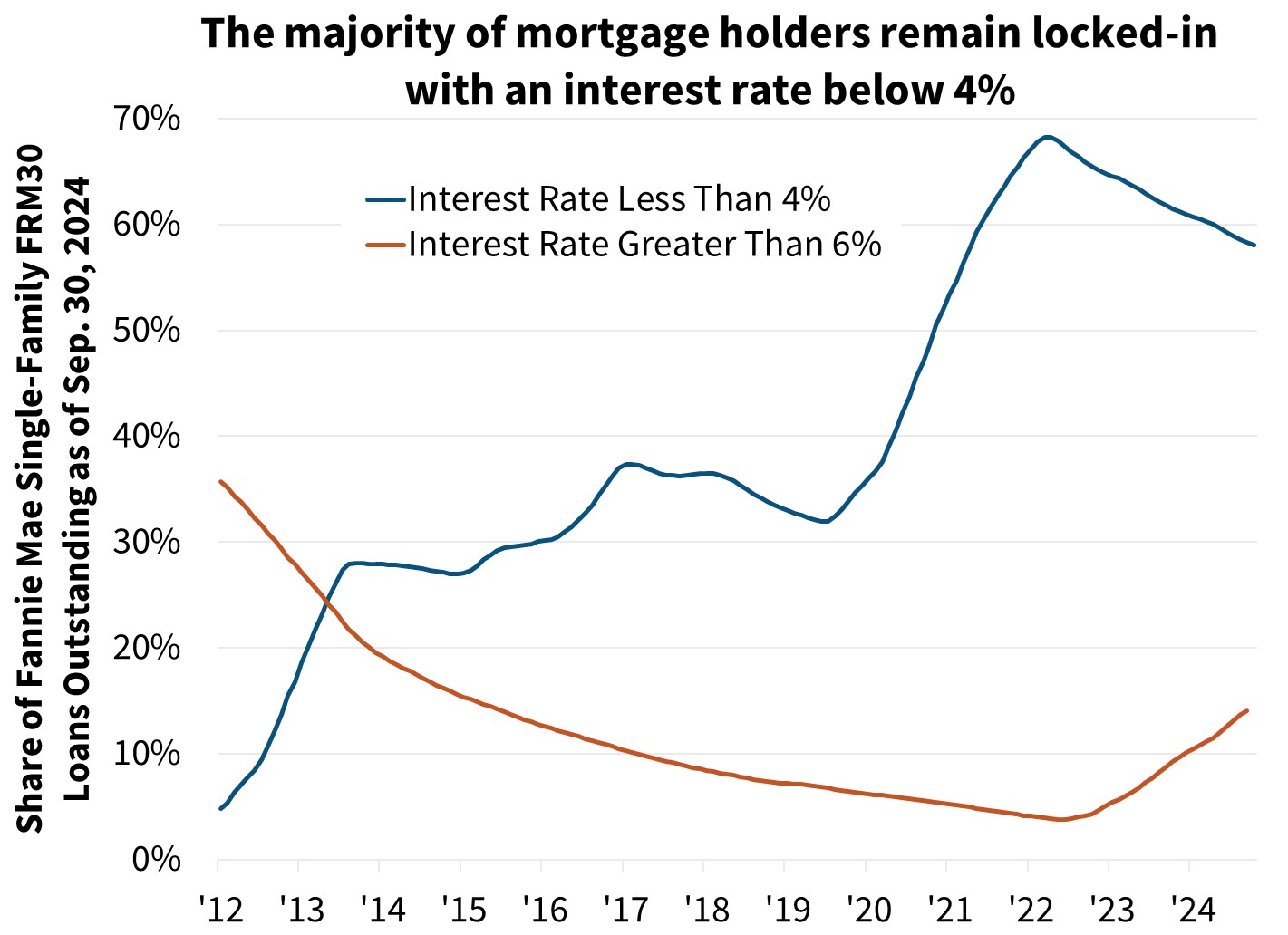

We forecast existing home sales to total 4.25 million in 2025, an improvement of 4.8 percent compared to our expected 2024 sales pace of 4.06 million, but still down 20.3 percent compared to 2019. We expect the increased inventory of homes available for sale will drive a modest improvement in existing home sales next year. According to the National Association of Realtors, the total number of homes available for sale at the end of November was 1.37 million units, up 19.1 percent from a year prior. However, given our mortgage rate outlook for rates to stay above 6 percent in 2025, we expect both constrained affordability conditions and the lock-in effect will continue to be the dominant themes limiting the recovery of existing home sales in 2025.

Even when interest rates briefly declined to around 6 percent in September, only a limited and brief pickup in mortgage applications and home sales occurred. Due to this muted response, we believe that mortgage rates near 6 percent are likely insufficient to spur enough additional demand or to encourage enough homeowners to sell, which is needed to thaw the housing market.

3. New home sales will remain a bright spot in the housing market (where they can be built)

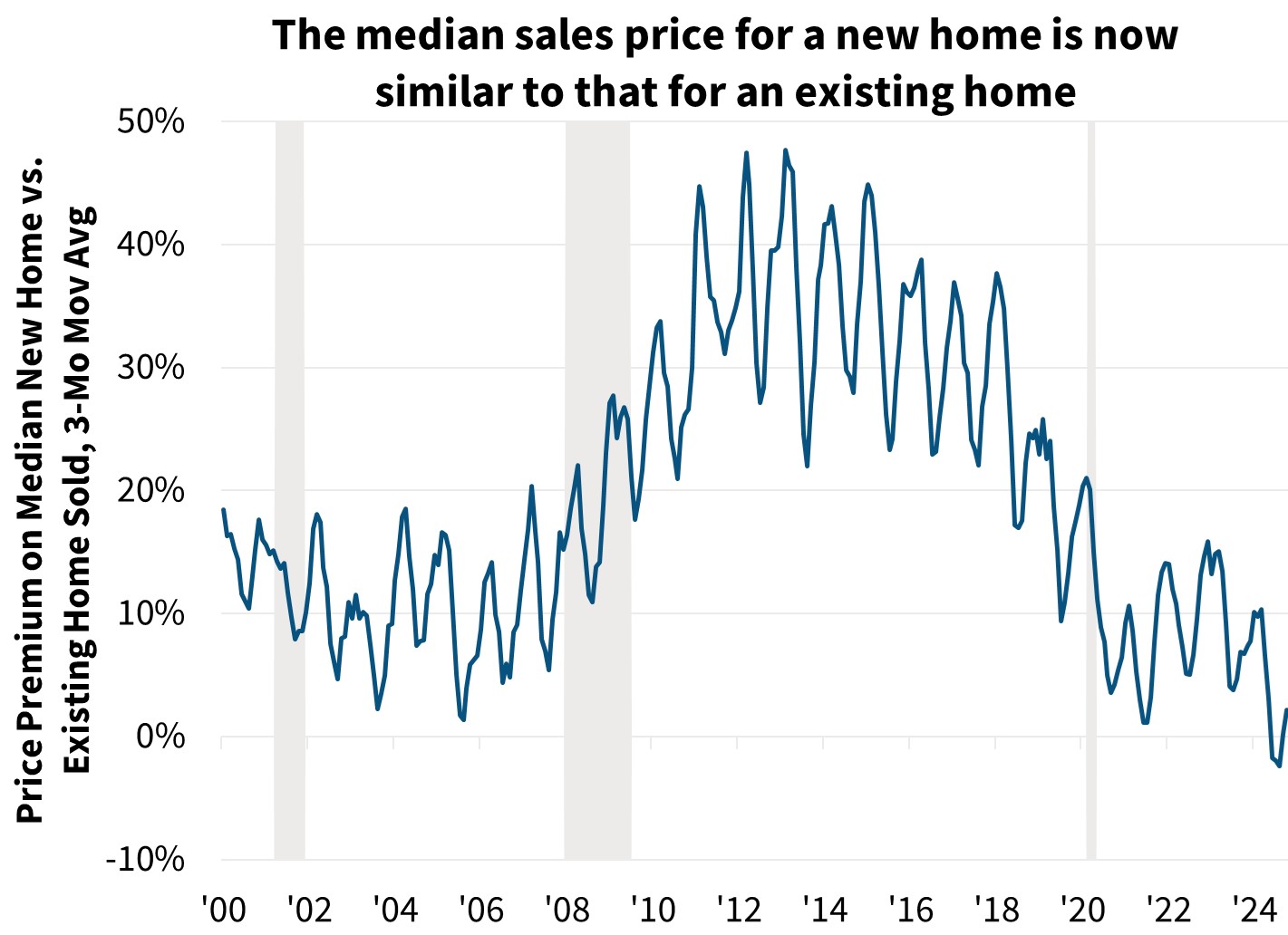

Whereas historically the median sales price on new homes has far exceeded the median sales price on existing homes, that gap has narrowed in recent years. The price premium between the median price on a new vs. existing home sold has averaged about 4 percent in 2024, compared to an average of 28 percent between 2015 and 2019.

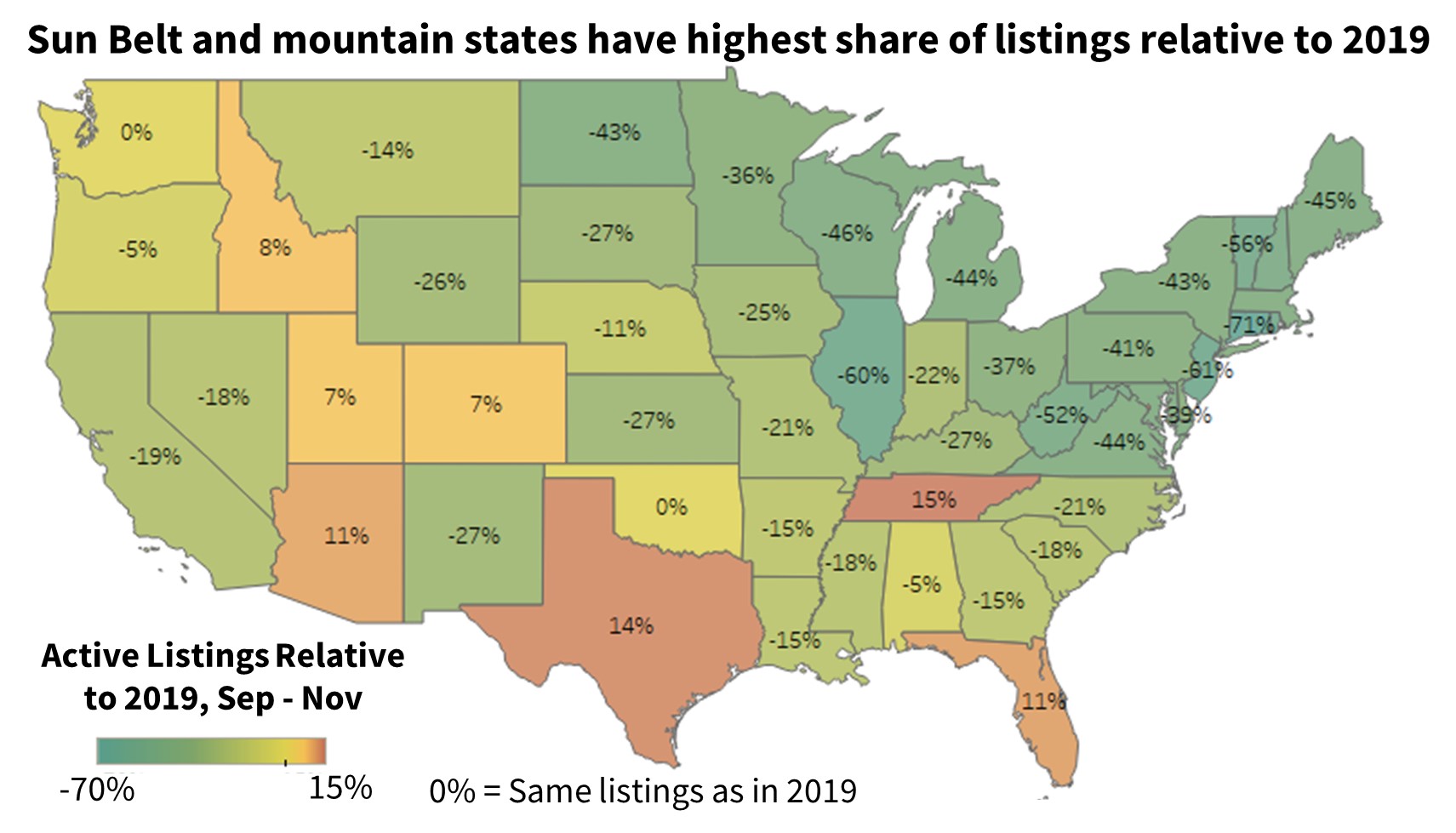

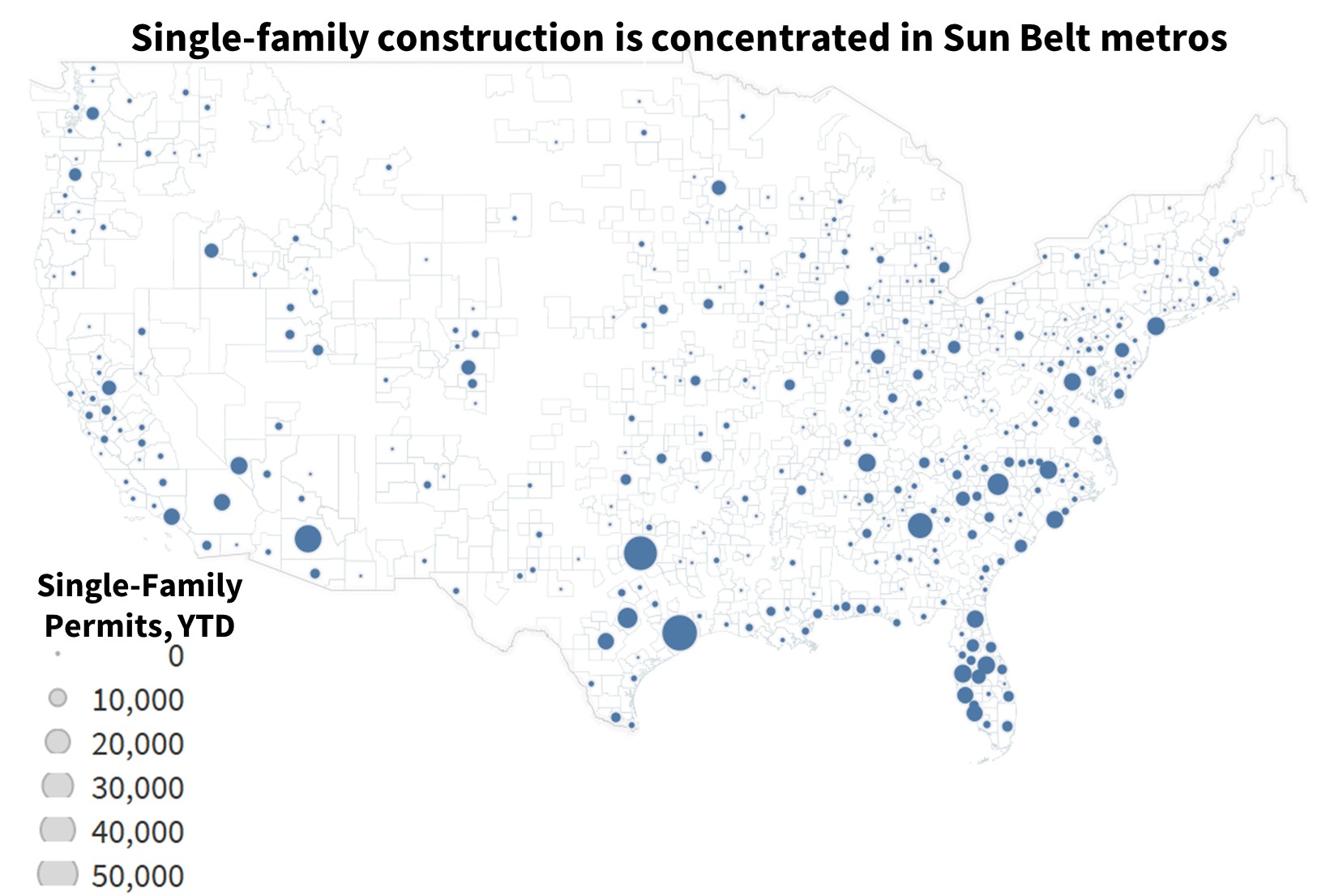

New home sales, however, vary greatly by region. The South and Mountain West are places where land and zoning allow for more construction and thus make up the bulk of sales. Of the roughly 750,000 single-family housing permits year-to-date through October, 20 percent were issued in the metropolitan statistical areas of Houston, Dallas, Phoenix, Atlanta, and Charlotte. In 2025, we expect the Sun Belt region will continue to see significant homebuilding activity.

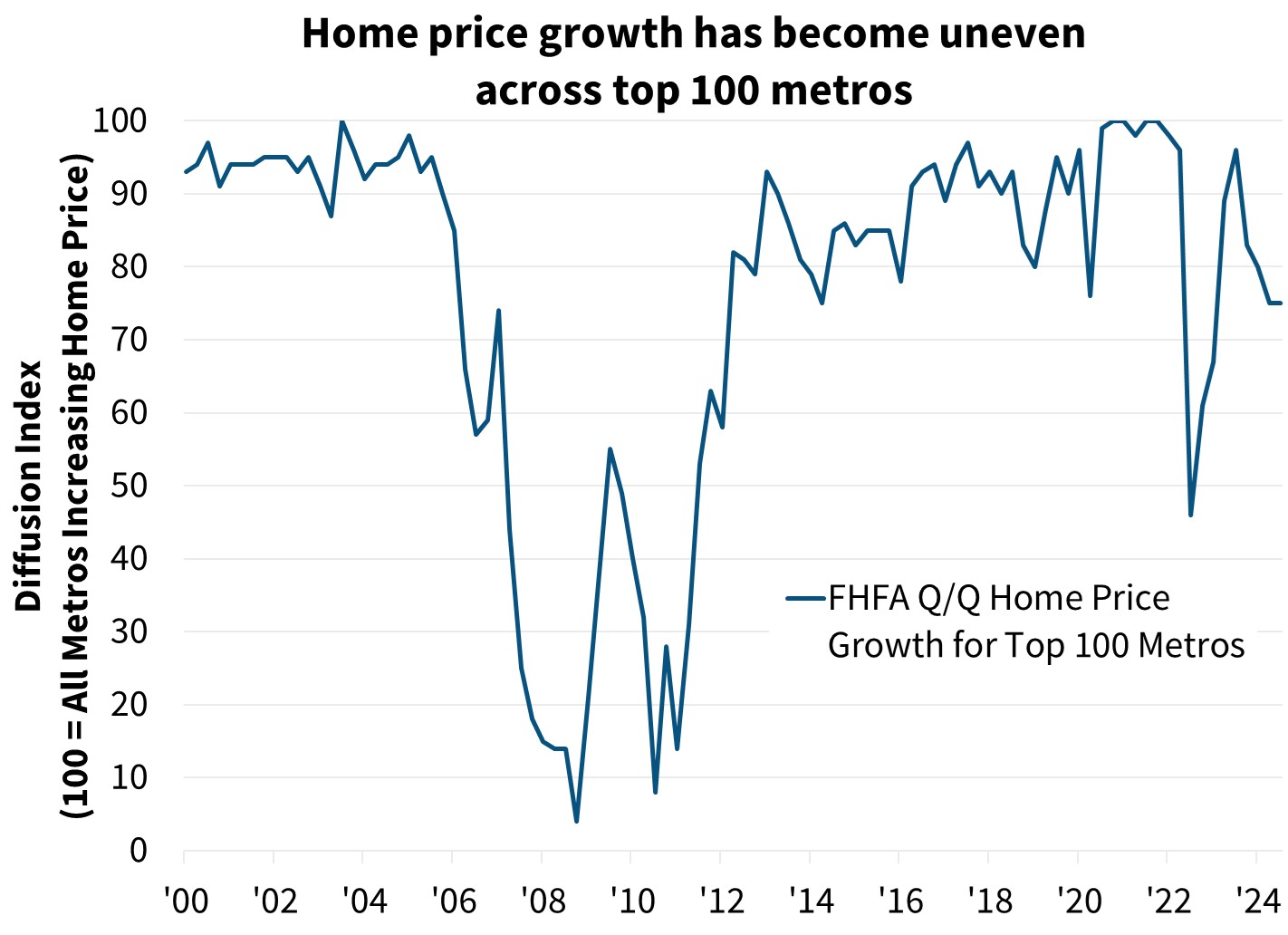

4. National home price growth will decelerate

While the continued lack of inventory for homes available for sale has helped to keep home price growth robust, we expect a continued deceleration in home price growth into 2025. We currently project year-over-year home price growth will be 3.6 percent in 2025 as measured by the Fannie Mae Home Price Index, compared to 5.8 percent in 2024. While mortgage rates will continue to present an affordability challenge, softening home price appreciation in 2025 could allow for nominal wage growth to exceed home price growth for the first time since 2011, helping to start a gradual improvement in homebuyer affordability conditions.

5. Multifamily housing will remain in a holding pattern

In the multifamily space, we expect 2025 to look a lot like 2024. While longer-term demographic trends remain supportive of multifamily construction over the next decade as the prime renter-aged population is expected to continue to grow, we expect below-average rent growth in the near term as additional units are completed. Depending on the measure, we expect rent growth to be between 2 and 2.5 percent in 2025. This will be helpful for renter affordability as it will represent the second-consecutive year of nominal wage growth exceeding rent growth in certain metros. However, slower rent growth will contribute to fewer new construction projects, especially in light of continued high longer-term interest rates.

Additionally, much of the regional variation present in single-family construction also applies to multifamily: Many of the Sun Belt metros experienced a building boom after the pandemic, and the growth in supply is affecting potential homebuyers’ buy-vs.-rent calculus. In many areas, renting is becoming more financially attractive than purchasing a home compared to several years ago, which means many would-be buyers are likely to decide to keep renting.

Economic Forecast Changes

Economic Growth

We’ve upgraded our Q4 2024 gross domestic product (GDP) growth expectation to a seasonally adjusted annualized rate (SAAR) of 2.3 percent, up three-tenths from the prior forecast, as consumption indicators remain robust. Our GDP forecast for total yearly growth in 2024 and 2025 on a Q4/Q4 basis was unchanged at 2.4 percent and 2.1 percent, respectively. Our forecast for 2026 is for growth of 2.1 percent Q4/Q4, one-tenth below the prior forecast.

Labor Market

Nonfarm payroll employment growth rebounded in November as expected, rising by 227,000, while the October and September employment figures were revised upward by a combined 56,000. The unemployment rate rose one-tenth to 4.2 percent. The jump in payroll employment growth is due to an end in strike activity and a rebound from disruptions caused by Hurricanes Helene and Milton. Our unemployment forecast was essentially unchanged from the last forecast.

Inflation & Monetary Policy

Core inflation remains sticky. Recent inflation indicators have come in largely in line with our expectations, therefore our outlook for year-over-year change in inflation is little changed.

In terms of monetary policy, our baseline expectation continues to be that the Fed will cut the federal funds rate by 25 basis points in December, followed by two 25-basis-point cuts in 2025.

Housing & Mortgage Forecast Changes

Mortgage Rates

Our mortgage rate forecast is largely unchanged compared to last month. We expect the 30-year fixed mortgage rate to average 6.7 percent in 2024 and 6.4 percent in 2025 (both unchanged from the prior forecast). We expect mortgage rates to average 6.1 percent in 2026, one-tenth lower than we forecast last month. However, interest rates remain volatile, particularly as the market attempts to adjust to changing expectations around Fed policy, which adds risk to our outlook.

Existing Home Sales

Existing home sales rose 3.4 percent to a SAAR of 3.96 million in October. Our outlook for existing home sales was revised upward modestly in 2024 and 2025, but notably downward in 2026. The near-term upward revision is due to a slightly lower near-term rate outlook and recently stronger purchase applications. However, our longer-term outlook in 2026 has been revised downward due to a reassessment of the persistence of the lock-in effect, which we expect to continue to suppress home sales for the foreseeable future.

New Home Sales

New single-family home sales fell sharply in October, likely due to hurricane disruptions, falling by 17.3 percent to a SAAR of 610,000. We have downwardly revised our near-term new home sales outlook due to this decline. In 2025, our outlook is essentially unchanged as we continue to believe that the new home sales market will be a bright spot in the housing market in 2025, though we expect a leveling off in new sales in 2026.

Single-Family Housing Starts

Our forecast for single-family housing starts is slightly weaker in the near term following the October new residential construction report, which saw single-family starts fall 6.9 percent, though this was likely exacerbated by hurricane-related disruptions. We have revised downward our outlook for 2026 in line with our new home sales outlook.

Multifamily Housing Starts

Our multifamily housing starts forecast was revised higher in the near term based on incoming data, though the rest of the path was essentially unchanged. While the multifamily starts series is notoriously volatile, we continue to believe demographic trends will be supportive of multifamily construction in the longer term once the current high levels of units in the construction pipeline are completed.

Single-Family Home Prices

Our quarterly single-family home price forecast, last updated in October, remains, by design, unchanged this month. We project home prices on a national basis will rise 5.8 percent in 2024 and 3.6 percent in 2025 on a Q4/Q4 basis. Our next home price update will be in January.

")

Single-Family Mortgage Originations

We currently expect purchase originations to be $1.3 trillion in 2024, essentially unchanged from last month’s forecast. In 2025, we expect purchase volumes to grow 12 percent to $1.4 trillion, representing an upgrade of $25 billion from the prior forecast as home sales are expected to be somewhat stronger in the near term compared to last month. However, our forecast for 2026 purchase volumes has been revised down by $54 billion from last month to $1.6 trillion, given the downgrades to the home sales path.

In the refinance market, volumes have been revised up given the slightly lower expected path for the mortgage rate, though these changes are slight compared to the prior month’s forecast. In particular, we expect refinance volumes to be $360 billion in 2024, $529 billion in 2025, and $724 billion in 2026, representing upgrades of about $30 billion in total from the prior month’s forecast.

Economic & Strategic Research (ESR) Group

December 11, 2024

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Federal Reserve Board, Fannie Mae, Census Bureau, Realtor.com, National Association of REALTORS®, Federal Housing Finance Agency

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Mark Palim, SVP and Chief Economist

- Doug Duncan, SVP

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Eric Hardy, Economist

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst