Economic Developments - May 2024

For a PDF version of this report, click here.

Our May forecast maintains our previous outlook for Q4/Q4 real Gross Domestic Product (GDP) growth of 1.8 percent in 2024 and 1.9 percent in 2025. We expect payroll growth to decelerate and the unemployment rate to drift upward to 4 percent by the end of the year. Longer-term interest rates, including mortgage rates, have been volatile the past two months – first rising in response to stronger than expected economic data, and then a more recent decline on weaker readings. Despite this, we view economic growth and inflation as being on the same track as our prior outlook, and we continue to anticipate moderation as the year progresses. We also continue to expect the Federal Reserve to implement the first of two rate cuts this year in September as inflation measures moderate, gradually trending toward the Fed's 2-percent target. However, we believe the Fed is likely to remain cautious as there are still signs that inflation may remain stickier than anticipated.

We revised modestly lower our total home sales forecast, primarily due to the higher mortgage rate forecast compared to last month's projection – although we still expect an upward trajectory in sales through our forecast horizon, and recent downward movements in mortgage rates following the conclusion of our interest rate forecast present slight upside risk to housing activity. We now project 2024 total home sales to be 4.89 million (4.96 million previously), followed by 2025 total sales of 5.29 million (previously 5.47 million). Consistent with the slower sales outlook, our forecast for total mortgage originations was downgraded modestly to $1.73 trillion for 2024 ($1.81 trillion previously) and $2.08 trillion in 2025 ($2.26 trillion previously).

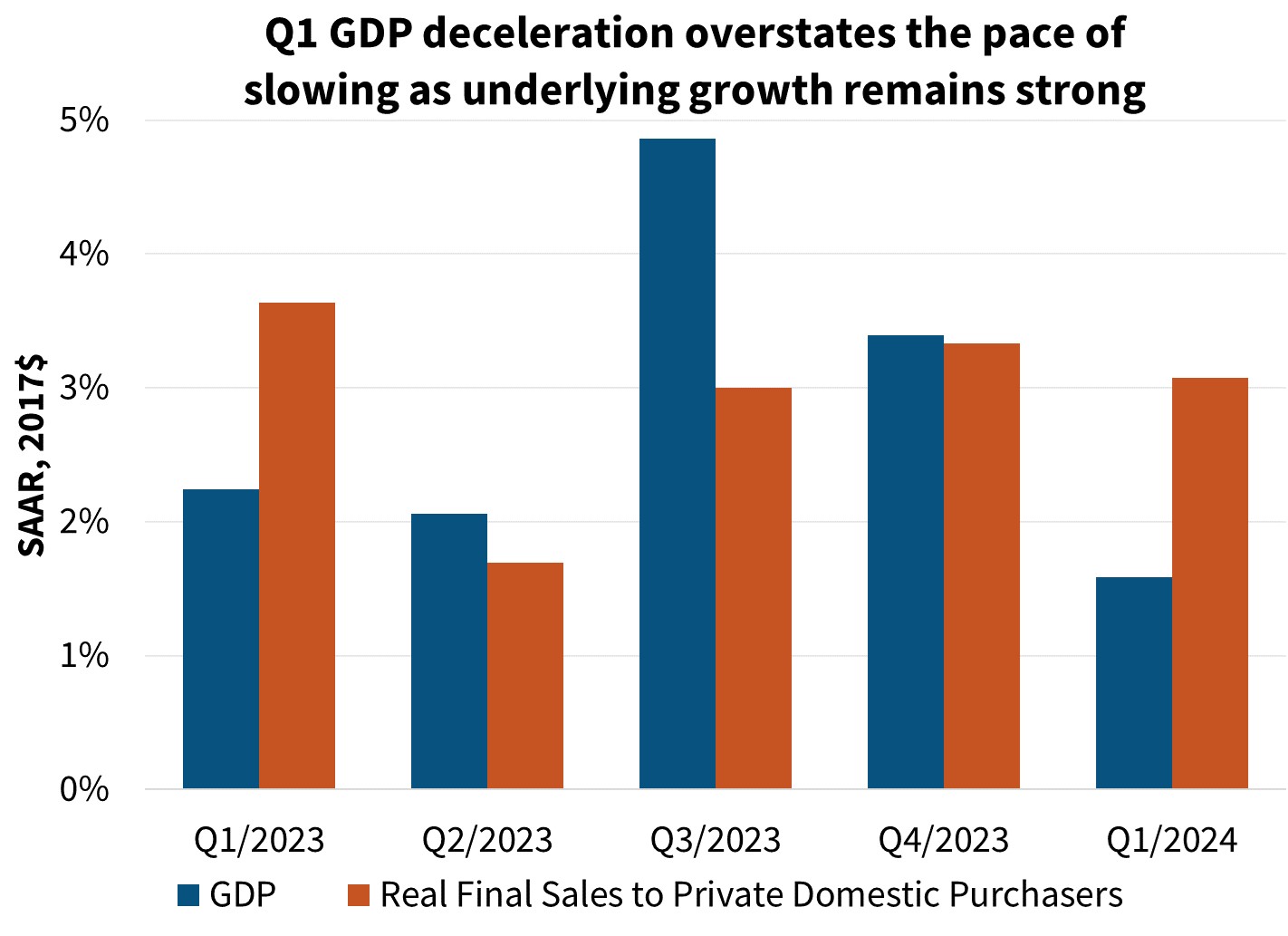

Underlying Growth Remained Steady Through Q1 but Slowing Still Likely

Putting aside near-term volatility, we do expect continued deceleration in growth as the year progresses. Strong consumer spending growth in February and March was not matched by income growth and, therefore, came at the expense of savings. We think growth in consumption is likely to slow, and the most recent pullback in core retail sales in April, which fell by 0.3 percent over the month, is supportive of this view. While revolving consumer credit balances remain normal relative to incomes, higher interest rates are likely putting some consumers under stress: Personal interest payments on all non-mortgage debt as a percentage of total personal outlays has been at its highest level since 2008 over the past three quarters, and recent data show an uptick in credit card and auto loan delinquencies. Additionally, we expect further softening in labor market conditions, which will likely limit consumption growth. The April employment report showed nonfarm payroll growth slowing to 175,000, a marked slowdown compared to the 269,000 average jobs added each month in the first quarter. While additional data will be necessary to definitively establish that the trend is slowing, a downshift in hiring would be consistent with other labor market indicators, such as the Job Openings and Labor Turnover Survey’s (JOLTS) job openings and quits rates, which have shown cooling labor market conditions for several months.

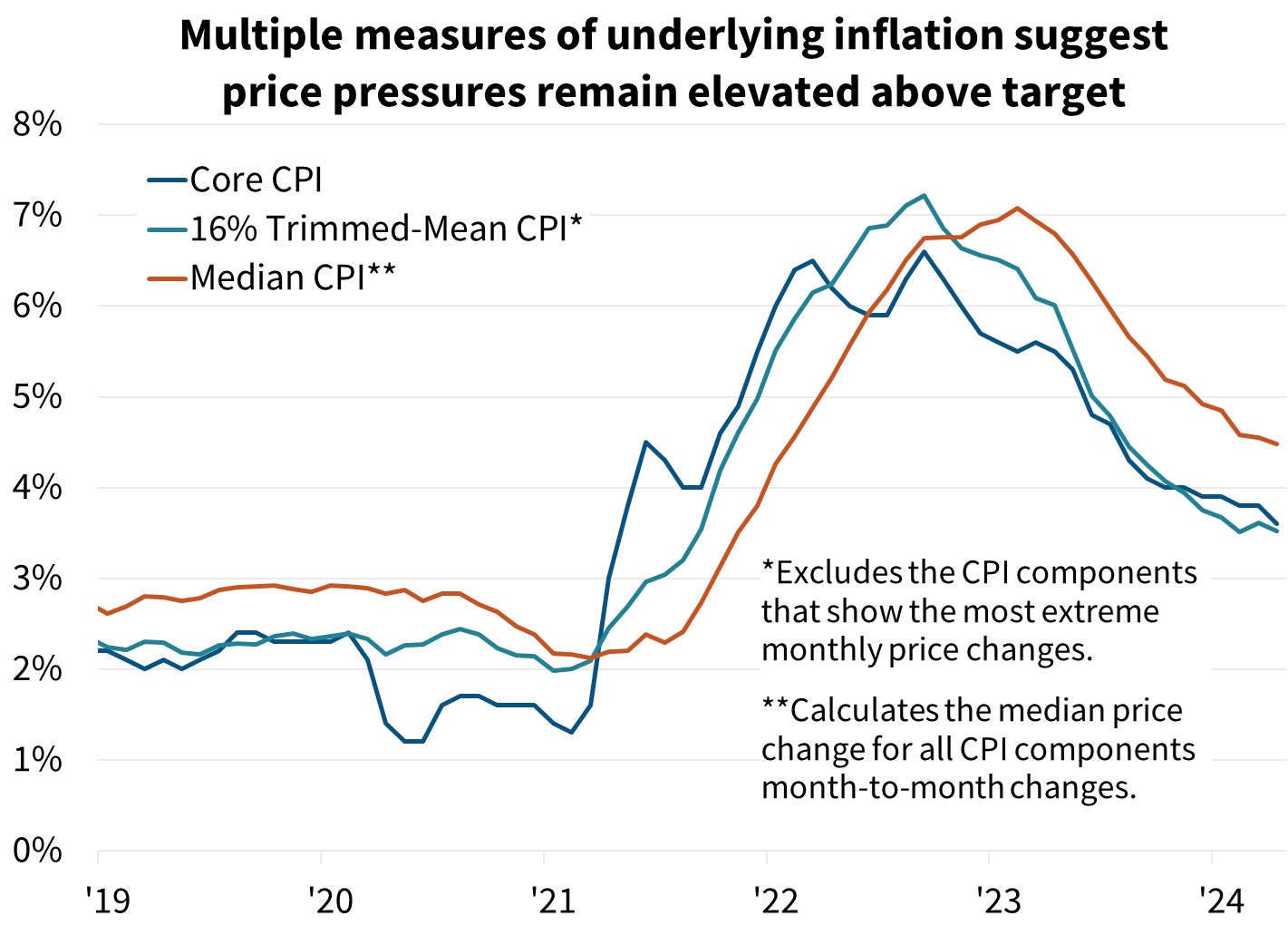

We believe the combination of softer labor market conditions and weaker consumption growth should flow through to lower inflation prints in the second half of the year. Further, we continue to expect measures of shelter inflation to weaken over time as measures of new tenant rents, including the Bureau of Labor Statistics’ (BLS) own series, show near-zero rent growth over the past two quarters. While these "fundamentals" point to decelerating inflation moving forward, releases to date have highlighted the risk that inflation pressures remain sticky. The Fed's preferred core Personal Consumption Expenditures (PCE) inflation averaged an annualized rate of 4.4 percent through the first three months of the year. While this strength can be explained away by idiosyncrasies in measuring items such as auto insurance and healthcare costs, alternative inflation measures, including the median Consumer Price Index (CPI), also point to some price stickiness that we believe will likely give the Fed and financial markets pause.

One thing we, and the market, expect at the March Federal Open Market Committee (FOMC) meeting is some discussion of the policy regarding their balance sheet. The Chair noted at the last press conference that it would be a topic of discussion at the March meeting.

Existing home sales fell back 4.3 percent in March to an annualized pace of 4.19 million, in line with our expectations. While we expect home sales to remain sluggish going forward, the flow of new listings has remained steady in recent months despite generally rising mortgage rates, suggesting that additional sizeable sales declines are unlikely. We suspect that, for a myriad of reasons, enough would-be sellers are deciding they can no longer put off moving. In April, the supply of active listings, according to Realtor.com, was up 30.4 percent from a year prior. While the higher mortgage rate forecast this month translates into a modest downgrade to 2024 sales, we see the flow of for-sale listings in the near term as being relatively resilient to recent mortgage rate moves. We forecast a modest drift upward in existing home sales over our forecast horizon.

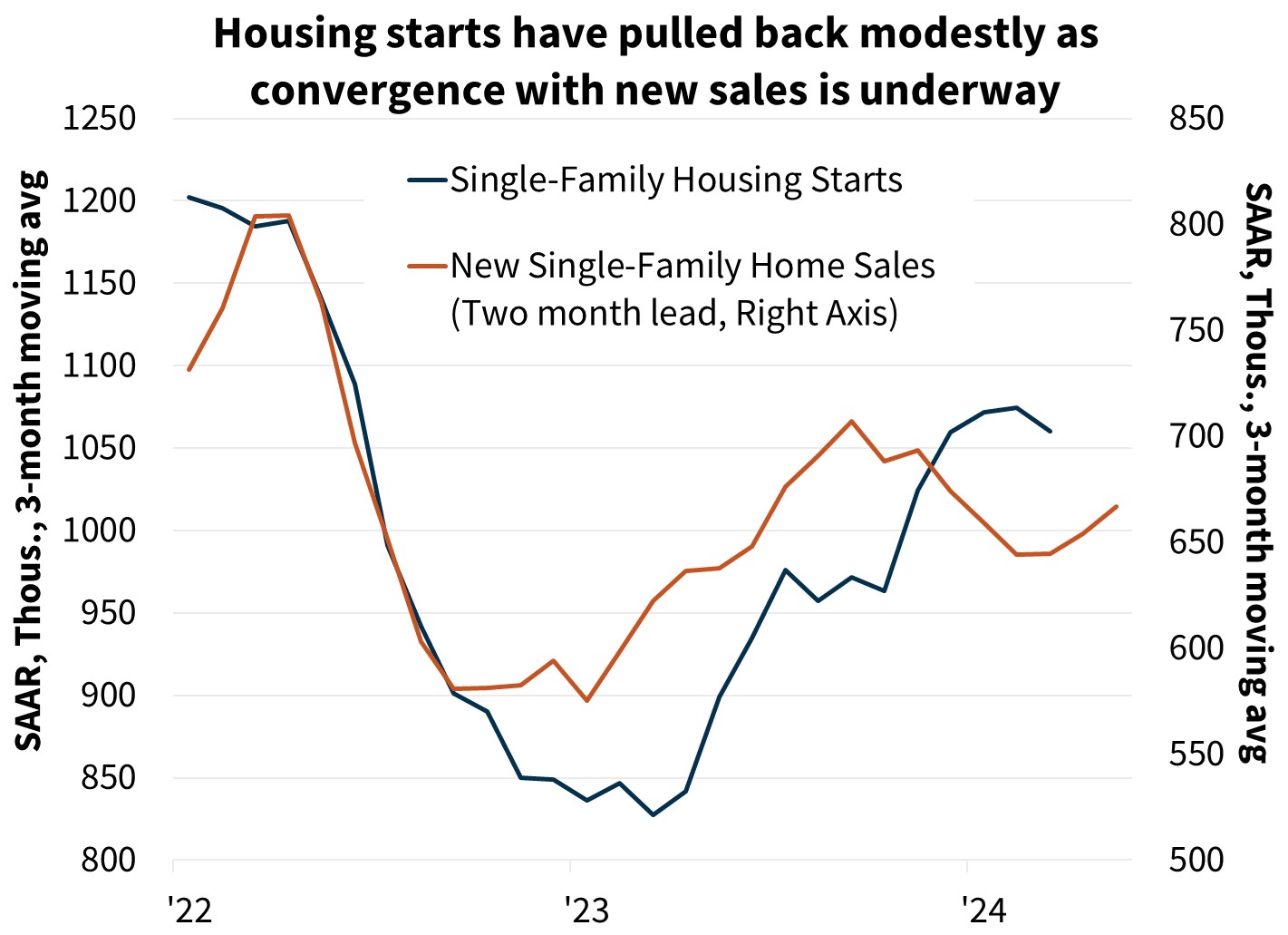

New home construction and sales look to be converging as expected. We had previously noted that the pace of starts has been elevated relative to the new home sales pace in recent months. Single-family starts fell in March by 8.7 percent, followed by a 0.4 percent decline in April, while new sales rose 8.8 percent in March. We expect this convergence to continue in the near term via a combination of homebuilders offering incentives to move existing inventories and a modest slowing in the pace of starts. While existing home sales listings are loosening somewhat, the housing market remains tight in most metros. As such, we continue to expect a solid pace of new home construction over the next two years as buyers look to new homes due to the limited existing home supply.

Economic Forecast Changes

Economic Growth

Q1 2024 GDP grew at an annualized 1.6 percent, well below the consensus and our estimate of 2.4 percent, with the difference driven mostly by net exports and the change in business inventories. Due to stronger “core” GDP we anticipate a rebound and, therefore, have revised upward our Q2 and Q3 forecasts, but our forecast for total yearly growth in both 2024 and 2025 is unchanged at 1.8 percent Q4/Q4 and 1.9 percent Q4/Q4, respectively.

Labor Market

Nonfarm payroll employment growth was 175,000 in April. The unemployment rate ticked up one-tenth to 3.9 percent. Compared to last month, we have lowered slightly our unemployment rate expectations consistent with a modest GDP growth upgrade in Q2 and Q3, though we continue to expect a gradual uptick over time. We continue to project the unemployment rate to gradually trend upward over the course of our forecast horizon.

Inflation & Monetary Policy

A lower near-term energy outlook led to a slight downward revision in the headline CPI outlook, though the persistent stickiness in the core measure of inflation led to a slight upward revision to our core inflation forecasts this month. However, we still forecast inflation to moderate over the outlook time horizon.

Our baseline expectation continues to be that the Fed will begin rate cuts in September, with only two rate cuts this year given the persistence of inflation and the robust labor market.

Housing & Mortgage Forecast Changes

Mortgage Rates

We revised our mortgage rate forecast upward month over month. We now forecast the 30-year fixed mortgage rate to average 7.0 percent in 2024 and 6.7 percent in 2025. However, interest rates remain volatile, particularly given changes in Fed policy expectations, which adds risk to our outlook. Following the completion of our start-of-the-month interest rate forecast, long-run rates have pulled back around 20 basis points, leading to some downside risk to our current baseline mortgage rate forecast.

Existing Home Sales

Existing home sales fell to a seasonally adjusted annualized rate (SAAR) of 4.19 million in March. We revised modestly downward our forecast through 2025, mostly driven by the change in mortgage rate expectations. While we expect a pullback in Q2, due to a strong start at the beginning of Q1, we continue to forecast existing sales to trend upward over our forecast horizon on a monthly sequential basis.

New Home Sales

New single-family home sales jumped 8.8 percent in March to a SAAR of 693,000. Similar to our existing home sales outlook, we have lowered our expectations for new home sales primarily due to the higher interest rate outlook. However, new home sales continue to benefit from the limited inventory of existing homes for sale, which we expect to support demand for new homes over our forecast horizon.

Single-Family Housing Starts

We continue to expect that the lack of existing homes available for sale will continue to boost new home construction in the medium term, though we have lowered our expected starts pace over the forecast horizon due to the higher interest rate path.

Multifamily Housing Starts

We have downgraded our forecast through the forecast horizon, as we believe multifamily starts remain likely to decline due to muted national rent growth, the large number of multifamily units near completion, and a higher interest rate outlook.

Single-Family Home Prices

Home prices grew 6.6 percent Q4/Q4 in 2023, according to the most recently published non-seasonally adjusted Fannie Mae Home Price Index (HPI) and are forecast to rise 4.8 percent in 2024 and 1.5 percent in 2025 on a Q4/Q4 basis. Our next home price update will be in July.

")

Single-Family Mortgage Originations

We have revised downward our expectation for purchase originations this month, consistent with the upward revisions to our mortgage rate forecast. In particular, we now expect market purchase volumes to be $1.4 trillion in 2024, representing 14 percent growth from 2023 but a downward revision of $35 billion from last month's forecast. In 2025, we expect purchase volumes to grow a further 13 percent.

For refinances, we have revised downward our expectation for 2024 volumes to $368 billion, $47 billion lower than the prior months' forecast, with revisions again driven by the higher mortgage rate expectation. This higher interest rate path has also caused us to revise downward refinance volumes in 2025, to $539 billion.

Economic & Strategic Research (ESR) Group

May 16, 2024

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Census Bureau, National Association of REALTORS, Federal Reserve, Freddie Mac, Fannie Mae

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Doug Duncan, SVP and Chief Economist

- Mark Palim, VP and Deputy Chief Economist

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst