Economic Developments - March 2025

For a PDF version of this report, click here.

- We now expect mortgage rates to end 2025 and 2026 at approximately 6.3 percent and 6.2 percent, respectively, each downward revisions of three-tenths from our prior forecast.

- For home sales, the lower mortgage rate forecast offsets the softer economic outlook (see below). We have revised upward our outlook for total home sales to 4.95 million in 2025, up slightly from 4.90 million in our prior forecast.

- Single-family mortgage originations are expected to total $1.94 trillion and $2.28 trillion in 2025 and 2026, respectively. These represent slight upward revisions from our prior forecast.

- Incoming data and greater clarity on trade policy has led us to reduce our growth outlook for 2025 to 1.7 percent (2.2 percent previously) and 2026 to 2.1 percent (previously 2.2 percent), with modest corresponding impacts to our labor market forecast.

- Inflation, as measured by the Consumer Price Index (CPI), is now expected to end 2025 at 3.2 percent on a Q4/Q4 basis. This is an upward revision from 2.8 percent in our prior forecast that largely reflects the expected pass-through of tariffs to consumer prices, though the impact is partially offset by slower economic growth and a downward revision to the energy price outlook.

Economic Growth Downgraded, Near Term-Inflation Revised Upward

We have revised downward our 2025 and 2026 growth outlooks from 2.2 percent for each year to 1.7 percent and 2.1 percent, respectively. This coincides with an upward revision to our inflation outlook for 2025, followed by a slight downward revision for 2026.

The major drivers of the changes to our economic outlook this month are:

- An updated assumption on tariffs to reflect current policy. Our previous forecast included the prior 10-percent China imports tariff increase, which went into effect last month. In our March outlook, we have included the since-implemented additional 10-percent tariff on imports from China (a total of 20 percent in total compared to tariff levels in 2024) and approximately half of the announced 25-percent tariffs on goods from Canada and Mexico, in line with the current implemented policy that exempts approximately half of goods currently subject to the United States-Mexico-Canada Agreement (USMCA).

Weaker consumer spending. Real personal consumption expenditures fell 0.5 percent over the month, the largest decline since February 2021. While we had expected that consumer spending would downshift from the robust 4.2 percent annualized growth rate set in Q4 (as it had outpaced income growth), the January figure was weaker than we had expected. We think the sharp contraction in January spending data was likely overstated due to volatility around the holiday shopping season, California wildfires, and unusually cold and snowy weather in other parts of the country. As such, while we are downgrading our Q1 personal consumption forecast from 3.1 percent to 2.1 percent annualized, this is a less significant downgrade for the quarter than would otherwise be suggested by the January consumption data alone.

Looking forward, we expect weaker wealth effect-driven consumption. While the recent pullback in equity prices as of this writing is not out of the ordinary, we believe continued resilience in consumer spending in 2024 was in part driven by strong stock market appreciation, leading to wealth effect-driven consumption gains, coinciding with a continued low personal savings rate. This tailwind for consumer spending is potentially no longer as strong. Consistent with this are weaker measures of consumer sentiment and recent comments during earnings reports from major retail and food service firms pointing to consumer softness. Taken together, we now expect a slower pace of consumer spending growth in coming quarters, as well as sluggish investment spending.

- Lower energy prices expected to partly offset the impact on inflation from higher tariffs. In the near term, lower energy prices that had been projected in our prior month’s forecast are expected to partially offset the near-term upward pressure to inflation measures related to tariffs. However, by the end of 2025, we expect the CPI to be at 3.2 percent before decelerating meaningfully in 2026 as the bump from tariffs passes.

In addition, we note that measures of uncertainty and market volatility have risen meaningfully this quarter. That greater uncertainty includes the likely path of fiscal, monetary and other policy developments, but also how firms and consumers respond to them and other financial market developments. There are plausible upside and downside risks to both growth and inflation measures over our forecast horizon, as well as to interest rates.

Modestly Lower Mortgage Rate Outlook

While the growth outlook has softened, we expect the upward pressure on price measures from tariff dynamics may lead to the Federal Reserve taking a wait-and-see approach as it seeks to balance its dual mandate for full employment and price stability. Federal Reserve Chair Jerome Powell recently stated that they “do not need to be in a hurry” to cut interest rates. As such, we project only one rate cut in September, followed by two additional cuts in 2026, though, again, there is both upside and downside risk here, too.

Housing Outlook Remains Little Changed, for Now

Historically, interest rate effects tend to be the dominant factor in driving home sales fluctuations compared to economic growth. Aside from credit crunch events, such as the Great Financial Crisis, home sales typically start rising – even amid economic contraction and weakening employment – if mortgage rates are falling. As such, we expect the modest pullback in mortgage rates to have a stronger positive effect to sales than the weakening of sentiment and a slower growth outlook. Therefore, combined with January existing home sales coming in near our expectations, we have slightly revised upward our existing home sales outlook for 2025 and 2026.

Regarding new home sales and construction, there is additional risk to starts stemming from upward pricing pressures related to tariffs on lumber and other materials. The National Association of Home Builders recently estimated the increased costs of lumber and other goods could raise the cost of constructing a typical home by about $10,000. However, lower mortgage rates would also give homebuilders some additional support by not having to offer as steep concessions and rate incentives to drive sales, and the net effect may be to keep homebuilders’ margins steady. As such, we have only made minor revisions to our new home sales and starts outlooks, largely reflecting incoming recent data.

Economic Forecast Changes

Economic Growth

Our March forecast incorporates the recently weaker Q1 economic data, including lower personal consumption, changes in trade policy since our February forecast, and corresponding financial market reactions and sentiment surveys. Taken together, we have downgraded our growth outlook for 2025 by five-tenths to 1.7 percent Q4/Q4 and for 2026 by one-tenth to 2.1 percent Q4/Q4.

Labor Market

Nonfarm payroll employment growth remained healthy in February, rising by 151,000 jobs. The unemployment rate rose one-tenth to 4.1 percent. Our unemployment outlook was unchanged at 4.2 percent for 2025, though we revised it upward a tenth to 4.4 percent in 2026 due to the weaker growth outlook.

Inflation & Monetary Policy

Our inflation forecast now calls for higher year-over-year growth in the latter half of 2025 and the first half of 2026. We now expect core inflation to end 2025 and 2026 at 3.3 percent year over year and 2.2 percent year over year, respectively. This result includes the already-enacted tariffs as well as our lowered oil price forecast, which counteracts some of the expected price increases in the near term.

In terms of monetary policy, we maintain our view that the Fed will cut the federal funds rate by 25 basis points just once in September. However, we have added two 25-basis point rate cuts to our forecast in 2026.

Housing & Mortgage Forecast Changes

Mortgage Rates

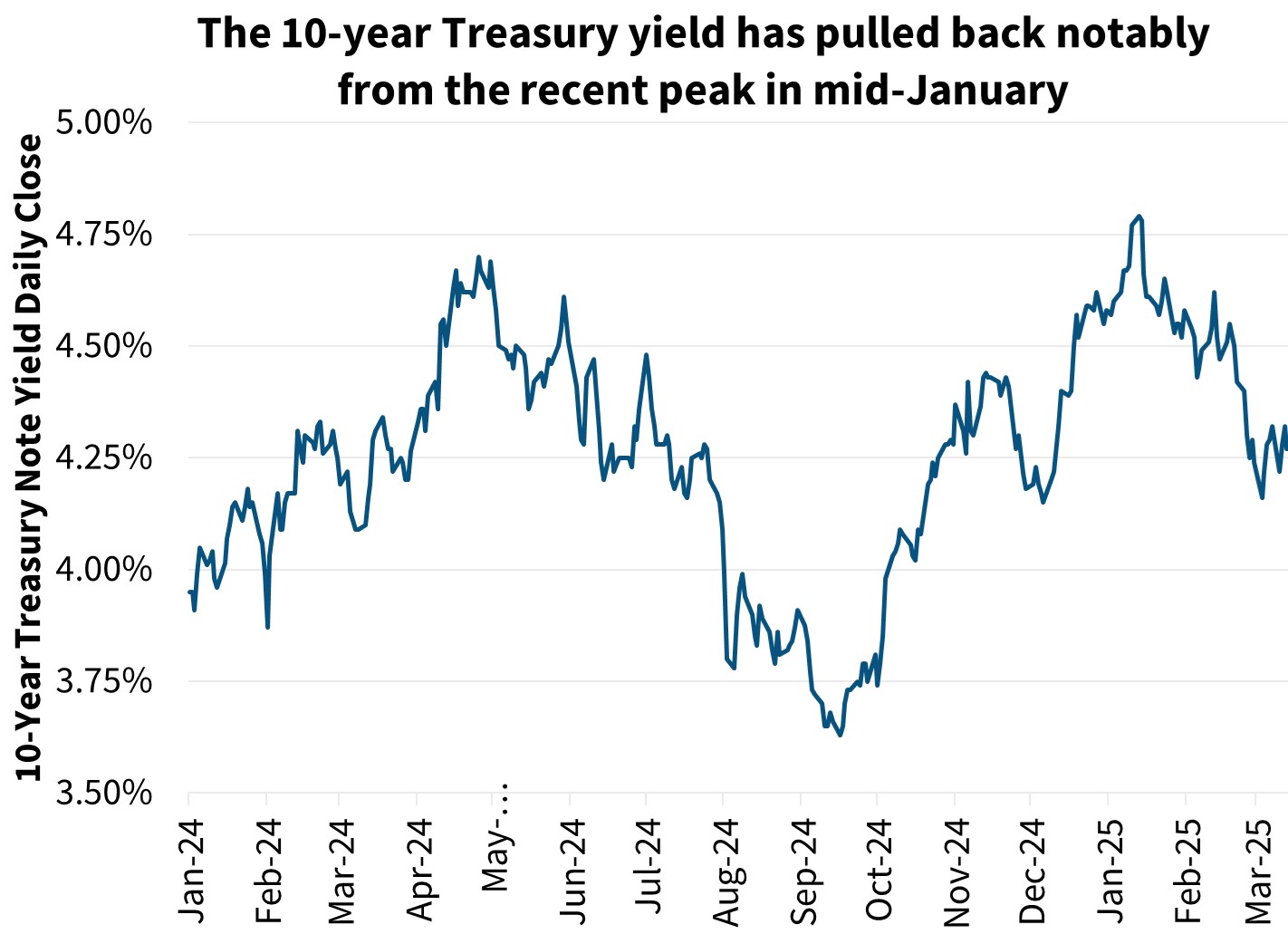

Our mortgage rate forecast has been revised downward given the recent movements in the mortgage rate. We now expect the 30-year fixed-rate mortgage to average 6.5 percent in 2025 and 6.2 percent in 2026 (both down three-tenths from our February forecast). However, there is an unusually high degree of uncertainty regarding the path for growth and inflation during the rest of 2025, which adds risk to our interest rate forecasts.

Existing Home Sales

Existing home sales fell 4.9 percent to a seasonally adjusted annual rate (SAAR) of 4.08 million in January, essentially in line with our Q1 forecast. Our outlook has been revised slightly upward given our lower mortgage rate forecast, though the decline in purchase applications and in pending home sales highlights the challenges that the housing market continues to face as affordability challenges and the lock-in effect remain persistent headwinds, even with some improvement in mortgage rates.

New Home Sales

New single-family home sales dropped sharply in January, falling by 10.5 percent to a SAAR of 657,000. We have made a slight downward revision to our near-term outlook given the lower growth outlook.

Single-Family Housing Starts

Despite the decline in single-family housing starts in January, our forecast for single-family housing starts was essentially unchanged, as data on single-family permits, typically more indicative of the underlying trend, was in line with our Q1 forecast.

Multifamily Housing Starts

Our multifamily housing starts forecast was mostly unchanged in the near term but revised slightly downward in 2026. Slow rent growth and nearly 1 million multifamily units already under construction continue to suggest multifamily construction will be subdued this year.

Single-Family Home Prices

Our quarterly single-family home price forecast, last updated in January, remains, by design, unchanged this month. Home prices grew 5.8 percent on a national basis in 2024. We project home prices will grow 3.5 percent in 2025 on a Q4/Q4 basis and 1.7 percent Q4/Q4 in 2026. Our next home price update will be in April.

")

Single-Family Mortgage Originations

We have modestly revised upward our expectations for single-family purchase originations this month given the more optimistic path for home sales as a result of our lower mortgage rate forecast. In particular, we now expect purchase volumes to grow by 10 percent year over year in 2025 to $1.4 trillion, representing an upgrade of $12 billion from last month’s forecast. Purchase volumes are expected to grow a further 10 percent to just under $1.6 trillion in 2026, an upgrade of $16 billion from the prior forecast.

We have also revised upward our expectations for single-family refinance originations, again driven by the lower mortgage rate forecast this month, as well as the recent up-tick in applications as indicated by the Fannie Mae Refinance Application-Level Index (RALI). We now expect refinance activity to total $502 billion in 2025, an upgrade of $38 billion from last month’s forecast, growing further to just under $700 billion in 2026.

Economic & Strategic Research (ESR) Group

March 14, 2025

Data sources for charts: Federal Reserve Board, Bureau of Economic Analysis

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic and Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR Group bases its opinions, analyses, estimates, forecasts, beliefs, and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current, or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR Group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Mark Palim, SVP and Chief Economist

- Patty Koscinski, Economics Director

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Eric Hardy, Economist

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst