Economic Developments - January 2025

For a PDF version of this report, click here.

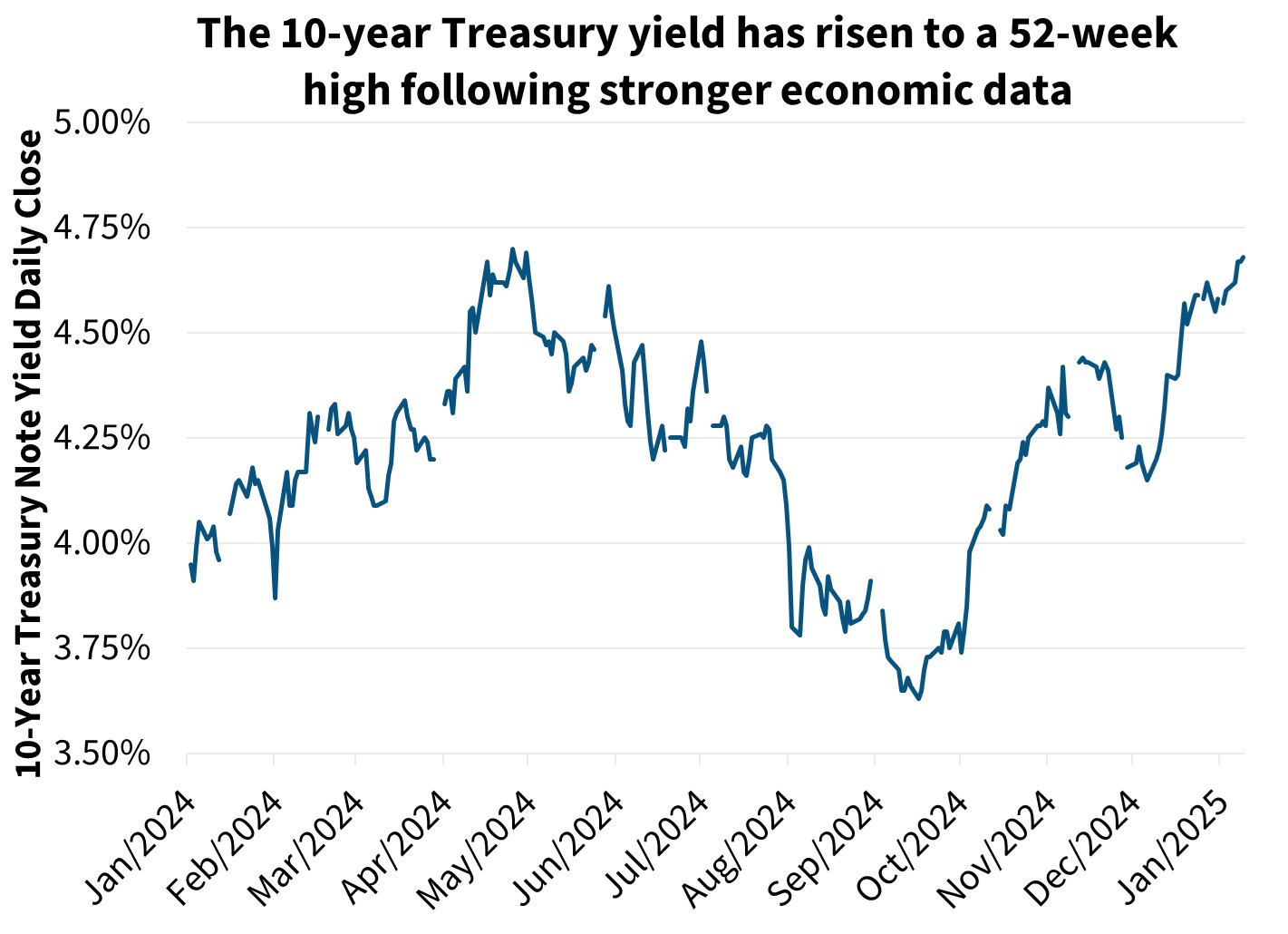

Longer-term interest rates have risen in recent months even as the Fed continued to cut the short-term rate at its December meeting. This divergence reflects the bond market’s repricing based on updated expectations for fewer additional rate cuts over the coming years in response to incoming economic and other data. Though we think the increase in longer-term rates is, in part, reflective of recent data pointing to continued momentum in economic growth, the rise in the 10-year Treasury, and therefore mortgage rates, reduces the prospects of a meaningful home sales recovery in 2025. As a result, both affordability challenges and lock-in effects will persist, hindering sales.

Incorporating both an upward revision to our mortgage rate forecast and a downward revision to our home sales outlook results in a downward revision of our single-family mortgage originations forecast to $1.92 trillion in 2025 (previously $1.97 trillion) and $2.27 trillion in 2026 (previously $2.37 trillion). This follows estimated originations of $1.69 trillion in 2024.

Our outlook for economic growth is effectively unchanged from last month. We now expect 2025 real gross domestic product (GDP) growth to be 2.2 percent on a Q4/Q4 basis (previously 2.1 percent), and 2026 growth to be 2.0 percent (previously 2.1 percent). Notably, we have upwardly revised our top-line inflation expectations for 2025 by 0.4 percent at end of year, largely due to a stronger energy price outlook. Core inflation, in contrast, is still expected to decelerate slowly through 2026, unchanged from our prior outlook.

It should be noted that we continue to make no explicit assumptions in our forecast regarding potential changes to trade, fiscal, and immigration policy as we await greater clarity. This is a source of both upside and downside risks to our growth, inflation, and housing outlooks.

Resilient Economic Activity and Sticky Inflation Point to Interest Rates Staying Higher for Longer

While a mix of "hot" and "cool" economic reports have driven some of the recent interest rate volatility, the overall picture shows that economic growth remained resilient over 2024, and that deceleration in inflation stalled in the latter half of the year. After slowing for much of 2024, December's labor report showed payroll growth jumping to 256,000 (up from a past six-month average of 142,000) and a decline in the unemployment rate to 4.1 percent, suggesting that the labor market may have firmed to end 2024. Meanwhile, measures of holiday shopping spending and personal consumption remain solid. Annual inflation as measured by the core Consumer Price Index (CPI) averaged around 3.3 percent over the second half of 2024 (though dipped to 3.2 percent in December), and the core Producer Price Index (PPI) has stabilized at a higher-than-pre-pandemic level, as measured on an annual basis.

The totality of indicators in recent months suggests that neither aggregate demand in the economy nor inflation pressures eased by as much as was previously expected. This implies that the current monetary policy stance is not restricting economic activity as much as previously thought, and, possibly, that the “neutral” short-term interest rate, where monetary policy is neither supporting nor restricting growth, is higher than the bond market and the Fed had anticipated.

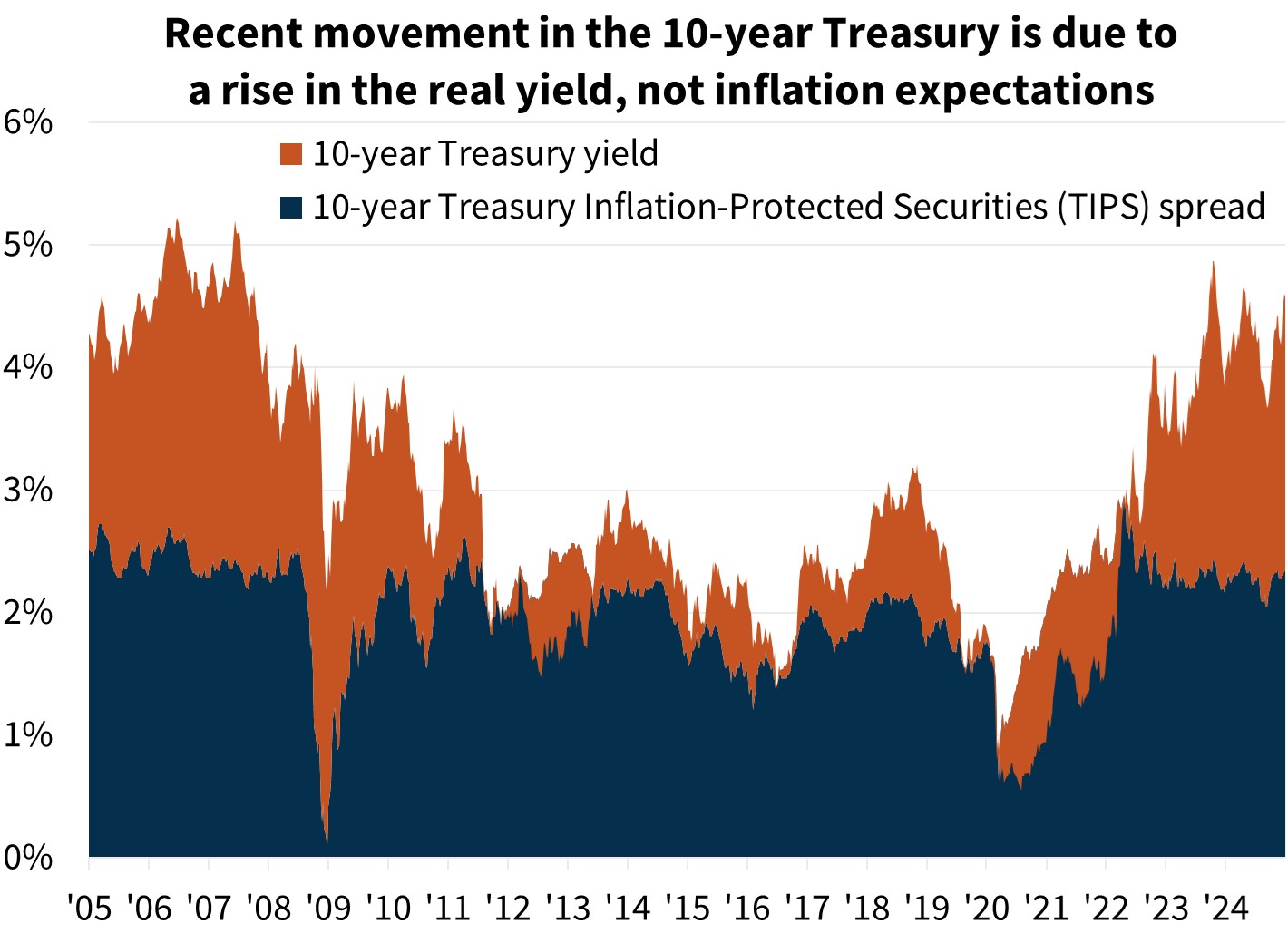

As a result, fed funds futures markets have increased the expectation for the year-end 2026 fed funds rate from around 2.9 percent this past September to 3.9 percent as of this writing — a reduction in the expected amount of total rate easing. The Fed has also indicated an upward shift in its views on the trajectory of future short-term rates in its Q4 Summary of Economic Projections (SEP). In September, the median participant expected the federal funds rate to be 2.9 percent by the end of 2026, while the December SEP had that figure at 3.4 percent. Given that long-term rates are a function of expected short-term rates over time, the 10-year Treasury yield has risen.

This indicates that bond markets still expect the Fed’s 2-percent inflation target to be achieved, and on a similar timeframe as before. However, the expected path for the fed funds rate going forward, required to achieve that goal, is now higher than previously expected after observing economic activity not slowing by as much as previously expected.

We are still expecting GDP growth to moderate in 2025 relative to 2024 but have only modestly revised our GDP forecast this month given incoming data and the recent rise in rates corresponding with apparent higher growth resiliency. Primarily, we modestly upgraded consumer spending over our forecast horizon. Largely offsetting this is a related wider trade deficit projection, and a modest downward revision to our expectation for housing investment, which is particularly interest rate-sensitive. Top-line inflation numbers in this forecast are modestly higher due to a higher expected energy price path, though the core inflation outlook was only minimally revised.

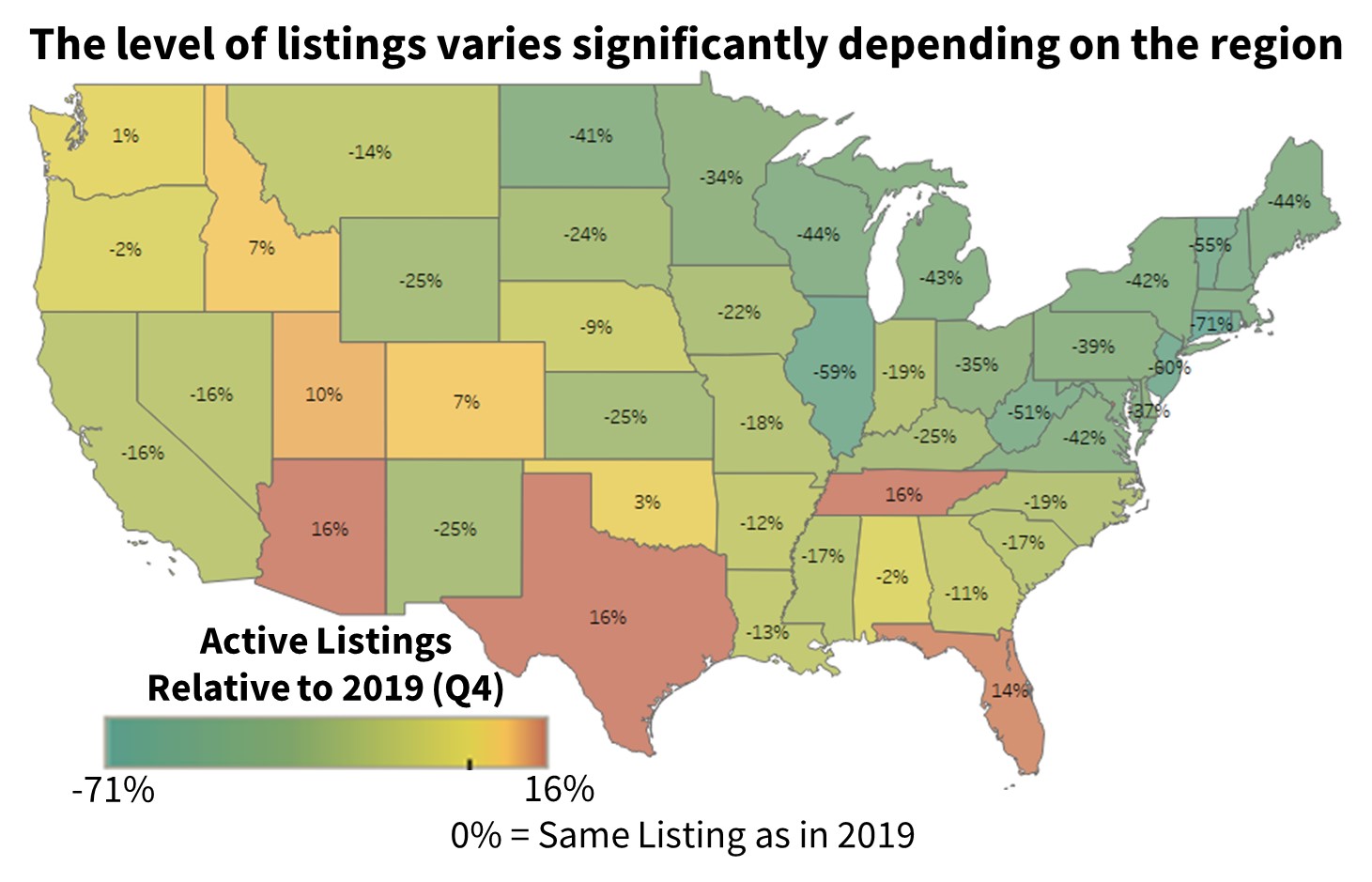

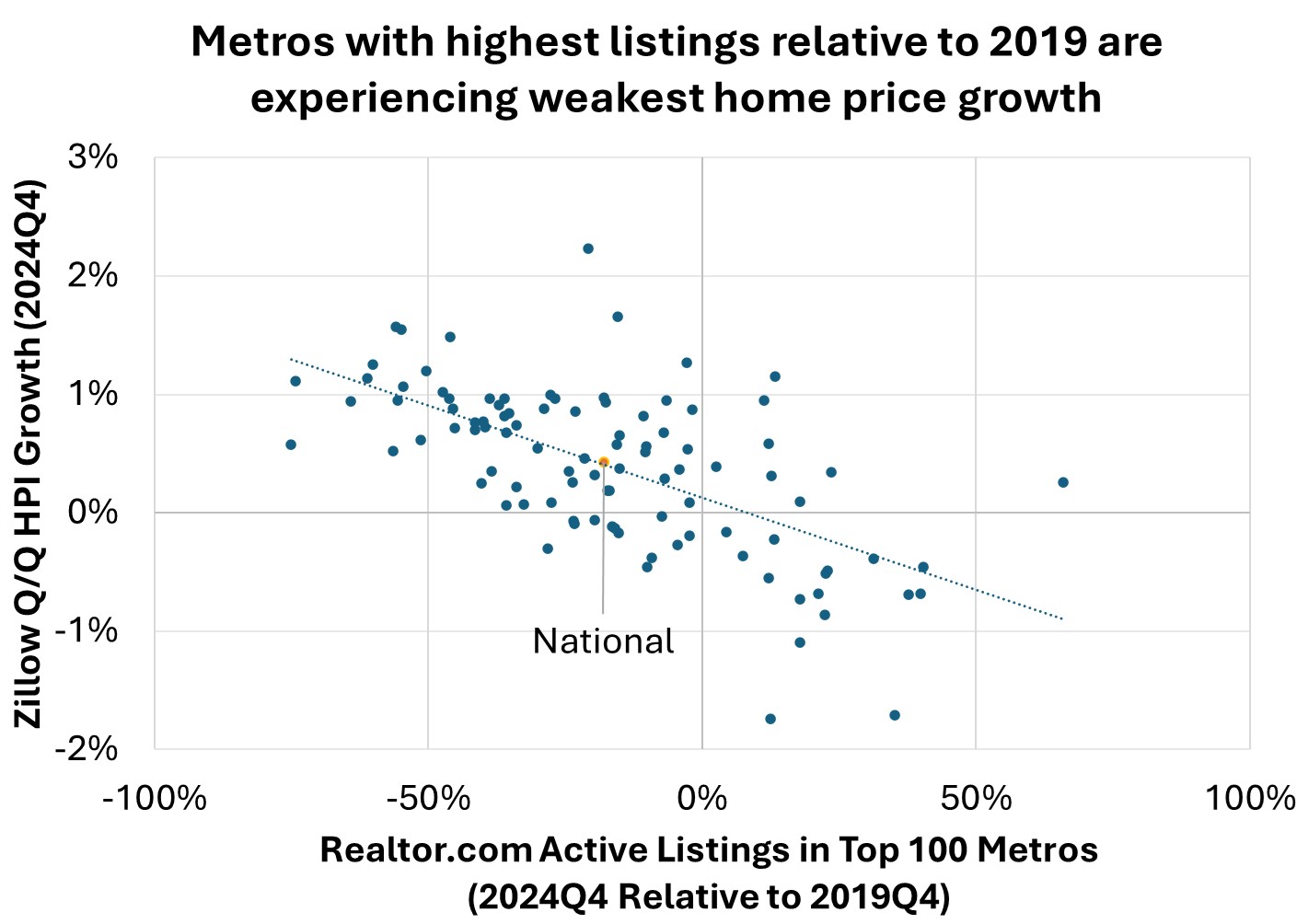

Lower Home Sales Will Continue, but Region Matters

Going forward, we suspect the regions with higher inventories at the start of the year will disproportionately drive increases in home sales, to the extent that sales on a national level increase. However, these regions will also likely disproportionately contribute to the deceleration in home price appreciation. In contrast, tight-inventory regions will likely experience comparatively firmer home price appreciation but also see less improvement in sales transactions this year, as the lock-in effect and more limited new homebuilding continues to suppress the total inventory of homes for sale.

Regarding new home construction, many of the publicly traded homebuilders have reported large declines in their operating margins as larger incentives have been required to move sales this past half year. While there is a limit to how much homebuilders are willing to offer buydowns and other concessions, the large builders continue to provide forward guidance that emphasizes a commitment to hitting sales and delivery targets, and a willingness to use deeper concessions to do so. Similarly, the most recent reading of the National Association of Home Builders Market Sentiment Survey, which is weighted towards smaller homebuilders, saw an increase of three points to the index for expected sales over the next six months, hitting the highest level since April 2022.

Therefore, we continue to expect comparatively robust new single-family home sales and construction and have only modestly downgraded both measures in this month’s forecast considering higher mortgage rates. We do, however, expect comparative softening in starts relative to sales, as homebuilders now have a growing inventory of homes for sale already started and completed, and we expect builders to prioritize clearing this inventory before ramping up new construction.

Economic Forecast Changes

Economic Growth

We've upgraded our Q4 2024 gross domestic product (GDP) growth expectation to a seasonally adjusted annualized rate (SAAR) of 2.4 percent, up one-tenth from the prior forecast, as consumption closes out 2024 on solid footing. This raises our Q4/Q4 growth expectation for 2024 by one-tenth to 2.5 percent. Our GDP forecast going forward was only slightly changed, with 2025 growth revised up one-tenth to 2.2 percent, as we expect stronger consumer spending to outweigh a wider trade deficit and modestly lower business and residential fixed investment. Our 2026 forecast is 2.0 percent Q4/Q4 growth, down a tenth from our last forecast.

Labor Market

Nonfarm payroll employment growth surprised to the upside in December, rising by 256,000, the largest gain in nine months. The unemployment rate fell one-tenth to 4.1 percent. Labor market conditions cooled throughout 2024, and it remains to be seen if this month’s strong report is an outlier or a sign that the labor market has firmed. Our unemployment forecast was essentially unchanged from the last forecast.

Inflation & Monetary Policy

Core inflation remains sticky. Recent inflation indicators have come in largely in line with our expectations; therefore, our outlook for year-over-year change in core inflation is little changed. However, we've revised our near-term oil price expectations upward, which led to an upward revision to our headline CPI forecast.

In terms of monetary policy, our baseline expectation continues to be that the Fed will cut the federal funds rate by 25 basis points in June, followed by another 25-basis-point cut in September, though there is risk of only one cut or even no cuts in 2025 if economic data continues to outperform. Given Fed guidance, the rise in rates, and the shift in risk toward firmer growth over the past month, we have removed the two cuts we previously had predicted for 2026.

Housing & Mortgage Forecast Changes

Mortgage Rates

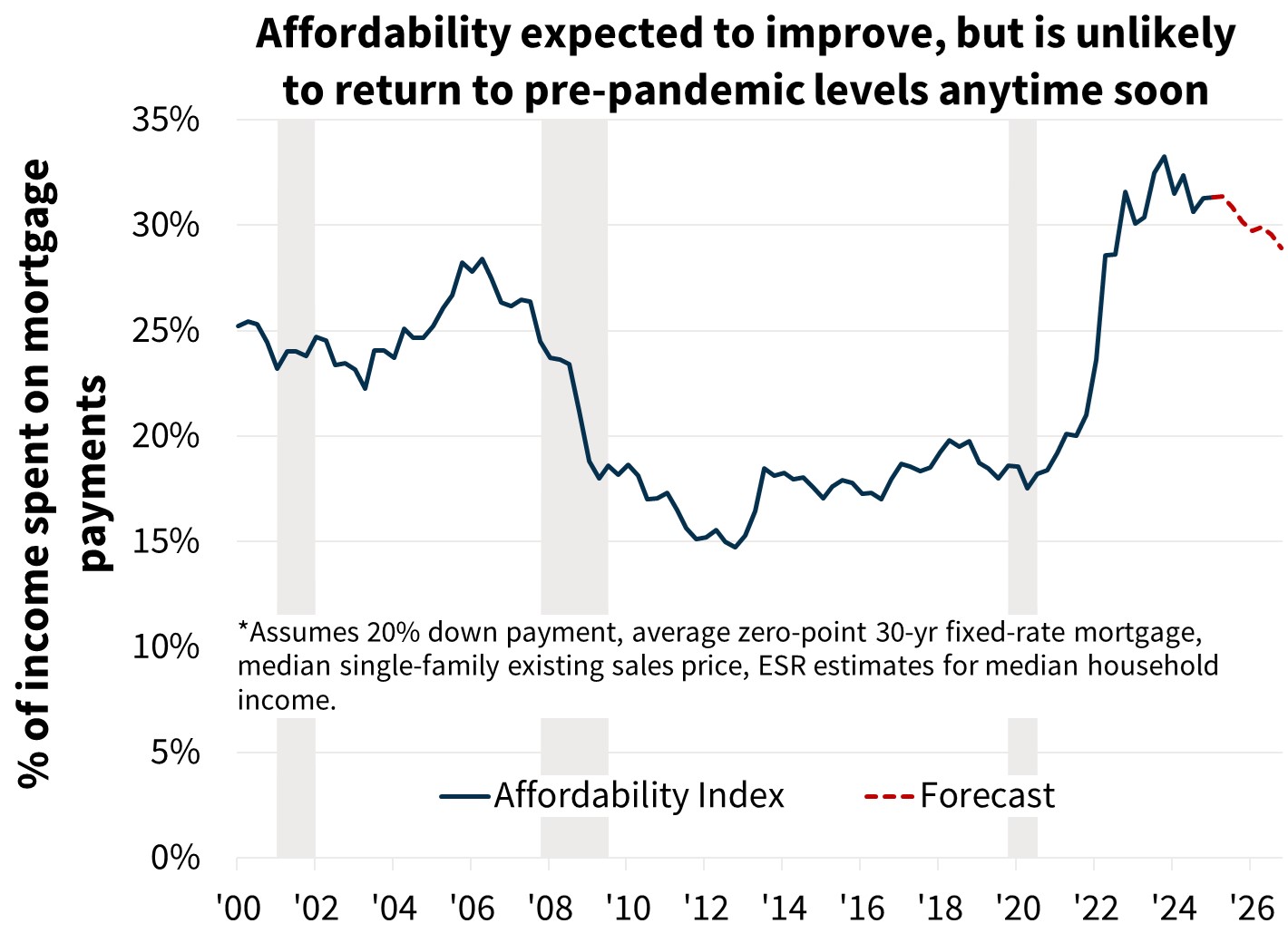

Our mortgage rate forecast has been revised upward compared to last month given the rise in interest rates since our last forecast. We expect the 30-year fixed mortgage rate to average 6.6 percent in 2025 and 6.4 percent in 2026 (up two-tenths and three-tenths, respectively, from our last forecast). However, interest rates remain volatile, particularly as the market attempts to adjust to changing expectations around Fed policy and other factors (see details above), which adds risk to our outlook.

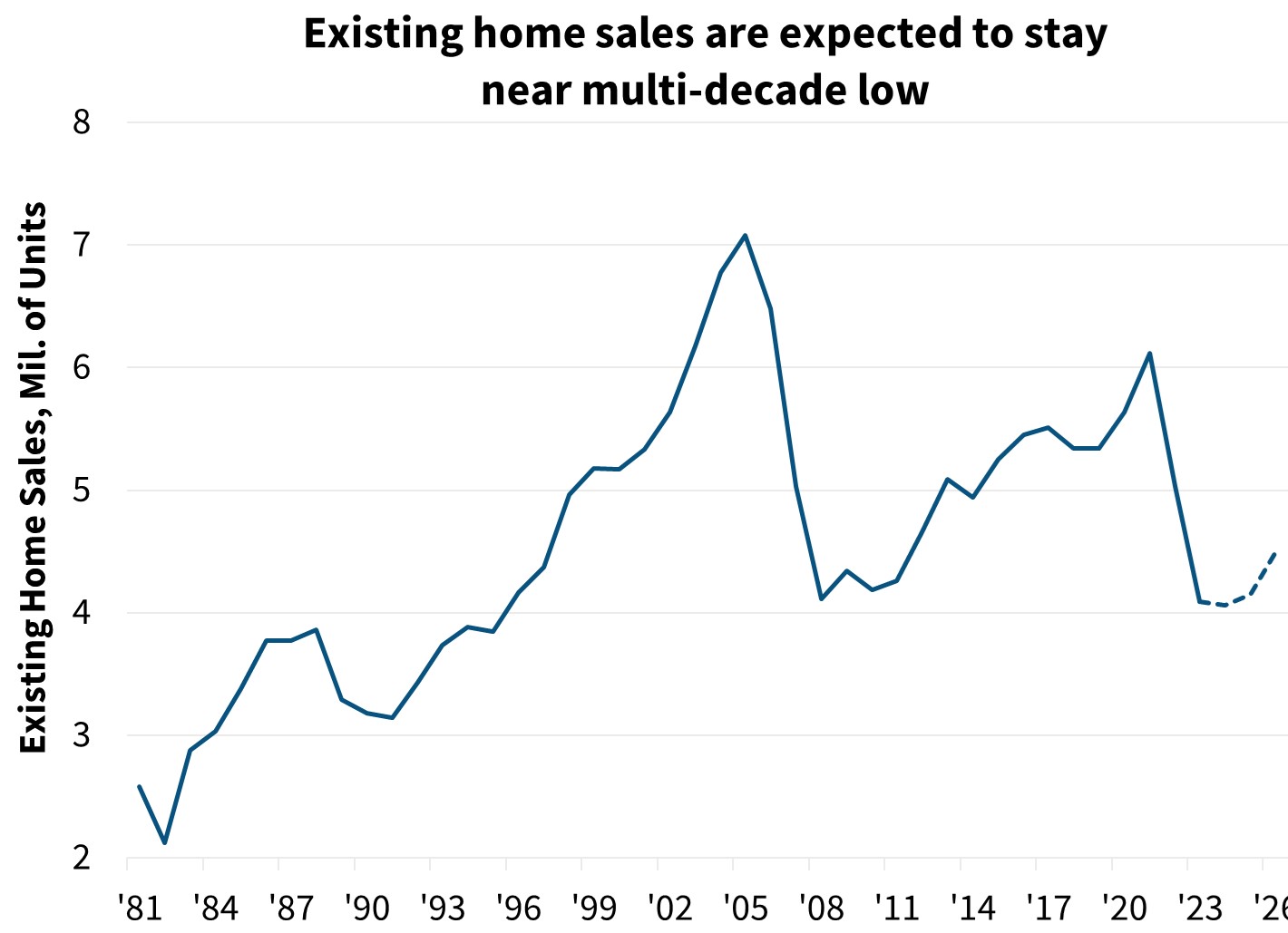

Existing Home Sales

Existing home sales rose 4.8 percent to a SAAR of 4.15 million in November. Despite this increase, our outlook for existing home sales was revised modestly downward through 2026 due to the increase in our mortgage rate forecast, which will both hurt affordability and exacerbate the lock-in effect. We expect these factors to further limit the pace of sales for the foreseeable future.

New Home Sales

New single-family home sales rose in November, rising by 5.9 percent to a SAAR of 640,000. We have downwardly revised our new home sales outlook due to our higher mortgage rate outlook, but we continue to believe that the new home sales market will be a comparative bright spot in the housing market in 2025.

Single-Family Housing Starts

Our forecast for single-family housing starts is essentially unchanged, as actuals remain in line with our forecast. Single-family starts jumped 6.4 percent in November, mostly erasing the hurricane-related decline seen in October.

Multifamily Housing Starts

Our multifamily housing starts forecast was revised lower through 2026 as interest rates continue to rise. While the multifamily starts series is notoriously volatile, we continue to believe demographic trends will be supportive of multifamily construction in the longer term once the current high levels of units in the construction pipeline are completed.

Single-Family Home Prices

January is a month when we update our quarterly single-family home price forecast. Our home price forecast was mostly unchanged from our October forecast. We project home prices on a national basis will rise 5.8 percent in 2024 and 3.5 percent in 2025 on a Q4/Q4 basis (one-tenth below last quarter’s forecast). We expect home prices to grow 1.7 percent Q4/Q4 in 2026. Our next home price update will be in April.

")

Single-Family Mortgage Originations

We expect single-family purchase volumes to be $1.4 trillion in 2025 and $1.6 trillion in 2026, representing downgrades of $19 billion and $63 billion, respectively, from the prior forecast. Overall, this represents a 2.5% decrease from our prior expectation over the 2025-2026 period, with this decrease in forecasted originations driven by a downgrade in our forecast for existing home sales. Since the mortgage rate forecast was revised upward in December, we expect the mortgage rate lock-in effect to put downward pressure on sales through the forecast horizon, as a high number of potential buyers continue to have mortgage rates on their current properties that are lower than the prevailing market rate.

While we saw an uptick in refinance originations late in 2024 given somewhat lower rates during the latter part of Q3, we have downgraded the future path of expected refinance originations resulting from the higher path for the mortgage rate assumed in this month’s forecast. For instance, 2025 single-family refinance volumes are expected to be $496 billion, representing a downgrade of $33 billion from the December forecast. In 2026, we expect single-family refinances to be $693 billion, a downgrade of $31 billion from December's forecast.

Economic & Strategic Research (ESR) Group

January 15, 2025

Data sources for charts: Federal Reserve Board, Fannie Mae, Census Bureau, Realtor.com, National Association of REALTORS®, Zillow, Freddie Mac

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Mark Palim, SVP and Chief Economist

- Patty Koscinski, Economics Director

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Eric Hardy, Economist

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst