Economic Developments - December 2023

For a PDF version of this report, click here.

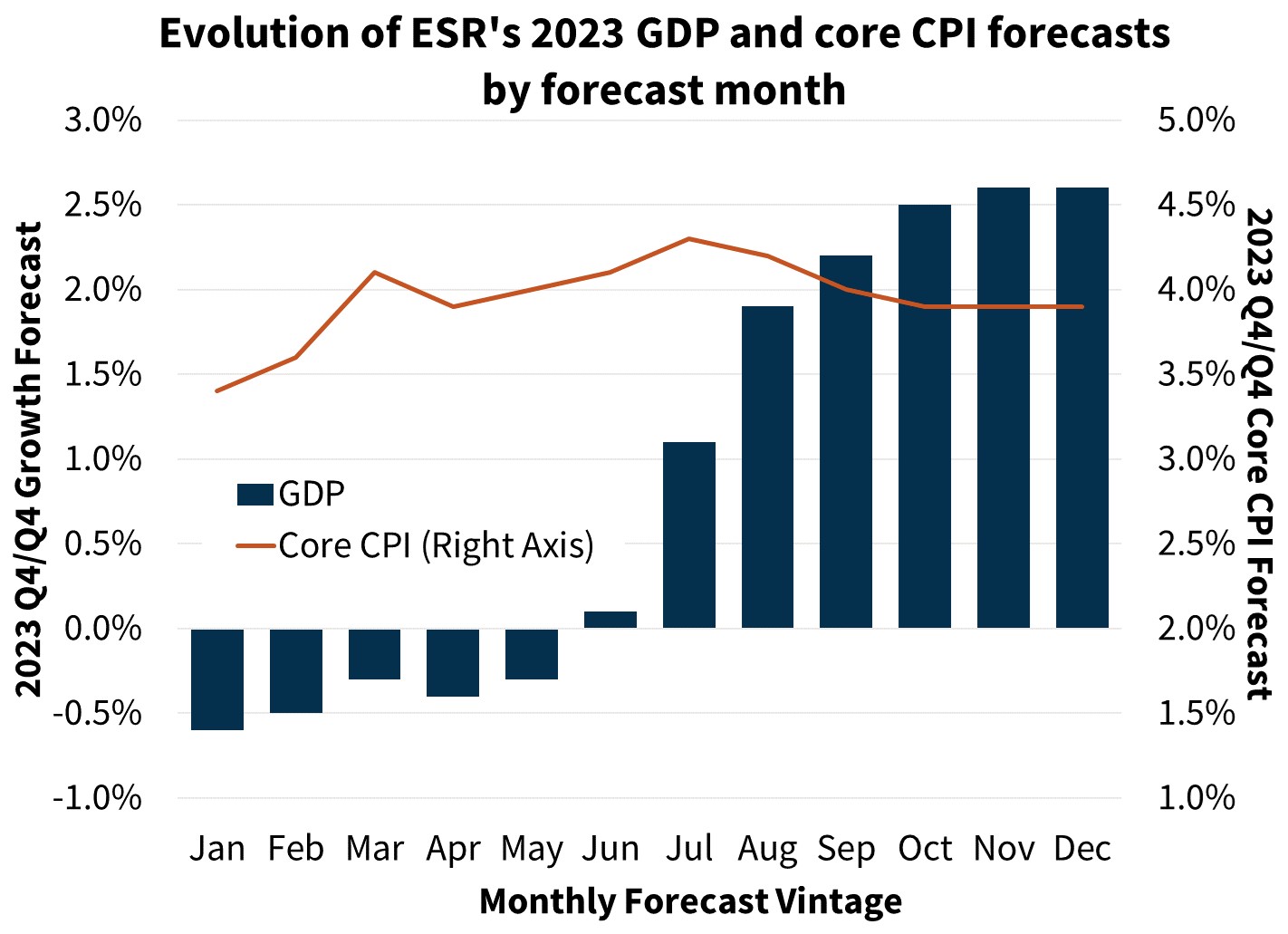

With 2023 nearing its end, we provide a look back at the year and our forecast evolution. While inflation decelerated largely as expected, economic growth has proven to be more resilient than we anticipated. We are now expecting 2023 Real Gross Domestic Product (GDP) growth to be 2.6 percent on a Q4/Q4 basis, whereas at the start of the year we were forecasting a modest 2023 recession. While the combination of disinflation alongside continued low unemployment points to a soft landing within reach, the dynamics that led us to expect a contraction mostly persist. We currently forecast GDP to decline slightly in 2024 by 0.3 percent followed by 1.7 percent growth in 2025.

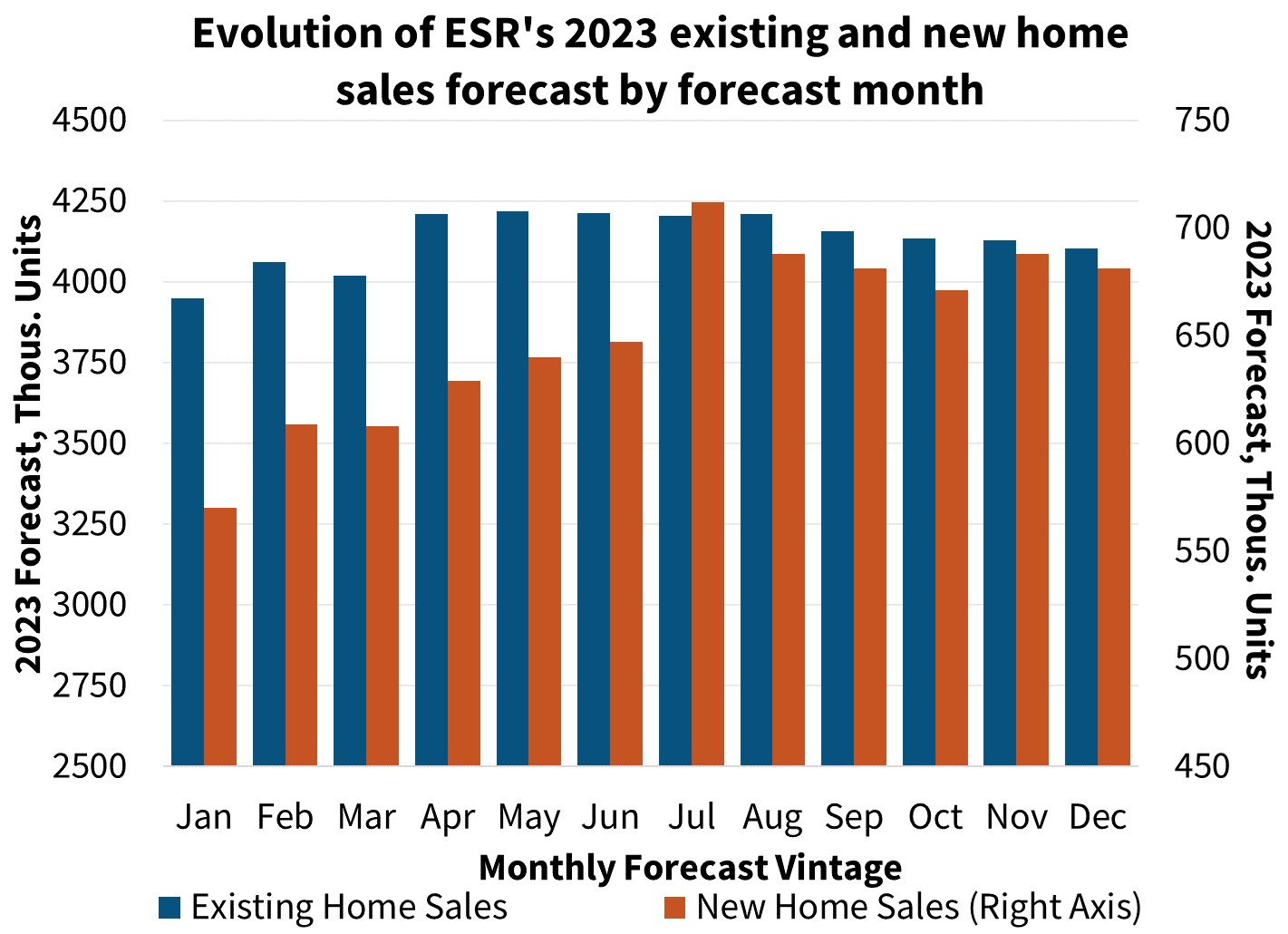

In housing, our persistent view that affordability challenges, lock-in effects, and a lack of available inventory of homes for sale would keep existing home sales at the slowest pace since the Great Financial Crisis proved correct. New home sales, however, were more resilient in the face of high mortgage rates than we had expected. The recent pullback in mortgage rates to 6.95 percent from their peak of 7.79 percent in October points to an incoming rebound in sales, but even with recent declines, mortgage rates are currently similar to those of the summer of this year. Given further declines in the ten-year Treasury rate since completion of our forecast, there is some upside risk to our home sales and originations forecast; however, rates are still comparatively high, and we still expect another year of slow sales in 2024. We project 2023 total sales will finish at 4.8 million, followed by a similar 4.8 million pace in 2024 and 5.4 million in 2025. However, taking into account home price appreciation and some modest growth in refinance activity, we forecast total single-family mortgage originations to grow from $1.5 trillion in 2023 to $1.9 trillion in 2024, and then to $2.3 trillion in 2025.

2023 Unfolded Better than Expected, but 2024 Still Poised to Slow

Fundamentally, our long-held view that the economy would enter a recession as monetary policy tightening worked to fight inflation was based on historical business-cycle dynamics that suggested inflation was unlikely to be brought back to the Fed’s 2-percent target without a significant weakening in the labor market. While some supply chain drivers of inflation were expected to subside over time, there was evidence that services inflation associated with a tight labor market had gone beyond what was consistent with an overall 2-percent inflation target. Historically, this has only been reduced via a substantial rise in the unemployment rate.

To date, however, cooling inflation and wage growth is occurring while unemployment remains low. Compared to a year ago, the Personal Consumption Expenditure (PCE) Price Index rose 3.0 percent in October while core prices were up 3.5 percent, down from cycle-peaks of 7.1 and 5.6 percent, respectively. While core inflation in particular remains elevated on an annual basis, much of this is due to ongoing high measures of shelter inflation which lag more timely market measures of rent by 4 to 5 quarters. Currently, measures of rent growth for new tenants show slowing or even negative rent growth. As such, it is only time before this is reflected in the PCE. And inflation less shelter, whether measured by the PCE or the Consumer Price Index (CPI), is already closer to the Fed’s target than the overall measures. The question of whether inflation could be brought down without a meaningful rise in the unemployment rate appears to have been answered in the affirmative.

However, we are not yet ready to declare that the window for a recession has passed. The labor market has cooled from extremely tight conditions in 2022 to a healthy level that broadly mimics its state in 2019. In November, the economy added 199,000 jobs, an increase from October, but this was inflated by the ending of the United Auto Workers (UAW) and Screen Actors Guild (SAG) strikes. Removing the effects of the strikes from both reports would indicate job gains slowed from roughly 180,000 in October to 150,000 in November. If this pace of employment growth can be maintained, then it would be consistent with a soft landing. However, the current monetary policy stance is still restrictive, and past tightening is still working its way through the economy. Bank lending is slow, near-term indicators suggest business investment is currently sluggish, and consumer spending is still in excess of its historical relationship to incomes. Whether it results in a recession or not, we believe growth is likely to decelerate significantly over the coming 2-3 quarters.

Given the current restrictive stance, to achieve a soft landing, monetary policy will need to ease sufficiently this next year to prevent a downturn, but not reanimate inflation – a difficult balance to achieve. An uptick in average hourly earnings in November illustrates the risk that the labor market could still overheat and contribute to future inflationary pressures if monetary policy is eased prematurely. As such, we are projecting the start of fed funds rate cuts in Q2 2024, but at a cautious pace.

2023 Home Sales Will Be Lowest Since 2010, With Slow Recovery Beginning in 2024

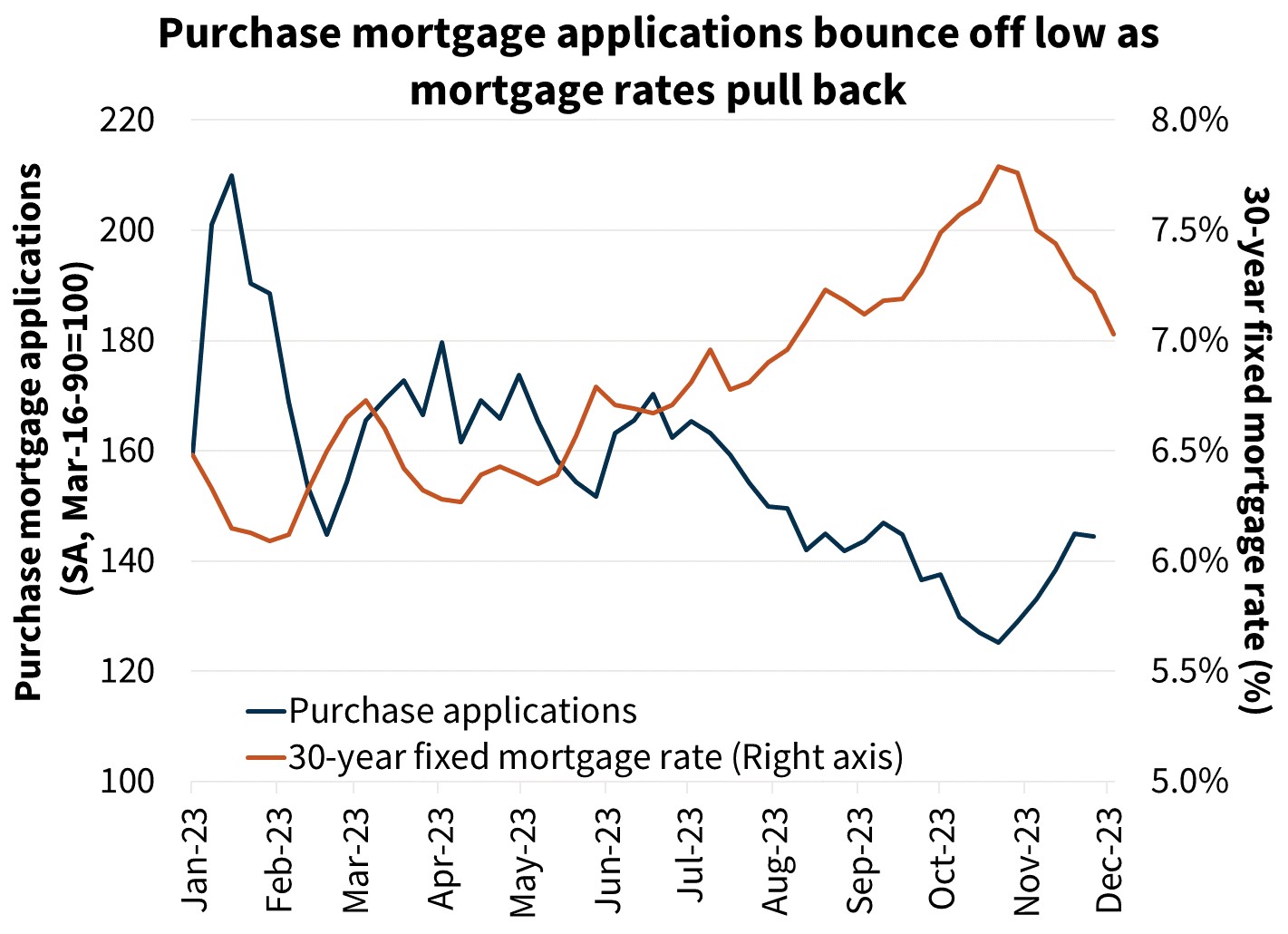

With that said, the extreme low point in October, where existing sales dropped to an annualized pace of 3.79 million, is likely to be at or near the low point. While October pending sales point to November sales also being low, purchase mortgage applications, as measured by the Mortgage Bankers Association, have bounced about 15 percent off their trough in November, as mortgage rates have fallen considerably. Given an expectation of further moderation in mortgage rates, we expect sales to start drifting upward. While the difference between a soft landing and a recession would have an effect on purchase demand, given current supply constraints, we see the path of future mortgage rates as being more determinative of sales.

Along with the resilience in new home sales, so too have home prices exceeded our start-of-year expectations, with prices rebounding modestly off mild declines in late 2022. Our mortgage originations outlook, being a function of home sales and home prices, tended to drift upward over the year but remained within a 9 percent band of what now appears to be the level of originations for the year.

Economic Forecast Changes

Economic Growth

GDP was revised upward to a 5.2 percent annualized rate in the third quarter of 2023, though the average of real GDP and Gross Domestic Income (GDI) show the economy grew 1.4 percent over the past year, which is below the long-term trend. We continue to expect a slowdown over coming quarters as consumer spending growth has exceeded income growth and higher real interest rates weigh on business investment. Conceptually our forecast is little changed from last month.

Labor Market

Nonfarm payroll employment growth was 199,000 in November (though this was inflated by the ending of the UAW and SAG strikes, which contributed an increase of roughly 47,000 workers). The unemployment rate dropped two-tenths to 3.7 percent. Compared to last month, our forecasted unemployment rate was revised downward due to incoming November data and a modest recalibration of the expected economic growth/labor market relationship.

Inflation & Monetary Policy

The November CPI report was generally in line with our expectations. Headline CPI, weighed down by energy prices, grew just 0.1 percent over the month and 3.1 percent compared to a year ago. Core inflation was more persistent, rising 0.2 percent over the month, with the annual rate unchanged at 4.0 percent as shelter inflation remains hot.

Our baseline expectation is that the Fed will begin a modest pace of fed funds rate cuts starting in Q2 2024.

Housing & Mortgage Forecast Changes

Mortgage Rates

Following the recent decline in interest rates, our interest rate forecast is lower this month, with the average FRM30 rate now predicted to average 7.4 percent over the fourth quarter of 2023. We expect the FRM30 rate to average 6.7 percent in 2024 and 6.2 percent in 2025. Our forecast was completed on December 11. Rates have declined further since then and are likely to remain volatile as we transition from monetary policy tightening to easing, which adds risk to our outlook for interest rates.

Existing Home Sales

Existing home sales were at a seasonally adjusted annualized rate (SAAR) of 3.79 million in October, below what we had anticipated, and the lowest level since 2010. With October pending sales also being weak, we have revised downward our Q4 sales estimate. However, we have revised our forecast modestly upward beginning in 2024, largely due to the lower projected interest rate environment. However, the continued heightened volatility of long-run interest rates continues to point to risk around the sales projection.

New Home Sales

New single-family home sales declined 5.6 percent to a SAAR of 679,000 in October and were downwardly revised in September; however, the lower projected interest rate path led us to modestly upgrade the forecast for new home sales. New home sales continue to benefit from the limited inventory of existing homes for sale and homebuilders’ ability and willingness to buy down borrowers’ interest rates.

Single-Family Housing Starts

Single-family housing starts rose to a SAAR of 970,000 in October and permits were at a pace of 968,000. While we continue to expect a softening trend in line with our forecast for a weakening economic backdrop, we have revised our forecast upward in part to reflect the lower projected interest rate path. We continue to expect that the lack of existing homes available for sale will continue to boost new home construction in the medium term.

Multifamily Housing Starts

Multifamily housing starts rose to a SAAR of 402,000 in October but were revised downward substantially in September. Permits rose slightly to a SAAR of 519,000. We have slightly upgraded our near-term forecast to reflect incoming data, but multifamily starts likely will decline in 2024 as national rent growth has been muted and more multifamily units near completion.

Single-Family Home Prices

Home prices grew 6.0 percent compared to a year ago in September, according to the most recently published non-seasonally adjusted FHFA Purchase-Only House Price Index (HPI). Our Fannie Mae HPI home price forecast is updated quarterly and was last updated in October. Our next home price forecast update will be in January.

")

Single-Family Mortgage Originations

We have upgraded our forecast for purchase mortgage origination volumes this month, consistent with upgrades to the home sales forecast. We now expect 2024 purchase volumes to be $1.4 trillion, an upgrade of $29 billion and a 13 percent increase from 2023’s projected volumes of $1.3 trillion. In 2025, we expect purchase origination volumes to continue to grow, reaching $1.6 trillion.

For refinances, we now project 2024 volumes to be $451 billion, an upgrade of $23 billion forecast over forecast, given the more favorable mortgage rate expectation this month. As shown by recent data from the Refinance Application-Level Index, we have seen refinance application volumes rise slightly from their trough in October as rates have fallen, supporting more refinance activity. In 2025, we expect refinance volumes to grow to $686 billion.

Economic & Strategic Research (ESR) Group

December 14, 2023

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Mortgage Bankers Association, Census Bureau, National Association of REALTORS, Freddie Mac, Fannie Mae

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Doug Duncan, SVP and Chief Economist

- Mark Palim, VP and Deputy Chief Economist

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst