Economic Developments - October 2024

For a PDF version of this report, click here.

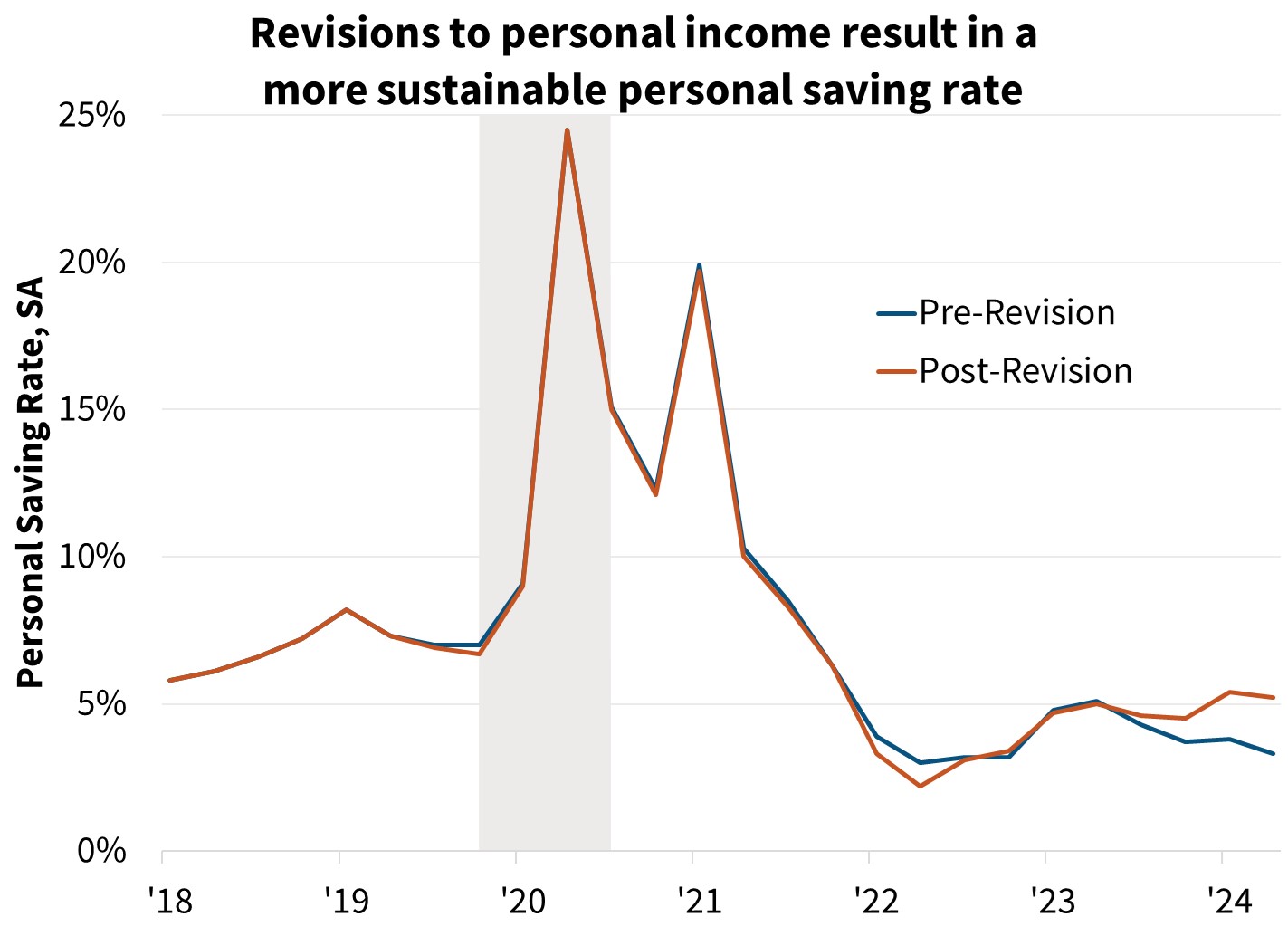

Stronger-than-expected job gains in the August employment report and sizable upward revisions to personal income data paint a picture of a more sustainable consumer spending trend going forward than had been thought just a month ago. While we still anticipate a slowing in economic growth, we’ve made a meaningful upward revision to our real Gross Domestic Product (GDP) outlook. We now forecast 2024 economic growth on a Q4/Q4 basis will be 2.3 percent (up from last month’s forecast of 2.0 percent) and 2025 growth will be 2.0 percent (up from 1.8 percent).

We have also modestly updated our quarterly home price outlook. Historical revisions to the Fannie Mae Home Price Index (FNM-HPI) point to modestly slower price appreciation over the past year; however, our outlook going forward has been revised upward. Taken together, and as measured by the FNM-HPI, we project home prices to rise 5.8 percent in 2024 (previously 6.1 percent) on a Q4/Q4 basis and 3.6 percent in 2025 (previously 3.0 percent).

We upgraded slightly our outlook for total home sales, although rising mortgage rates in recent weeks (since the completion of our interest rate forecast) present some downside risk to our forecast. We project total home sales will be 4.77 million in 2024 and 5.24 million in 2025.

Lastly, we concluded our annual mortgage originations benchmarking exercise to incorporate the latest Home Mortgage Disclosure Act (HMDA) data and have modestly upwardly revised our historical estimate for 2023 mortgage originations by $33 billion. Our outlook for total mortgage originations for 2024 is now $1.67 trillion, essentially unchanged from last month, while we project 2025 originations will be $2.14 trillion, down slightly from $2.16 trillion.

Growth Outlook Upgraded on Revisions to Income Data

We have upgraded our economic growth outlook for 2024 and 2025 in large part due to significant revisions to recent personal income data as part of the Bureau of Economic Analysis’s (BEA) annual revision to the national accounts. Pre-revision data had shown that, while personal

Although we revised our growth forecast upward, we note that our outlook of 2.3 percent growth in 2024 and 2.0 percent growth in 2025 still represents a slowdown from the 3.2 percent GDP growth recorded in 2023. Further, the long-term potential growth rate of the economy depends on several factors, including future productivity growth and immigration flows, both of which at this point remain highly uncertain. Estimates of productivity growth in recent quarters have been well above their pre-pandemic levels, though the disruptions to the economy around COVID may still be causing reverberations to these measures following a period of weakness. Still, if strong productivity growth can be sustained, the economy could operate at a higher potential growth rate than is implied in our forecast. Similarly, recent estimates of immigration flows have been strong and have contributed positively to economic growth and total job gains, but the path of future immigration flows is highly uncertain.

Economic and Labor Market Data Push Rates Higher after Brief Reprieve

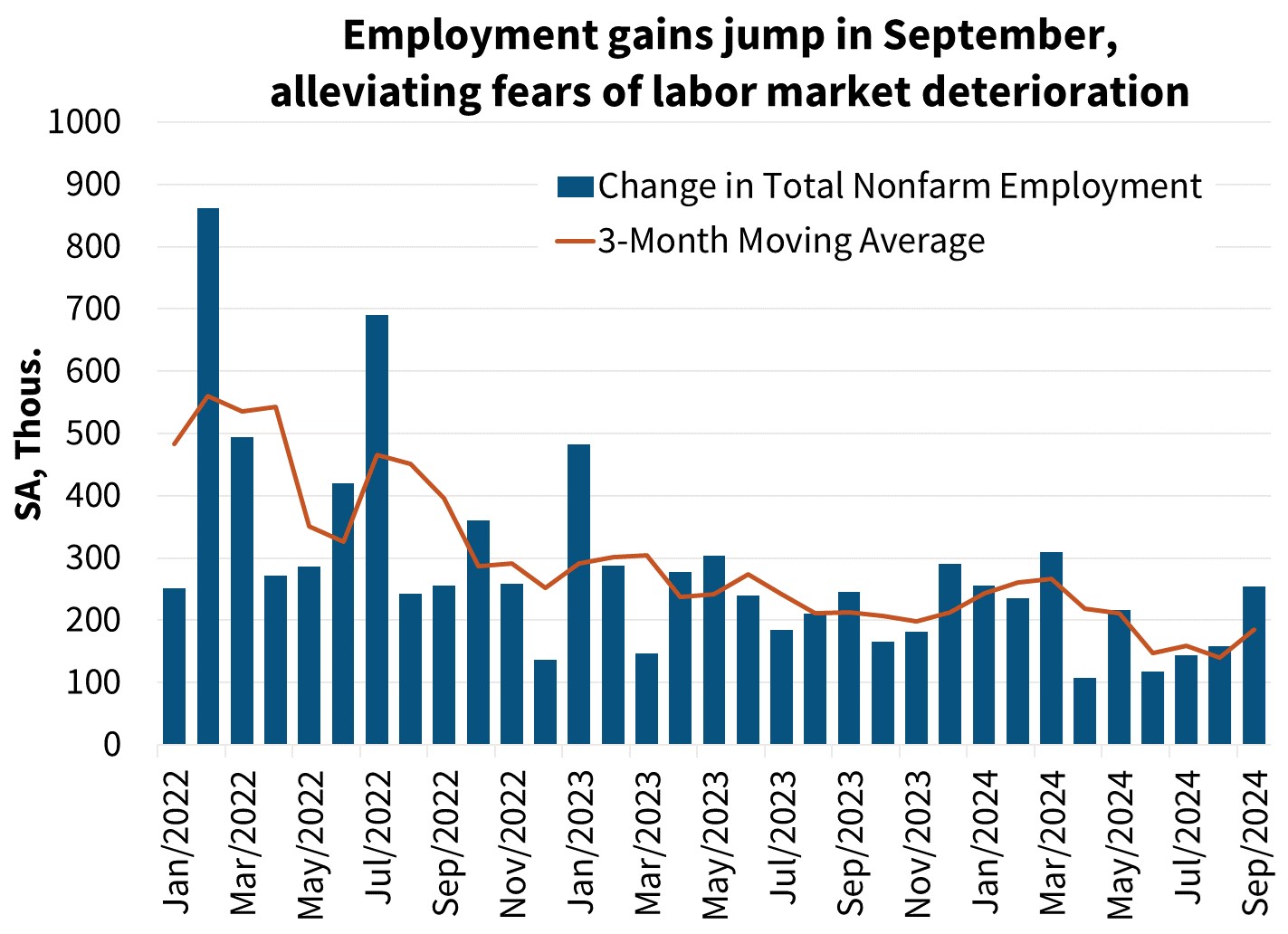

Nonfarm payroll employment rose by 254,000 in September, well above market expectations. Additionally, the prior two months of data were revised upward by a combined 72,000 jobs, and the unemployment rate declined one-tenth to 4.2 percent. Following fears that the labor market was slowing too quickly when unemployment hit 4.4 percent in July, the August and September labor reports have largely assuaged those concerns. Still, a broad range of labor market indicators continue to suggest that conditions are meaningfully looser now than in 2023. The quits rate, a useful indicator for both future wage growth and confidence in the labor market, declined to 1.9 percent in August, four-tenths below its pre-pandemic level, and the lowest since July 2015 (excluding the pandemic period). The Kansas City Fed Labor Market Conditions Index, an aggregate of 24 monthly measures of labor market conditions, remains in positive territory (signaling better than long-run average conditions) but is nearly 50 percent lower than it was a year ago in September 2023. On balance, we continue to expect a gradual slowing in employment growth. Similar to our expectation that the economy will return to roughly its long-run growth rate, we believe the unemployment rate will rise modestly to 4.4 percent, roughly our current estimate of the natural rate of unemployment.

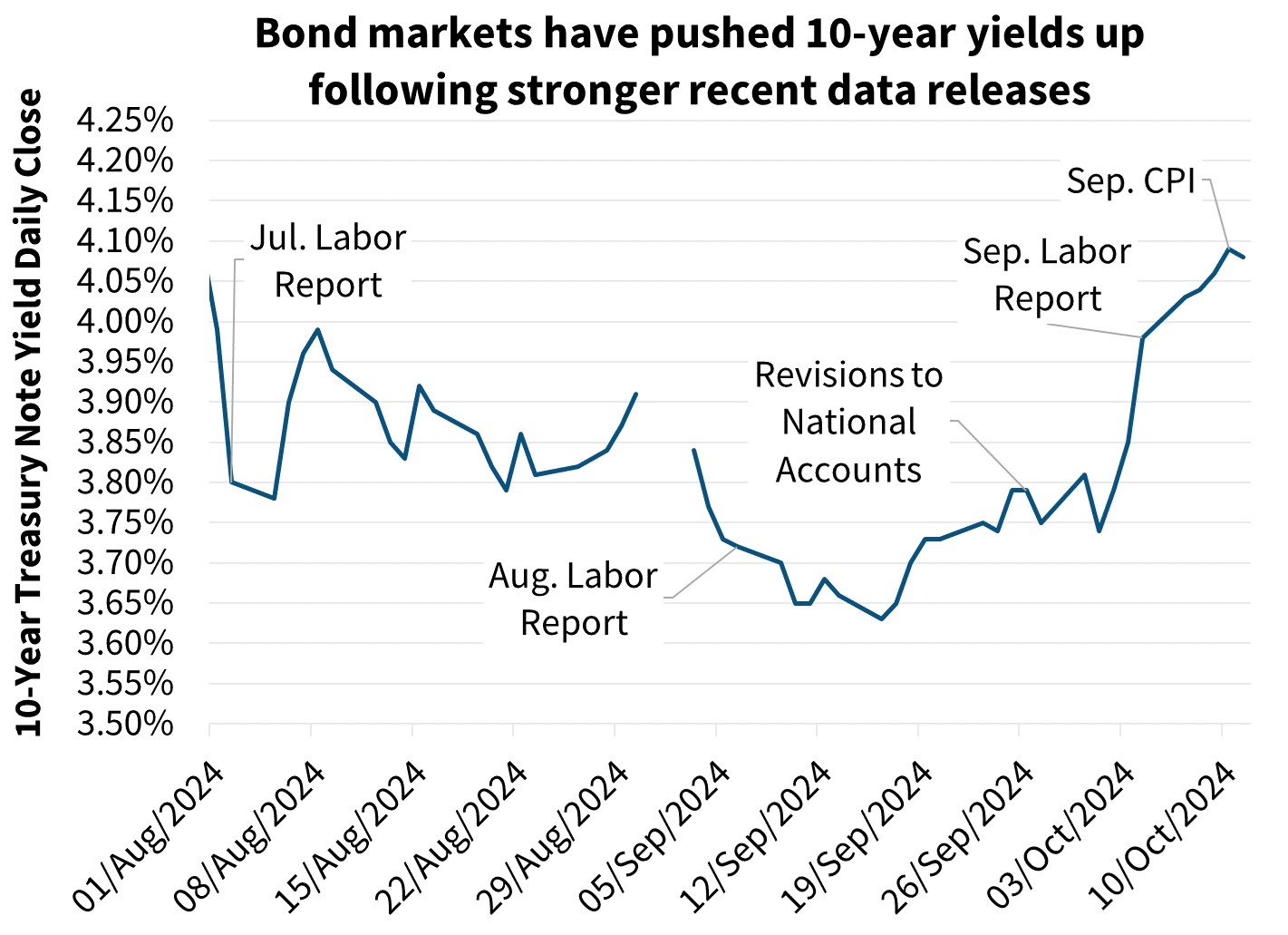

Following the release of the September labor report, the 10-year Treasury jumped 13 basis points to 3.98 percent and has continued to rise. Between the upward revisions to personal income and the saving rate, an above-consensus labor report, and a slightly hotter-than-expected core Consumer Price Index (CPI) release in September, markets have digested a number of critical data releases that have ultimately pushed back their expectations of cuts to the federal funds rate and moved long-duration yields upward. Our official interest rate forecast, which was completed at the beginning of the month, shows the 10-year Treasury yield and mortgage rates lower compared to our prior outlook. However, given the recent movement in interest rates since our forecast was completed, our rate outlook faces upside risk.

Apart from the slightly above-consensus CPI report, rates have risen because of “good” reasons, including better economic growth and above-consensus increases in payroll employment. Therefore, we don’t expect the recent rise in the 10-year Treasury, from the low of 3.65 percent in mid-September to around 4.1 percent as of this writing, to act as a significant headwind for future growth. On balance, the improved economic and labor market outlook are benefits to the housing market, though the rise in mortgage rates from close to 6 percent at the end of September to 6.32 percent as of this writing, is likely to keep home sales activity at subdued levels.

Home Price Outlook Upgraded as Sales Expected to Remain Subdued

As measured by the Fannie Mae Home Price Index (FNM-HPI), home prices increased 5.9 percent year over year in Q3 2024, a deceleration compared to the previous quarter’s downwardly revised year-over-year growth rate of 6.3 percent. We have updated our quarterly home price outlook and now expect modestly strong home price appreciation through 2025. However, revisions to historical data on balance were to the downside, leading to a modest downward revision to our 2024 expectation for year-total home price growth, but an upward revision to our 2025 outlook. We are expecting deceleration of home price growth as affordability continues to be stretched and inventories of homes available for sale are rising in some regions. However, the overall low level of available homes for sale is still bolstering home price appreciation, especially as income growth and employment remain strong.

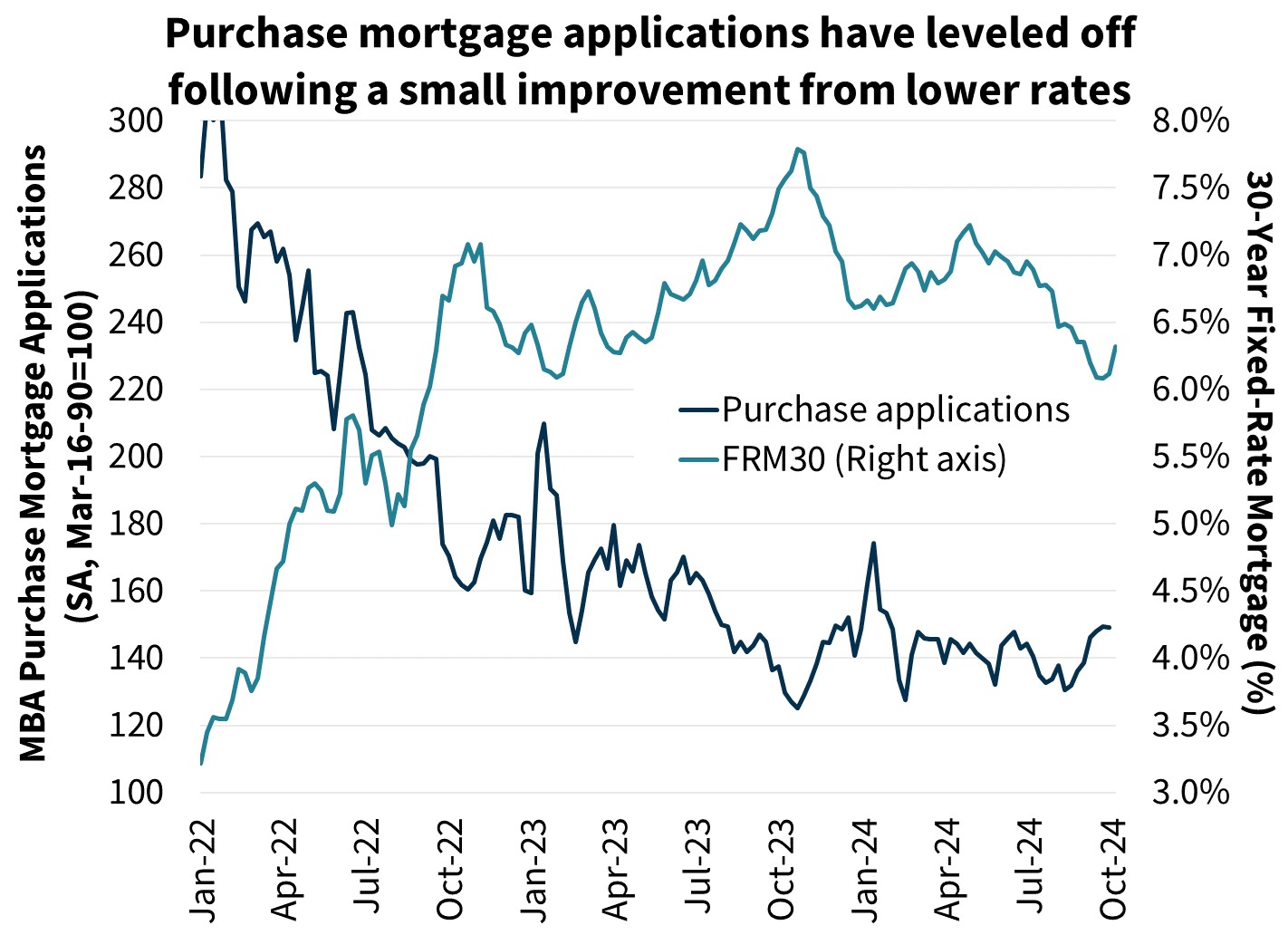

We have modestly upgraded our existing home sales outlook in 2025 largely due to a lower mortgage rate forecast; however, as previously noted, mortgage rates have risen meaningfully following strong economic data, presenting upside risk to our rate outlook but also downside risk to our sales projection. Regardless of mortgage rate volatility, “lock-in” effects still remain strong, and we expect a recovery in home sales to be modest in the near term. While a strong economic outlook will support home purchase demand, this will also likely lead to higher mortgage rates, which would keep sales of existing homes more subdued. In fact, the modest bump in purchase mortgage applications seen in September has now leveled off in the most recent week’s data.

However, with continued resilience in the labor market, and the low level of existing homes for sale, we expect the new home sales market to continue to remain a bright spot. We have upwardly revised our new home sales expectations for 2024 and 2025, while slightly increasing our single-family housing starts forecast.

Annual Benchmarking Update to Mortgage Originations Estimate

We have updated our estimate of 2023 mortgage origination volumes as part of our annual benchmarking exercise to incorporate the latest Home Mortgage Disclosure Act (HMDA) data. Specifically, we have revised upward total mortgage volumes by $33 billion to $1.5 trillion in 2023, with the purchase market being revised upward by $60 billion to $1.28 trillion and the refinance market being revised downward by $27 billion to $221 billion. As part of this benchmarking work, our estimate of the share of homes purchased with cash instead of a mortgage was revised downward somewhat relative to last month’s forecast.

Looking forward, our 2024 expectation for purchase mortgage volumes is essentially unchanged from last month at just over $1.3 trillion, while our estimate of refinance volumes was revised downward by $7 billion. Despite the somewhat lower mortgage rate projection, our benchmarking activity has caused us to revise downward the overall size of the refinance market in future periods, as well, relative to last month’s forecast.

In 2025, we expect purchase volumes to grow to $1.5 trillion, as home sales rebound somewhat from recent lows and solid home price appreciation continues. Refinance volumes are expected to grow to $625 billion in 2025, as a gradually declining mortgage rate path continues to be supportive of refinance activity. While refinance application activity has dipped as of late, as seen in the Refinance Application-Level Index (or RALI), application activity is still well above levels seen earlier in 2024.

Economic Forecast Changes

Economic Growth

The third estimate of Q2 2024 GDP was unchanged at an annualized 3.0 percent. However, the annual revision by the BEA to the national accounts data showed much stronger data for personal income and the saving rate. This explains the resilience of the consumer and suggests further spending power moving forward, which led us to revise our GDP expectations upward. Our GDP forecast for total yearly growth in 2024 on a Q4/Q4 basis was revised upward three-tenths to 2.3 percent. Our forecast for growth in 2025 was revised upward two-tenths to 2.0 percent Q4/Q4.

Labor Market

Nonfarm payroll employment growth jumped in September, rising by 254,000, while the July and August employment figures were revised upwards by a combined 72,000. The unemployment rate fell one-tenth to 4.1 percent. Given this, as well as the stronger economic growth outlook, our unemployment rate expectations were revised downward slightly, though we continue to expect the labor market to cool at a gradual pace.

Inflation & Monetary Policy

Our inflation outlook was little changed. The September Consumer Price Index (CPI) report was essentially in line with our expectations for further deceleration in inflation. We continue to forecast inflation to moderate over our forecast horizon.

In terms of monetary policy, our baseline expectation remains that the Fed will cut the federal funds rate by 25 basis points in November and December, followed by four 25-basis point cuts throughout 2025.

Housing & Mortgage Forecast Changes

Mortgage Rates

We revised downward our mortgage rate forecast for 2024 given the decline in longer-term interest rates in September. We continue to forecast the 30-year fixed mortgage rate to average 6.6 percent in 2024 (unchanged from last month’s forecast) and to average 5.7 percent in 2025 (down two-tenths from last month’s forecast). However, interest rates remain volatile, particularly given changes to Fed policy expectations, which adds risk to our outlook. Following the completion of our beginning-of-the-month interest rate forecast and as of this writing, 10-year Treasury rates have increased almost 30 basis points, leading to some upside risk to our current baseline mortgage rate forecast.

Existing Home Sales

Existing home sales fell 2.5 percent to a seasonally adjusted annualized rate (SAAR) of 3.86 million in August. Our near-term outlook for existing home sales was essentially unchanged, despite the lower mortgage rate path. High-frequency indicators, such as purchase applications, have shown little movement despite lower mortgage rates. However, we continue to forecast existing sales to trend gradually upward over our forecast horizon as affordability slowly improves and lock-in effects weaken.

New Home Sales

New single-family home sales fell 4.7 percent in August to a SAAR of 716,000. We have upwardly revised our new home sales outlook given the decline in interest rates in our forecast this month, and we continue to expect the dearth of existing homes being listed for sale to help support new home sales and lead to a gradual increase over the forecast horizon.

Single-Family Housing Starts

Our forecast for single-family housing starts is essentially unchanged. Starts rebounded in August as expected, though the September report may be impacted by the recent hurricanes. Overall, we continue to expect that the shortage of homes will help spur residential construction in the coming years.

Multifamily Housing Starts

Similar to the single-family starts series, our multifamily housing starts forecast was mostly unchanged. While the multifamily starts series is notoriously volatile, we continue to believe demographic trends will be supportive of multifamily construction further out in the future once the current high level of units in the construction pipeline work their way onto the market over the next couple of years.

Single-Family Home Prices

We have revised our quarterly home price forecast this month. We now forecast national home prices to rise 5.8 percent in 2024 (a downward revision of three-tenths from our July forecast) and 3.6 percent in 2025 (an upgrade of six-tenths) on a Q4/Q4 basis. Our next home price update will be in January.

")

Single-Family Mortgage Originations

We have updated our estimate of 2023 mortgage origination volumes as part of our annual benchmarking exercise to incorporate the latest Home Mortgage Disclosure Act (HMDA) data. Looking forward, our 2024 expectation for purchase mortgage volumes is essentially unchanged from last month at just over $1.3 trillion, while our estimate of refinance volumes was revised downward modestly. Despite the somewhat lower mortgage rate projection, our benchmarking activity has caused us to revise downward the overall size of the refinance market in future periods as well.

In 2025, we expect purchase volumes to grow to $1.5 trillion, as home sales rebound somewhat from recent lows and solid home price appreciation continues. Refinance volumes are expected to grow to $625 billion in 2025, as a gradually declining mortgage rate path continues to be supportive of refinance activity.

Economic & Strategic Research (ESR) Group

October 15, 2024

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Federal Reserve Board, Mortgage Bankers Association, Freddie Mac

Opinions, analyses, estimates, forecasts, beliefs, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, beliefs, and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Mark Palim, SVP and Chief Economist

- Doug Duncan, SVP

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Eric Hardy, Economist

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst