Now is the Time to Adopt Digital Mortgage Technology

Raising the bar for a better mortgage experience

Raising the bar for a better mortgage experience

As the Amazons and Ubers of the world continue to raise the bar for "consumer-grade" experiences, homebuyers have made it clear that it's also time for the home purchasing and mortgage processes to change. Although the mortgage process is extremely complex and heavily regulated, digital experiences in other businesses have increased the demand for digital resources to speed up the onerous mortgage process. Lenders recognize this demand, citing consumer-facing technology as their top priority. Unsurprisingly, homebuyers also crave a human touch as they navigate this very personal and significant life decision.

How should lenders prioritize digital investments?

The choice of which digital investments to pursue is critical at a time when lenders also cite cost-cutting as a top priority, so we asked about 3,000 recent homebuyers, via our National Housing Survey®, to tell us which aspects of the mortgage process would benefit most from digitization, and which areas are best supported with a human touch.

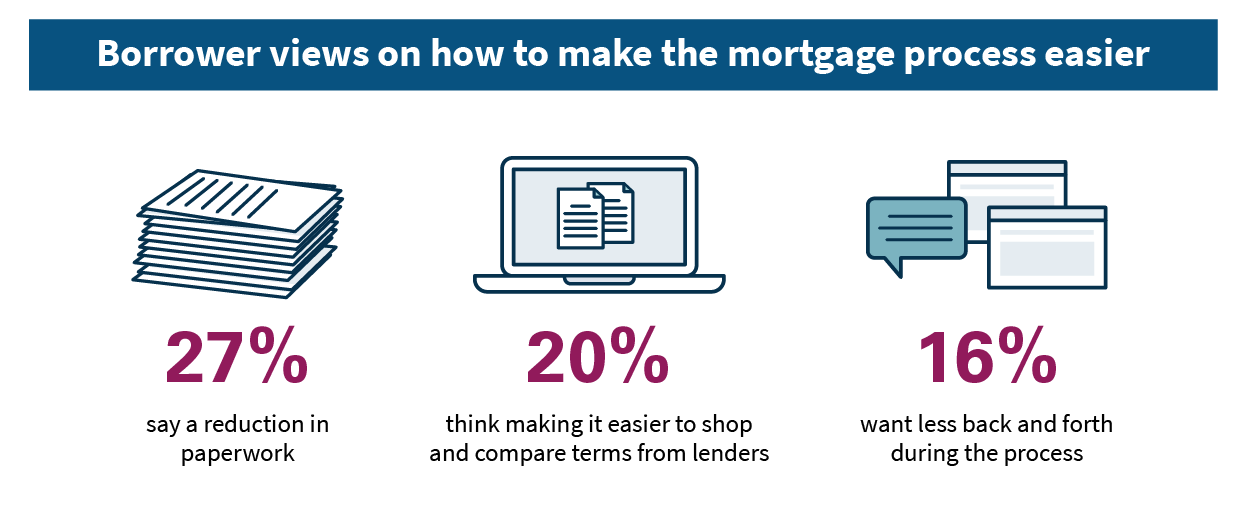

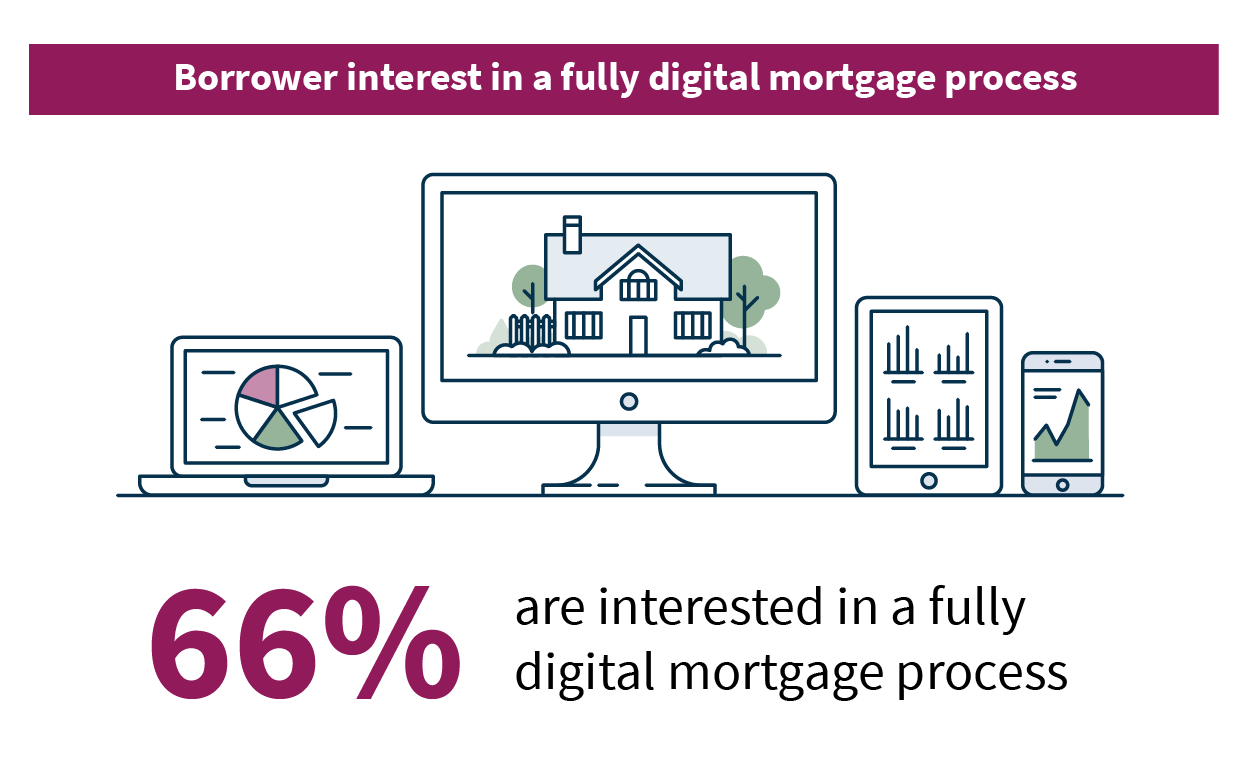

Above all, borrowers want less paperwork. Gathering the necessary financial information to apply and get approved for a loan was cited as the most difficult part of process by far. This is especially true for those over the age of 45 or those who have purchased more than one home in their lifetime. Ideally, these homebuyers would like to see the application and pre-approval processes digitized as well. When asked what they thought of a fully digital mortgage process, where all steps could be completed online, most said they would be "somewhat" or "very" interested.

The majority of homebuyers said they’d like to see the mortgage process, from application to close, completed in one month. That's 5 days less than the current median process, which takes about 35 days.

Maintaining a personal touch

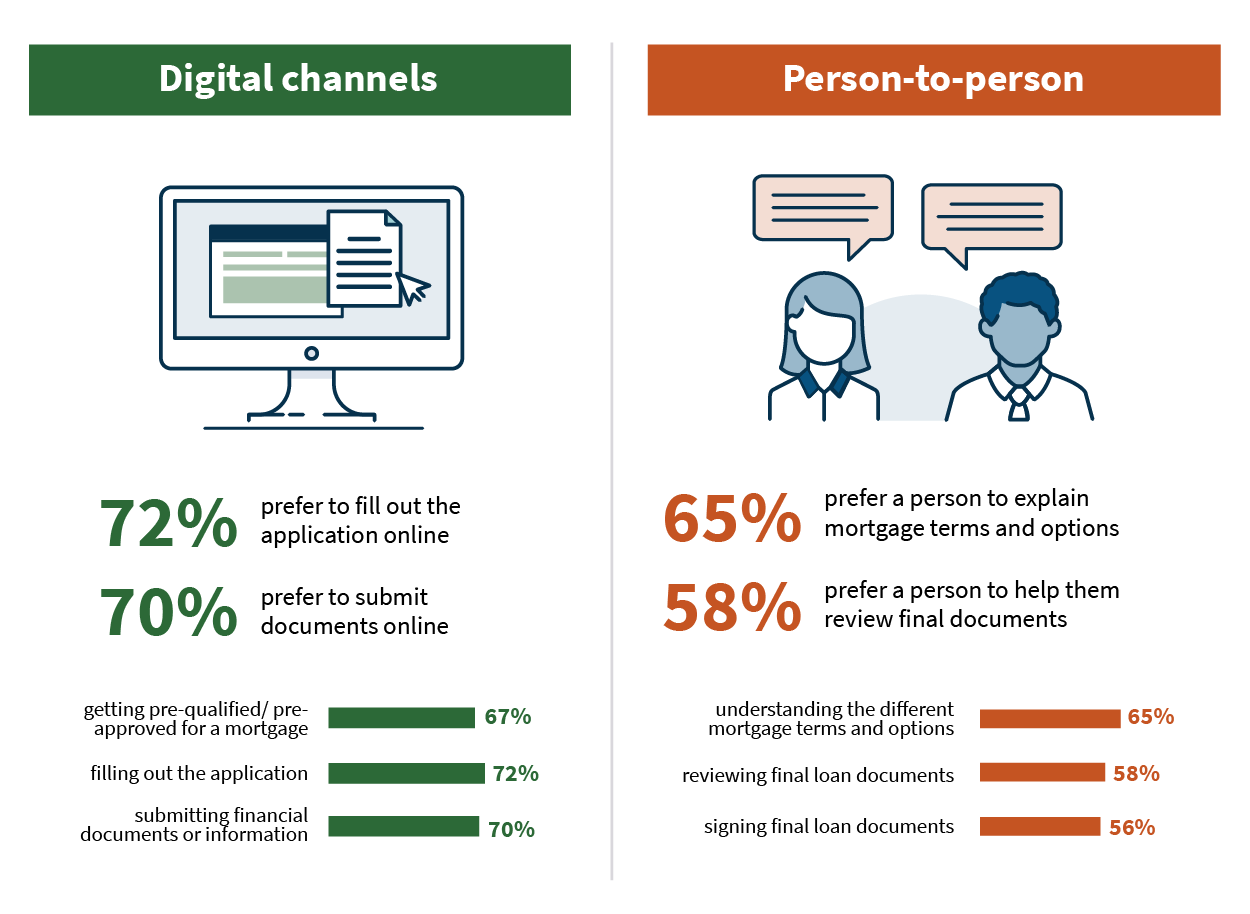

While younger and higher-income borrowers tend to prefer digitization more frequently than others, they still prefer interpersonal interaction for the more complex or critical steps of the process, such as reviewing final loan documents and understanding mortgage terms and options, as much as everyone else does.

A digital future

Change in the mortgage industry is accelerating, opening the door for potentially significant impact and value creation for lenders and homebuyers alike. There is good reason to be optimistic about the future.

We are partnering with lenders, large and small, in our product design process, creating a digital experience that will improve the mortgage process. We’ve worked with lenders to leverage digital data from third-party vendors to quickly validate borrowers’ income, assets, and employment data. Through an automated programming interface (API) platform, we’re starting to share pieces of our process with lenders, so they can quickly access what they need. We’ve reduced the application to delivery cycle time by 7 days with a goal to reduce it to just 10 days.

There’s much more work to do, and we look forward to continued partnership with our customers as we design, create, and adopt technology with the potential to transform the digital mortgage space.

Henry Cason

SVP and Head of Digital Products, Single-Family Mortgage Business

August 28, 2018

Henry Cason is the head of Digital Products for Fannie Mae's Single-Family business. He integrates business and technology to help lenders deliver the digital consumer-quality experiences we’ve all come to expect in our everyday lives.

Our Company

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count