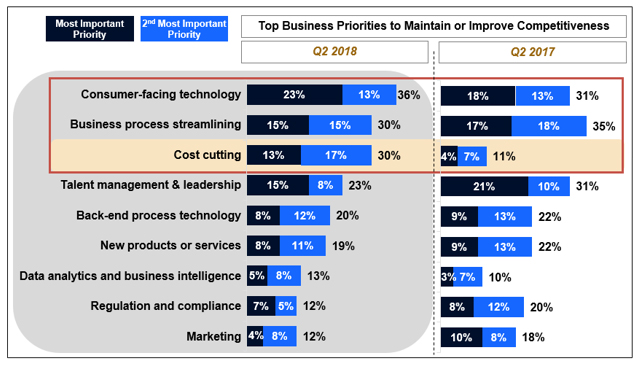

Cost Cutting Has Emerged as a Focus of Lender Competitiveness

In Fannie Mae's second quarter Mortgage Lender Sentiment Survey®, we asked mortgage executives to identify their top business priorities for 2018, the same question asked in the second quarter of last year. The results showed that, while "consumer-facing technology" and "business process streamlining" remained the two most important business priorities,"cost cutting" jumped from the second least important priority in 2017 to the third most important priority this year.

In Fannie Mae's second quarter Mortgage Lender Sentiment Survey®, we asked mortgage executives to identify their top business priorities for 2018, the same question asked in the second quarter of last year. The results showed that, while "consumer-facing technology" and "business process streamlining" remained the two most important business priorities,"cost cutting" jumped from the second least important priority in 2017 to the third most important priority this year.

The second quarter results released last week1 also painted a gloomy picture for the housing market. Mortgage demand sentiment reached a three-year low and lenders' profit margin outlook remained negative for the seventh consecutive quarter.

The rise of cost cutting as a competitiveness priority should not come as a surprise. Today, lenders are facing an increasingly difficult market environment. Mortgage rates have risen about 80 basis points since September 2017, pushing refinance activity down sharply. Refinance applications fell every week in May, dragging the monthly average to the lowest level since December 2000.

Existing home sales and new home sales fell in April to 5.46 million and a 662,000 seasonally-adjusted annualized rate (SAAR), respectively. Year-to-date existing home sales through April were 0.7 percent below the level during the same period last year. New home sales fared better, with year-to-date sales increasing 8.5 percent compared with sales through April 2017. Leading indicators suggest a meaningful rebound is unlikely, as pending home sales fell 1.3 percent in April from March, and 2.1 percent from a year ago, marking the fourth consecutive year-over-year drop. Furthermore, purchase mortgage applications fell every week in May, sending the average monthly volume 2.9 percent below April’s average reading.

The problem for the home purchase market is not demand. The National Association of REALTORS® (NAR) noted that homes are selling fast, with properties typically staying on the market for only 26 days in April, the shortest duration since the series began in 2011. In another sign of strong demand, NAR reported that multiple offers are becoming increasingly common.2

Inventory shortages are impeding sales, although demand remains robust. The for-sale inventory of existing homes has remained below the year-ago level for nearly three years. While the number of new homes for sale has continued to trend up, the increase has been concentrated in incomplete units. Ongoing tightness in the for-sale inventory of existing homes and completed new homes is likely to continue to restrain new home sales and boost prices. The main first-quarter measures of home prices—the S&P CoreLogic Case-Shiller, CoreLogic, and FHFA home price indices—showed strong annual gains between 6.4 percent and 6.9 percent for the nation.

Increasingly tight margins will likely persist as a top driver of lenders' mortgage business strategy, with our outlook calling for interest rates to continue rising and housing inventories to remain tight. Despite lenders making significant investments to improve operational efficiency over the past few years, margins have still declined.

In the first quarter of 2016, pre-tax production profit per loan was 33 basis points. Profits declined to 10 basis points in the first quarter of 2017 until, finally this past quarter, the industry took a loss of 8 basis points per loan, the first loss in four years3. Now, they appear to be turning to cost cutting as a means of managing their bottom lines. Personnel expenses made up 66 percent of total loan production expense in the first quarter of 2018, little changed from the prior quarter and from a year ago4. Payroll reduction could potentially assume a more prominent role in future cost-cutting efforts. While hiring among nonbanks and mortgage brokers remained elevated in April, hovering near expansion highs, mortgage industry employment may be approaching the cyclical peak. With rising interest rates and tight housing supply squeezing mortgage origination volumes, lenders could soon turn to job reduction as a means of maintaining a competitive edge.

To learn more, read the full report "Cost Cutting Has Emerged as a Focus of Lender Competitiveness."

Doug Duncan

Chief Economist and Senior Vice President

Economic and Strategic Research

June 21, 2018

The author thanks Li-Ning Huang, Orawin Velz, Rebecca Meeker, Frank Shaw, and Steve Deggendorf for valuable input in the creation of this commentary. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group or of survey respondents reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in this commentary is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

1 For details about the Mortgage Lender Sentiment Survey, please visit the survey webpage at https://www.fanniemae.com/portal/research-insights/surveys/mortgage-lender-sentiment-survey.html

For the full Q2 2018 survey report, please see https://www.fanniemae.com/resources/file/research/mlss/pdf/mortgage-lender-sentiment-survey-findings-q22018.pdf

2 For details, please see https://www.nar.realtor/newsroom/pending-home-sales-lose-steam-in-april-decline-13-percent

3 For details about the Mortgage Bankers Association’s IMB Production Profit data, please see https://www.mba.org/publications/insights/articles/current-issue/mba-chart-of-the-week-imb-production-profit-and-volume?_zs=84rwB1&_zl=iIJV4

4 Source: MBA Quarterly Mortgage Bankers Performance Report, Q1 2018

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count